This year started strong for real estate, but then the market began to soften. Home inventory in the starter and move-up categories dwindled to almost nothing, mortgage rates were projected to rise, and home sales had decreased for several months in a row.

To many, the outlook heading into 2019 appeared dim… at best. Then, in a 24-hour window last week, things seemed to change. On Wednesday, the National Association of Realtors’ (NAR) revealed in their Existing Homes Sales Report that home sales had INCREASED for the second consecutive month. The next day, NAR’s economic research team announced that the percentage of first-time buyers in the market was higher than last month and even higher than a year ago. What happened to turn around the downward momentum in the market? You only needed to wait a few hours to find out. On the heels of NAR’s revelations, Zillow released their November Real Estate Market Report that explained: “After nearly four years of annual declines in inventory, the number of homes for sale has now increased year-over-year for three straight months…” Ending 2018, we now know two things:

But, what about those pesky interest rates? Last Thursday (the day after all of the above news), Freddie Mac announced that mortgage rates did not increase but instead decreased…again. From their release: “The response to the recent decline in mortgage rates is already being felt in the housing market. After declining for six consecutive months, existing home sales finally rose in October and November and are essentially at the same level as during the summer months. This modest rebound in sales indicates that homebuyers are very sensitive to mortgage rate changes – and given the further drop in rates we’ve seen this month, we expect to see a modest rebound in home sales as well.” Bottom Line Will 2019 start out better than many have predicted? Perhaps, but we’ll have to wait and see. Things do look much better today, though, than they did just a month ago. SOURCE KCM #FirstTimeBuyer #HousingMarketUpdates #SimardRealtyGroup #eXpRealty

0 Comments

One of the most common loans you can get to buy a home is a 30-year fixed rate mortgage. If the thought of paying for your home over the course of 30-years seems daunting, here are some easy ways to shorten that term which will actually end up saving you money over the life of your loan.

Any additional payments to the principal amount (the original sum of money borrowed in a loan), helps to cut down the amount of interest that you will pay over the life of your loan and can also help to shave years off the loan as well. When you make ‘extra’ payments toward your loan, the key is to let your lender/bank know that you want the extra funds to go toward your principal balance as they will not automatically do this for you. You don’t have to double your mortgage payment to make a big difference either! If you have a 30-year mortgage on a median-priced home ($250,000) with a 5% interest rate, you’ll be responsible for a $1,342.05 monthly principal and interest payment. Over the course of the loan, if you pay your exact monthly payment, you will have paid $233,133.89 in interest alone! Paying a Little Extra Can Pay Off Big 1. Pay an additional 1/12th of your mortgage payment every month Benefit: In the example above, adding $111.84 to your monthly mortgage payment might not seem like a lot, but each year you will have paid one extra month’s worth of payments which will shorten the term of your loan by 4 years and 8 months, all while saving you $42,000 in interest! 2. Pay an additional $50 per month towards your mortgage Benefit: Fifty dollars might not seem like enough to make a difference on the term of your loan, but that small amount will save you over $21,000 in interest and will take over 2 years off the end of your loan. Twenty-eight years from now, you’ll be happy to pay off your loan that much sooner! 3. Make one-time lump sum payments when you can Benefit: If you find yourself with a little extra money after a yearly bonus, a tax return, or from investment dividends, paying that money towards the principal can cut your costs. This option, however, is less predictable than the extra monthly payments. If you have higher interest debts, like credit cards, consider using any extra funds you have to pay those debts down before applying that money towards your mortgage. Also, if you do not plan on staying in your home for more than 10 years, paying extra toward your mortgage might not make sense. Bottom Line If you’re wondering what strategies would work best for you to shorten the term of your loan, consult a local real estate professional who can answer your questions or connect you with someone who can. SOURCE KCM #InterestRates #ForBuyers #SimardRealtyGroup #eXpRealty

The price of any item is determined by the supply of that item, as well as the demand for that item in its market. The same is true in real estate. As the inventory of homes available for sale shrinks, and the demand that buyers have for those homes continues to grow, prices increase. Let's get together to discuss the supply and demand of homes in our market!

Some Highlights:

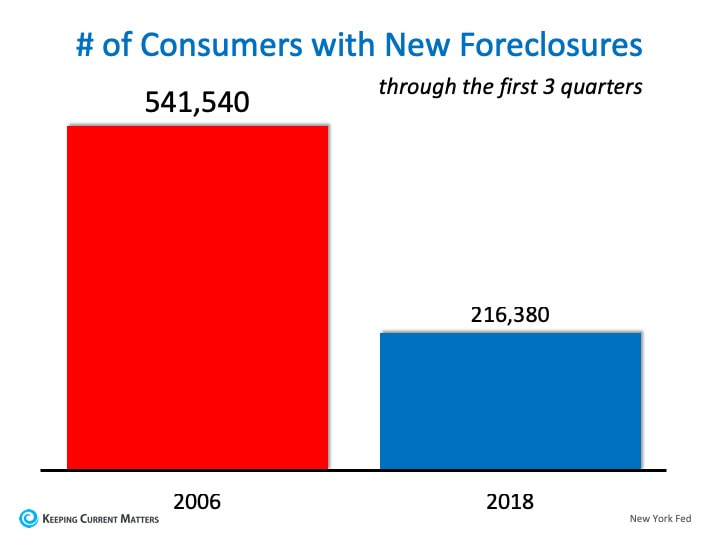

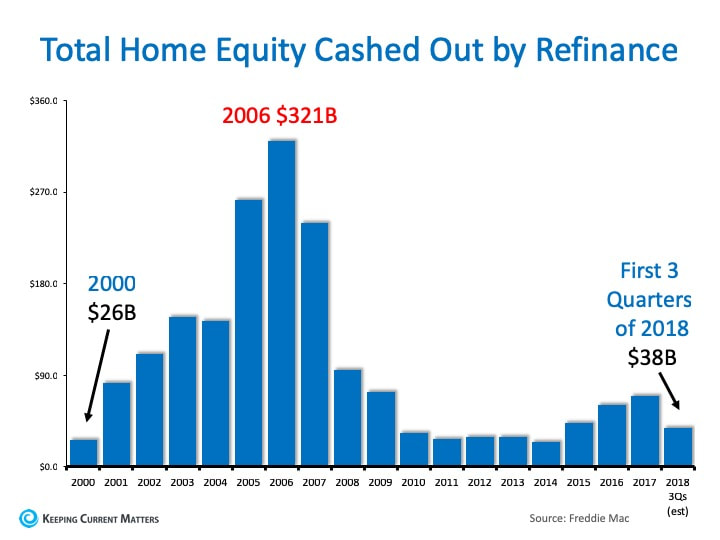

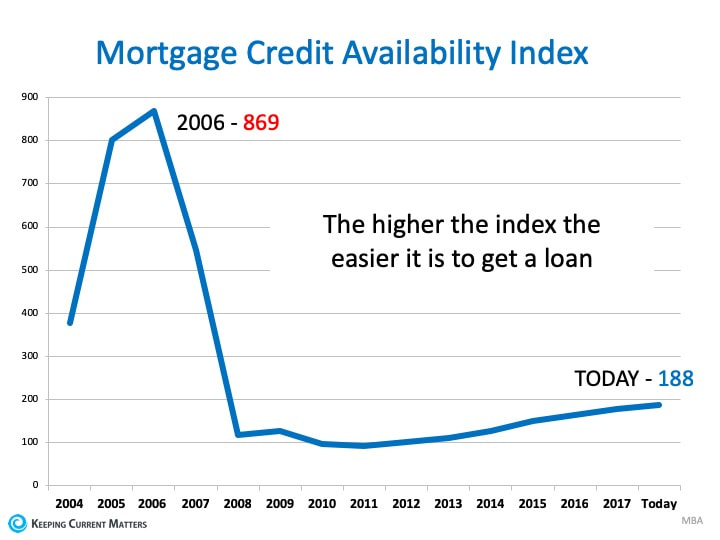

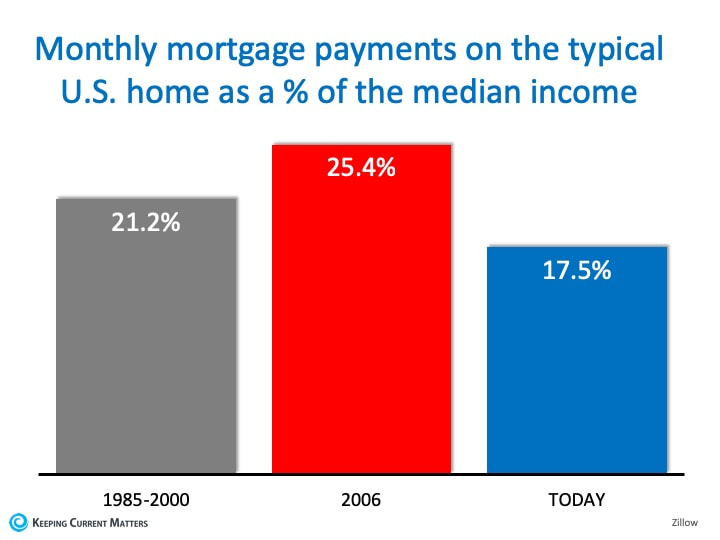

SOURCE KCM #ForBuyers #ForSellers #SimardRealtyGroup #eXpRealty  There is a lot of uncertainty regarding the real estate market heading into 2019. That uncertainty has raised concerns that we may be headed toward another housing crash like the one we experienced a decade ago. Here are four reasons why today’s market is much different: 1. There are fewer foreclosures now than there were in 2006 A major challenge in 2006 was the number of foreclosures. There will always be foreclosures, but they spiked by over 100% prior to the crash. Foreclosures sold at a discount and, in many cases, lowered the values of adjacent homes. We are ending 2018 with foreclosures at historic pre-crash numbers – much fewer foreclosures than we ended 2006 with.  2. Most homeowners have tremendous equity in their homes Ten years ago, many homeowners irrationally converted much, if not all, of their equity into cash with a cash-out refinance. When foreclosures rose and prices fell, they found themselves in a negative equity situation where their homes were worth less than their mortgage amounts. Many just walked away from their houses which led to even more foreclosures entering the market. Today is different. Over forty-eight percent of homeowners have at least 50% equity in their homes and they are not extracting their equity at the same rates they did in 2006.  3. Lending standards are much tougher One of the causes of the crash ten years ago was that lending standards were almost non-existent. NINJA loans (no income, no job, and no assets) no longer exist. ARMs (adjustable rate mortgages) still exist but only as a fraction of the number from a decade ago. Though mortgage standards have loosened somewhat during the last few years, we are nowhere near the standards that helped create the housing crisis ten years ago.  4. Affordability is better now than in 2006 Though it is difficult to afford a home for many Americans, data shows that it is more affordable to purchase a home now than it was from 1985 to 2000. And, it requires much less of a percentage of your income today than it did in 2006.  Bottom Line

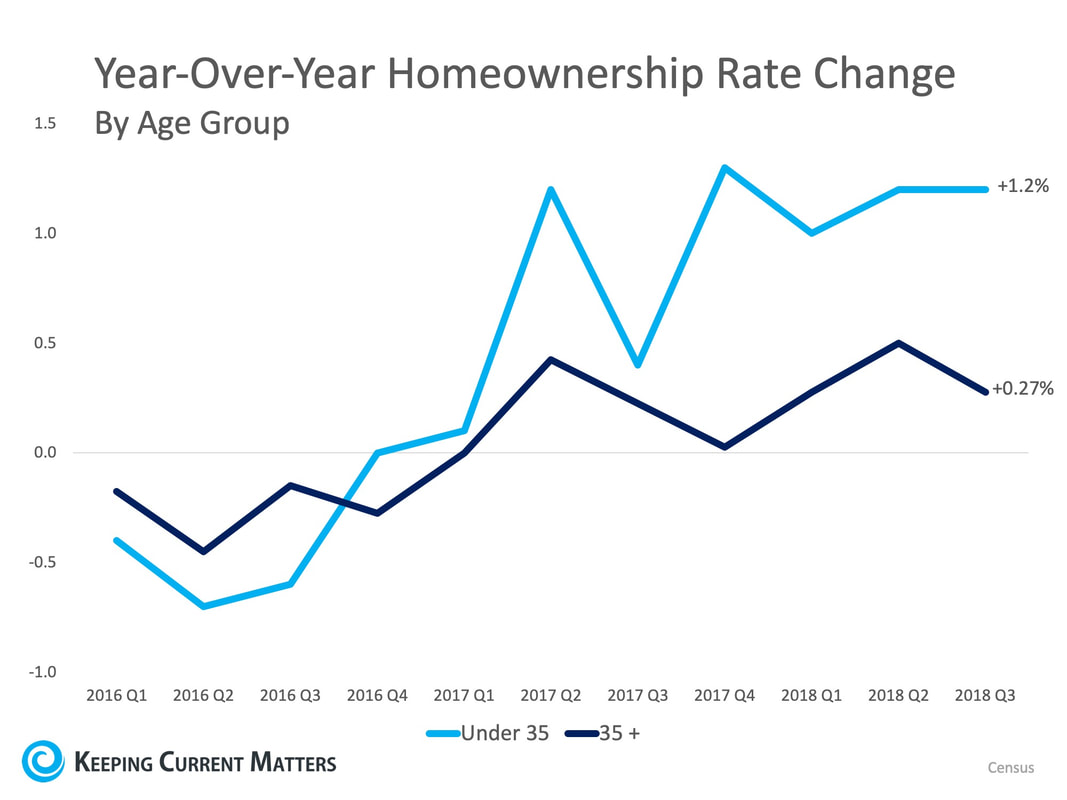

The housing industry is facing some rough waters heading into 2019. However, the graphs above show that the market is much healthier than it was prior to the crash ten years ago. SOURCE KCM #ForBuyers #ForSellers #SimardRealtyGroup #eXpRealty  As we head into 2019, many news outlets and housing experts warn that the housing market may slow down. Over the last six years, the inventory of homes for sale has been near historic lows, which has been the force behind increasing home prices. This has been great news for sellers as many of them have been able to capitalize on the demand in the market and sell their homes quickly and at a great profit. One of the big reasons why inventory has remained so low for so long is that an entire generation of home buyers is finally buying! The millennial generation (ages 19-35) has been the driving force behind bidding wars in many areas of the country as they ditch their renter lifestyles and put down roots in new communities. First American recently released a study entitled “How ‘Renter’ Millennials Will Transform the Housing Market.”In their study, they explained that: “…As more millennials age into their early-to-mid thirties, and begin to get married, have children and form households, they will continue to be the primary drivers of homeownership demand.” Because of this, it is safe to say that one aspect of 2019’s housing market that WILL NOT slow down is the demand for housing from young renters who are no longer satisfied living in someone else’s homes. According to the latest Housing Vacancies and Homeownership Report from the Census Bureau, home buyers under 35 are already out-buying older Americans. The chart below shows the year-over-year change in homeownership rate by those under and over the age of 35.  The national homeownership rate spiked to its highest level in 2004 and then steadily declined until the second quarter of 2016 when it reversed course. Homebuyers under the age of 35 are the reason for that shift.

More than half of the purchase mortgages originated by Fannie Mae and Freddie Mac in 2018 were to first-time homebuyers. In fact, “according to Census Bureau and First American calculations, over the next 10 years, aging millennials are expected to purchase at least 10 million new homes. By 2060, it is estimated millennials will have produced more than 20 million first-time home buyers.” Bottom Line If you are a homeowner who is nervous that the demand for your home will slow, don’t worry! If your home is priced competitively, there will be demand for years to come as this generation of renters is finally able to buy! SOURCE KCM #FirstTimeHomeBuyers #SimardRealtyGroup #eXpRealty  As we approach the end of the year, many homeowners find themselves asking the question, “If we’re currently in a strong real estate market, why won’t my house sell?”

Below are the 5 most common reasons why a listing contract will expire: 1. The Price Sometimes when the market is hot, homeowners attempt to set their listing price higher. Their hope is that a motivated buyer will be willing to pay any price for a house in their desired neighborhood! Sellers must remember, though, that in today’s market a house must be sold twice; first to the buyer and then to their bank. A buyer can agree to pay the homeowner’s asking price, but after the bank conducts their appraisal, the price might need to be adjusted. The bank will only give the buyer a mortgage for the value of determined in the appraisal. Sellers must also keep in mind that today’s homebuyers are well-educated. Before they look to buy a house, they have already seen many houses online. They’ve done their research on the neighborhoods they are interested in, including information on the school districts in the area. They will know if your house seems overpriced and will not waste their time considering it. This is why it’s so important to make sure that your home is priced right from day one on the market! 2. The Condition of the House In many areas, builders are taking advantage of the lack of inventory of homes for sale by building new houses. These newly constructed homes create competition for existing homes in the market. For this reason, many homeowners are making renovations and updates to their homes to compete with the new construction in their marketplace. Most agents recommend that homeowners declutter their houses before putting them on the market. Buyers want to be able to imagine themselves living in the home instead of focusing on the current homeowner’s decor. It’s important to take care of the small problems like dripping faucets and torn screens, while also remembering to remove any posters hanging in your teenager’s bedroom. Making sure your home is in perfect condition will make buyers fall in love with it and will ultimately help you get the right price for your house! 3. Seller’s Motivation Why did the seller put their house on the market in the first place? Is the seller’s motivation still the same as it was when they first listed? If homeowners are really motivated to sell, they will make sure their houses are both priced right and in good condition. The seller’s motivation will push them to consider all offers and help them make the right decision for their family’s future. 4. Marketing Plan Having a marketing plan is important! According to NAR’s 2018 Profile of Home Buyers and Sellers, 95% of buyers searched online for a home last year. The days of looking for a newspaper ad or yard sign in your preferred neighborhood are over. If you want to sell your home, you need a real estate professional who understands your local market and knows how to promote your home online. Something as simple as using pictures taken by a professional photographer can make a huge impact in advertising your home! 5. Lack of Communication with Your Agent Keeping an open line of communication with your agent is crucial in getting your home sold with the least amount of hassles, in the right amount of time, and for the right price! From the beginning, establish a continuous line of communication with your agent, and make sure you review your agreement often to see if any changes need to be made. For example, adjusting the selling price! Bottom Line There are houses selling every single day because they are listed at the right price, have the right marketing plan, and are staged for the sale. If for some reason your home didn’t sell and you’re still motivated to get it sold, contact a local real estate professional who can help you figure out the reason your house isn’t selling! SOURCE KCM #ForSellers #MoveUpBuyers #SimardRealtyGroup #eXpRealty  Some Highlights:

SOURCE KCM #ForSellers #Infographics #SimardRealtyGroup #eXpRealty

Waiting until spring to list your house no longer makes sense. Most listings come to market between April and June, so waiting to list means you'll be met with a ton of competition. Let's get together today to discuss why it makes more sense to list your house now!

|

Archives

October 2022

Categories

All

|

RSS Feed

RSS Feed