When it comes to talking about millennials, there are many stereotypes out there that have influenced the way the public feels about the generation. Whether it’s the assumption that millennials are irresponsible with money and would rather buy avocado toast than save for a down payment, or that millennials jump from job to job, the majority of these stereotypes paint the generation in a negative light.

A new study by Bank of America entitled Better Money Habits Millennial Report recently came to the defense of the generation when it reported that: “Millennials deserve more credit – both from themselves and from others – for their mindfulness when it comes to money and their lives.” Here are some key takeaways from the study proving that millennials deserve more credit for what they are already doing:

Many have wondered if millennials even want to own their own homes or if they would choose to rent instead. Well, not only do they want to own their own homes, but many already do and are looking to trade up! A recent study by realtor.com shows that 49% of Americans who plan to sell their home in the next 12 months are millennials! Danielle Hale, realtor.com’s Chief Economist, gave some insight into why millennials are looking to sell, “The housing shortage forced many first-time homebuyers to consider smaller homes and condos as a way to literally get their foot in the door. Our survey data reveals that we may see more of these homes hitting the market in the next year.” Bottom Line Not every millennial fits into the stereotypes that are so prominent in our society. Those who have risen above the stereotype are ready and willing to buy a home of their own, and many others already have. SOURCE KCM #ForBuyers #ForSellers #SimardRealtyGroup #ExpRealty

0 Comments

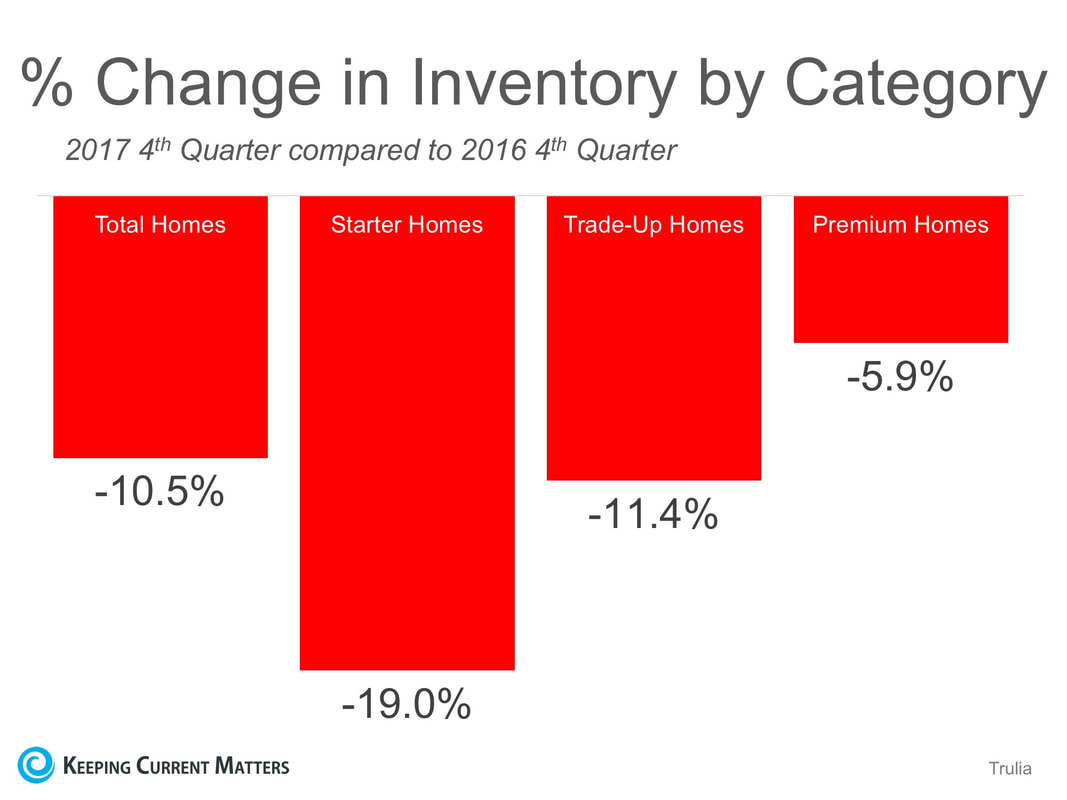

Every winter, families across the country decide if this will be the year that they sell their current houses and move into their dream homes. Mortgage rates hovered around 4% for all of 2017 which forced many buyers off the fence and into the market, resulting in incredibly strong demand RIGHT NOW! At the same time, however, inventory levels of homes for sale have dropped dramatically as compared to this time last year. Trulia reported that “in Q4 2017, U.S. home inventory decreased by 10.5%. That is the biggest drop we’ve seen since Q2 2013.” Here is a chart showing the decrease in inventory levels by category:  The largest drop in inventory was in the starter home category which saw a 19% dip in listings.

Bottom Line Demand for your home is very strong right now while your competition (other homes for sale) is at a historically low level. If you are thinking of selling in 2018, now may be the perfect time. SOURCE KCM #ForSellers #ListYourHouseToday #SimardRealtyGroup #ExpRealty  Some Highlights:

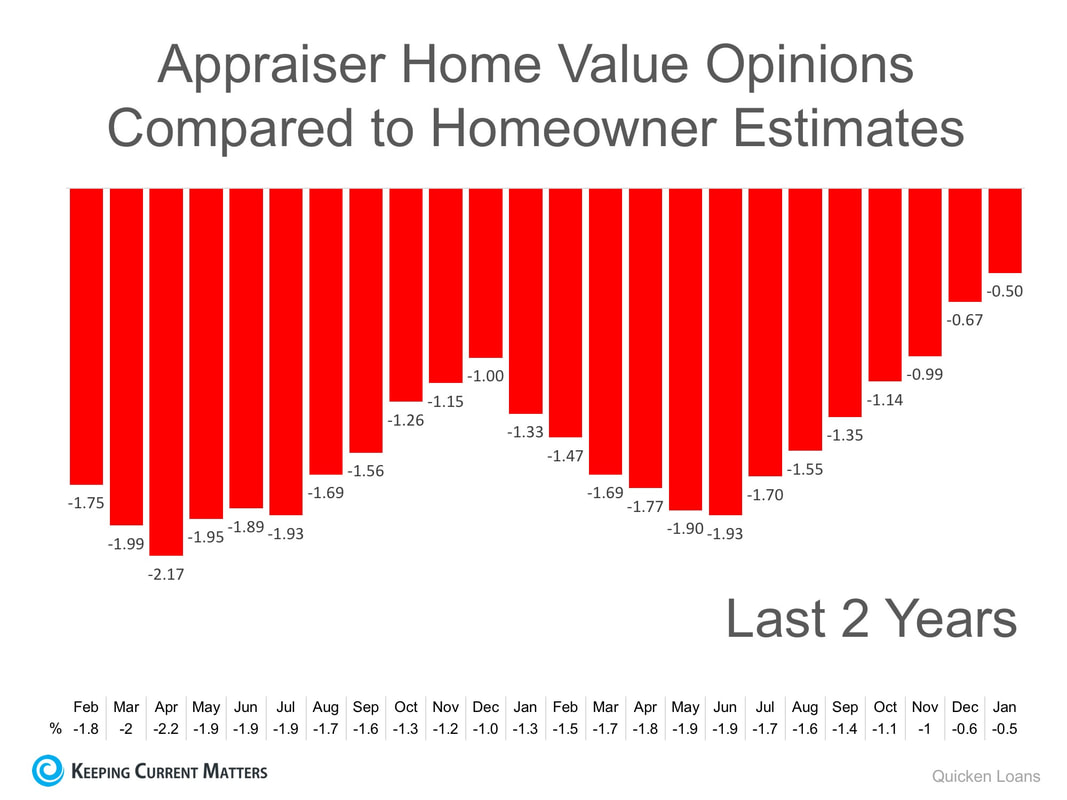

SOURCE KCM #ForBuyers #Infographics #SimardRealtyGroup #JoinExpRealty  In today’s housing market, where supply is very low and demand is very high, home values are increasing rapidly. Many experts are projecting that home values could appreciate by another 4% or more over the next twelve months. One major challenge in such a market is the bank appraisal. When prices are surging, it is difficult for appraisers to find adequate, comparable sales (similar houses in the neighborhood that recently closed) to defend the selling price when performing the appraisal for the bank. Every month in their Home Price Perception Index (HPPI), Quicken Loans measures the disparity between what a homeowner who is seeking to refinance their home believes their house is worth and what an appraiser’s evaluation of that same home is. In the latest release, the disparity was the narrowest it has been in over two years, as the gap between appraisers and homeowners was only -0.5%. This is important for homeowners to note as even a .5% difference in appraisal can mean thousands of dollars that a buyer or seller would have to come up with at closing (depending on the price of the home) The chart below illustrates the changes in home price estimates over the last two years.  Bill Banfield, Executive VP of Capital Markets at Quicken Loans urges homeowners to find out how their local markets have been impacted by supply and demand:

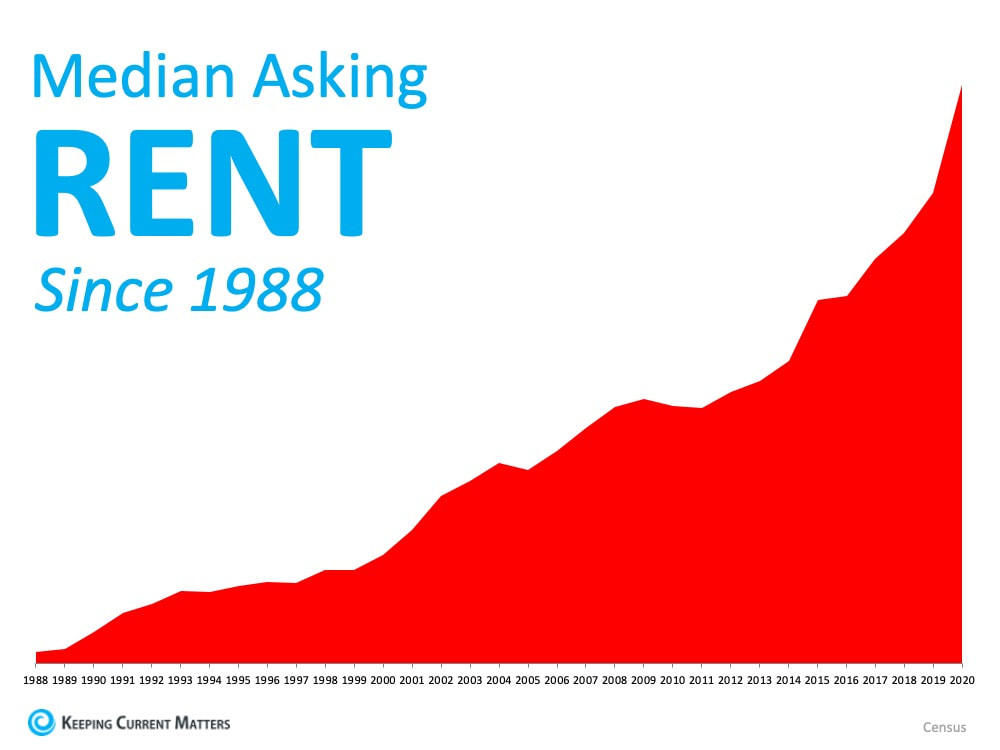

“Appraisers and real estate professionals evaluate their local housing markets daily. Homeowners, on the other hand, may only think about their housing market when they see ‘for sale’ signs hit front yards in the spring or when they think about accessing their equity.” “With several years of growth, owners may have more equity than they realize. Many consumers use the tax season at the beginning of the year to reevaluate their entire financial life. It also provides a good opportunity for them to consider how best to take advantage of their equity while mortgage interest rates and borrowing costs are still near record lows.” Bottom Line Every house on the market must be sold twice; once to a prospective buyer and then to the bank (through the bank’s appraisal). With escalating prices, the second sale might be even more difficult than the first. If you are planning on entering the housing market this year, meet with an experienced professional who can guide you through this and any other obstacles that may arise. SOURCE KCM #ForSellers #Pricing #SimardRealtyGroup #JoinExpRealty  According to ATTOM Data Solutions’ 2018 Rental Affordability Report, “buying a median-priced home is more affordable than renting a three-bedroom property in 240 of 447 [or 54% of] U.S. counties analyzed for the report.”

For the report, ATTOM Data Solutions compared recently released fair market rent data from the Department of Housing and Urban Development with reported income amounts from the Department of Labor and Statistics to determine the percentage of income that a family would have to spend on their monthly housing cost (rent or mortgage payments). Daren Blomquist, Senior Vice President of ATTOM Data Solutions had this to say: “Although buying is still more affordable than renting in the majority of U.S. housing markets, the majority is shrinking as home price appreciation continues to outpace rental growth in most areas.” However, the report also shows that the average fair market rent rose faster than average weekly wages in 60% of the counties analyzed in the report (266 of 447 counties). With rents rising, many renters should consider buying a home soon. Bottom Line Rents will continue to rise, and mortgage interest rates are still at historic lows. Before you sign or renew your next lease, meet with a local professional who can help you determine if you are able to buy a home of your own and lock in your monthly housing expense. SOURCE KCM #ForBuyers #SimardRealtyGroup #JoinExpRealty Congrats to our buyers! 👍👍👍 #UnderContract #SimardRealtyGroup #joinExpRealty   Some Highlights:

SOURCE KCM #Buyers #Moving #SimardRealtyGroup #ExpRealty  According to the National Association of Realtors’ latest Realtors Confidence Index, 61% of first-time homebuyers purchased their homes with down payments below 6% from October 2016 through November 2017.

Many potential homebuyers believe that a 20% down payment is necessary to buy a home and have disqualified themselves without even trying. The median down payment for all buyers in 2017 was just 10% and that percentage drops to 6% for first-time buyers. Zillow Senior Economist Aaron Terrazas’ recent comments shed light on why buyer demand has remained strong, “Looking into 2018, rent is expected to continue gaining. More widespread rent growth could mean home buying demands stay high, as renters who can afford it move away from the unpredictability of rising rents toward the relative stability of a monthly mortgage payment instead.” It’s no surprise that with rents rising, more and more first-time buyers are taking advantage of low-down-payment mortgage options to secure their monthly housing costs and finally attain their dream homes. Bottom Line If you are one of the many first-time buyers who is not sure if you would qualify for a low-down payment mortgage, consult a local real estate professional who can set you on your path to homeownership! SOURCE KCM #Buyers #DownPayments #SimardRealtyGroup #JoinExpRealty  It is common knowledge that a great number of homes sell during the spring-buying season. For that reason, many homeowners hold off on putting their homes on the market until then. The question is whether or not that will be a good strategy this year. The other listings that do come out in the spring will represent increased competition to any seller. Do a greater number of homes actually come to the market in the spring as compared to the rest of the year? The National Association of Realtors (NAR) recently revealed the months in which most people listed their homes for sale in 2017. Here is a graphic showing the results:  The three months in the second quarter of the year (represented in red) are consistently the most popular months for sellers to list their homes on the market. Last year, the number of homes available for sale in January was 1,680,000.

That number spiked to 1,970,000 by May! What does this mean to you? With the national job situation improving, and mortgage interest rates projected to rise later in the year, buyers are not waiting until the spring; they are out looking for homes right now. If you are looking to sell this year, waiting until the spring to list your home means you will have the greatest competition amongst buyers. Bottom Line It may make sense to beat the rush of housing inventory that will enter the market in the spring and list your home today. SOURCE KCM #ForSellers #SimardRealtyGroup #ExpRealty |

Archives

October 2022

Categories

All

|

RSS Feed

RSS Feed