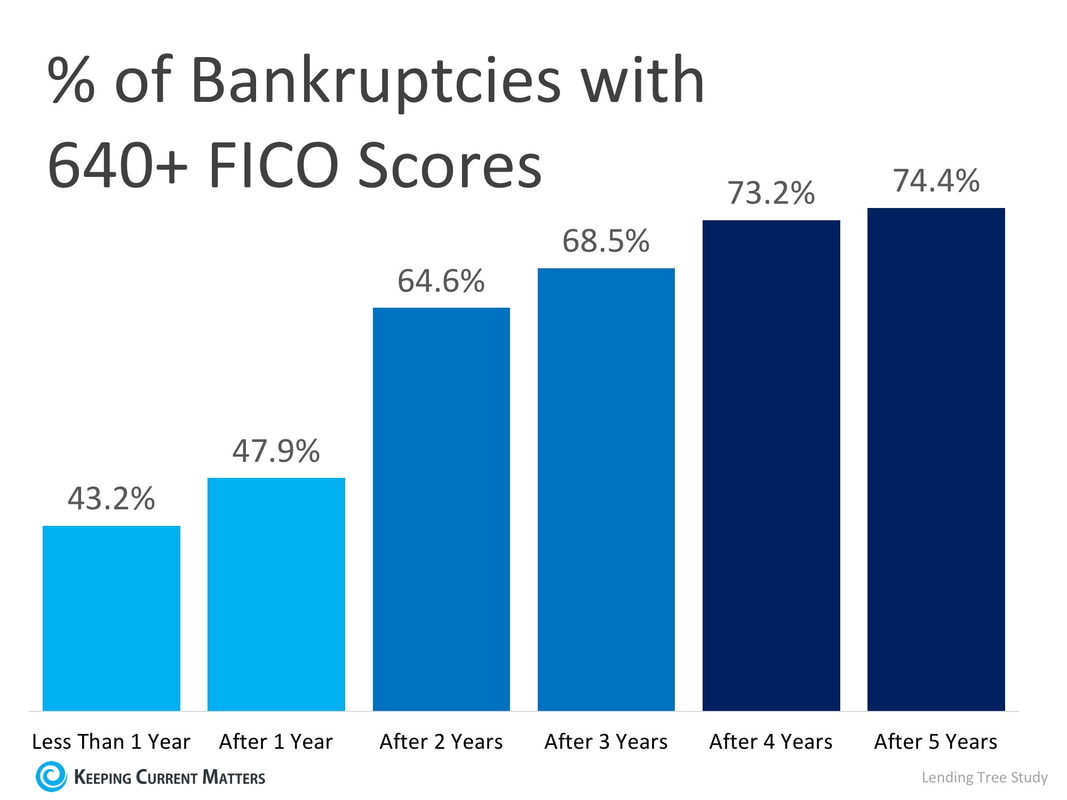

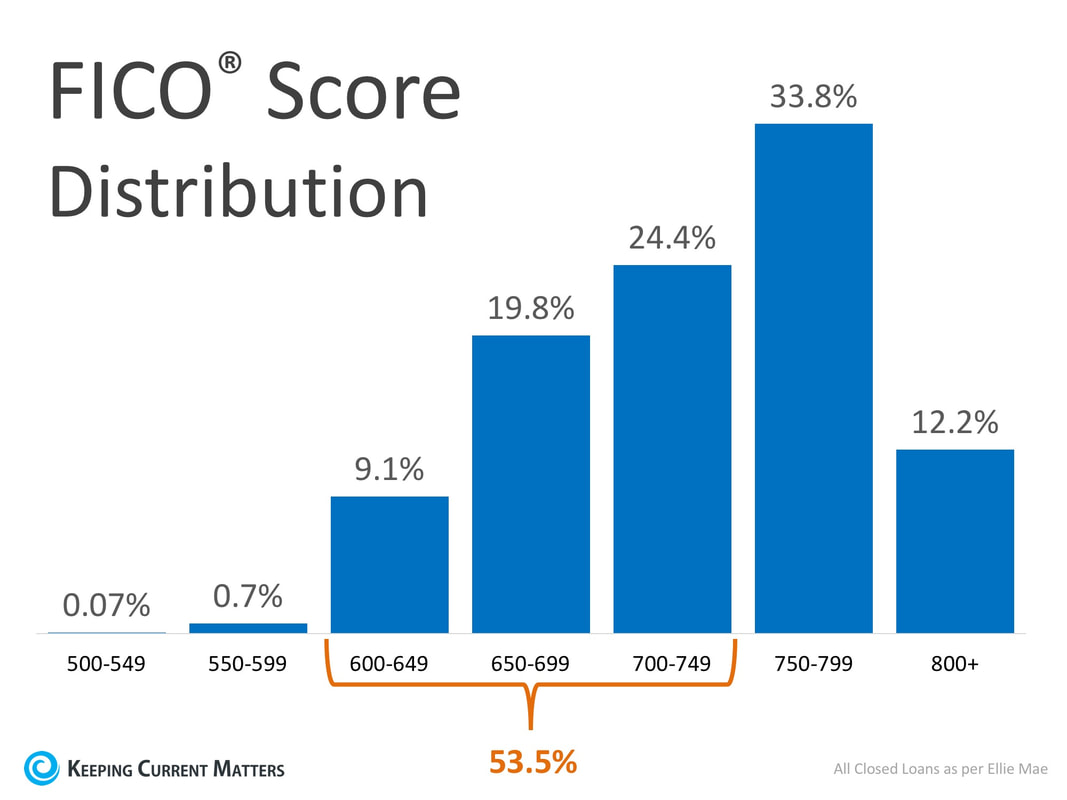

According to a new study from Lending Tree, Americans who have filed for bankruptcy may be able to rebuild enough credit to qualify for a home loan in as little as 2-3 years. This is in stark contrast to the belief that many have that they need to wait 7-10 years for their bankruptcies to clear from their credit reports before attempting to apply for either a mortgage or a personal or auto loan. The study analyzed over one million loan applications for mortgages, personal, and auto loans and compared borrowers who had a bankruptcy on their credit report vs. those who did not to find out the “Cost of Bankruptcy.” The study found that 43.2% of Americans who filed bankruptcy were able to repair their credit back to a 640 FICO® Score in less than a year. The percentage of those who achieved a 640 FICO® Score increased to nearly 75% after 5 years. The full breakdown of the findings was used to create the chart below  Americans who were able to repair their credit scores to a range of 720-739 within three years of filing were able to obtain the same financing options as those who had never filed bankruptcy. According to Ellie Mae’s latest Origination Insights Report, 53.5% of those who were approved for a home loan had FICO® Scores between 600-749 last month. This is great news for Americans who are looking to re-enter the housing market.  Raj Patel, Lending Tree’s Director of Credit Restoration & Debt-Related Services had this to say:

“People may think that filing a bankruptcy would put you out of the loan market for seven to ten years, but this study shows that it is possible to rebuild your credit to a good credit quality.” “LendingTree’s research found that very few bankruptcy filers have a harder time [obtaining a mortgage] than those who have not filed for bankruptcy.” Bottom Line If you are one of the millions of Americans who has filed for bankruptcy and think that you have to wait 7-10 years to make your dream of returning to homeownership a reality, meet with a local real estate professional who can help you find out if you qualify now. SOURCE KCM #BuyingMyths #ForBuyers #SimardRealtyGroup #eXpRealty

0 Comments

How do you select the members of your team who are going to help make your dream of owning a home a reality? What should you be looking for? How do you know if you’ve found the right agent or lender?

The most important characteristic that you should be looking for in your agent is someone who is going to take the time to really educate you on the choices available to you and your ability to buy in today’s market. As the financial guru Dave Ramsey advises: “When getting help with money, whether it’s insurance, real estate or investments, you should always look for someone with the heart of a teacher, not the heart of a salesman.” Do your research. Ask your friends and family for recommendations of professionals they’ve worked with in the past and have had good experiences with. Look for members of your team who will be honest and trustworthy; after all, you will be trusting them to help you make one of the biggest financial decisions of your life. Whether this is your first or fifth time buying a home, you want to make sure that you have an agent who is going to have the tough conversations with you, not just the easy ones. If your offer isn’t accepted by the seller, or they think that there may be something wrong with the home that you’ve fallen in love with, you would rather know what they think than make a costly mistake. According to the Home Buyer and Seller Generational Trends Report: “Buyers from all generations primarily wanted their agent’s help to find the right home to purchase. Buyers were also looking for help to negotiate the terms of sale and to help with price negotiations.” Additionally, “Help understanding the purchase process was most beneficial to buyers 37 years and younger at 75 percent.” Look for someone to invest in your family’s future with you. You want an agent who isn’t focused on the transaction but is instead focused on helping you understand the process while helping you find your dream home. Bottom Line In this world of Google searches, where it seems like all the answers are just a mouse-click away, you need an agent who is going to educate you and share the information that you need to know before you even know you need it. SOURCE KCM #ForBuyers #ForSellers #RealEstateTeam #SimardRealtyGroup #eXpRealty  Owning a home has great financial benefits, yet many continue to rent! Today, let’s look at the financial reasons why owning a home of your own has been a part of the American Dream for as long as America has existed.

Realtor.com recently reported that: “Buying remains the more attractive option in the long term – that remains the American dream, and it’s true in many markets where renting has become really the shortsighted option… as people get more savings in their pockets, buying becomes the better option.” What proof exists that owning is financially better than renting?1. In a previous blog we highlighted the top 5 financial benefits of homeownership:

2. Studies have shown that a homeowner’s net worth is 44x greater than that of a renter. 3. Just a few months ago, we explained that a family that purchased an average-priced home at the beginning of 2018 could build more than $44,000 in family wealth over the next five years. 4. Some argue that renting eliminates the cost of taxes and home repairs, but every potential renter must realize that all the expenses the landlord incurs are already baked into the rent payment– along with a profit margin!! Bottom Line Owning a home has always been, and will always be, better from a financial standpoint than renting. SOURCE KCM #ForBuyers #SimardRealtyGroup #eXpRealty |

Archives

October 2022

Categories

All

|

RSS Feed

RSS Feed