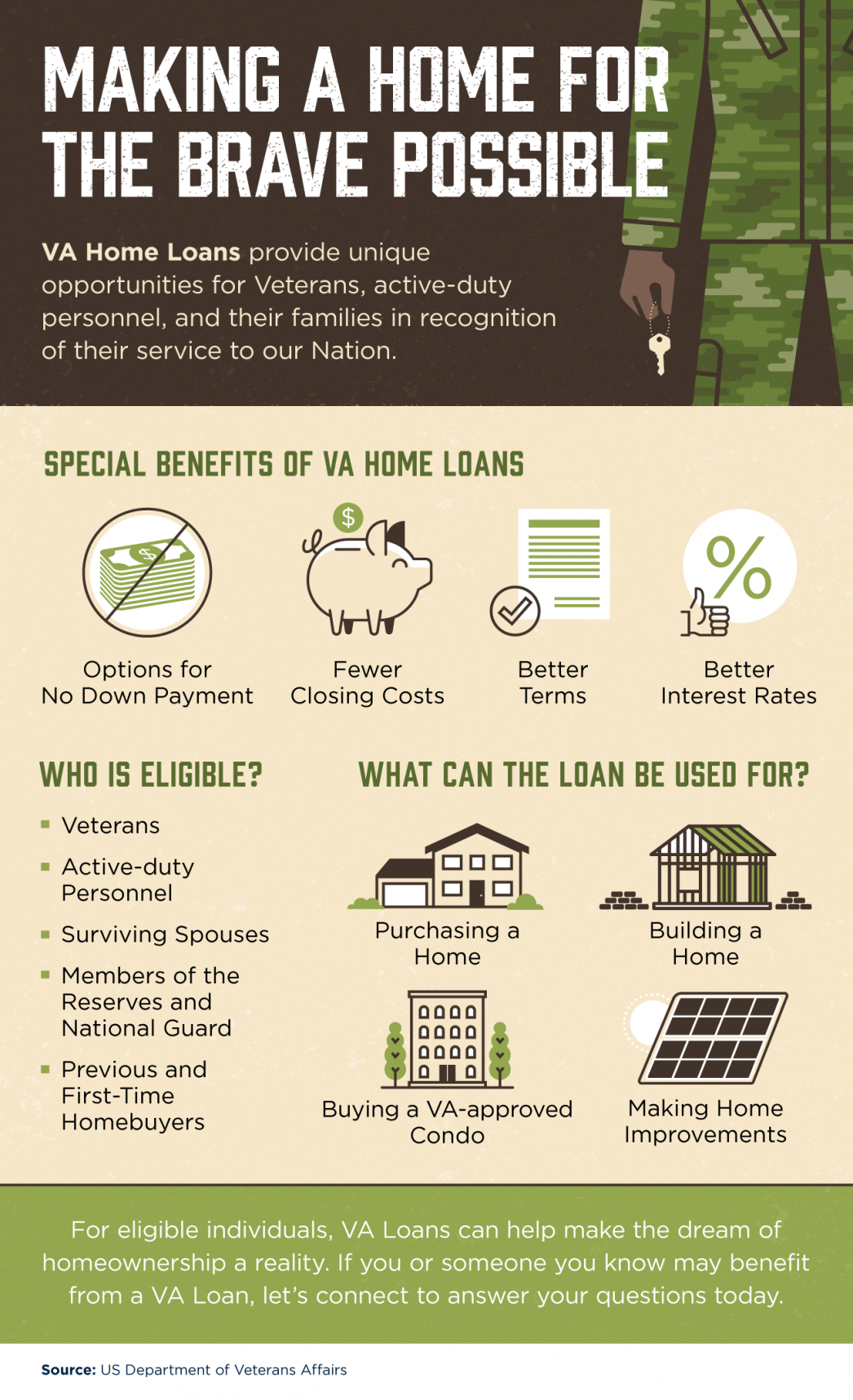

Some Highlights

SOURCE KCM #DownPayments #ForBuyers #InterestRates #SimardRealtyGroup #joineXpRealty

0 Comments

If your current home no longer suits your needs, today’s record-low interest rates mean you may be able to make a move now and stretch your dollar a little further. This is a huge opportunity to get more for your money in the housing market. DM me today to make sure we can find your dream home before mortgage rates start to rise.

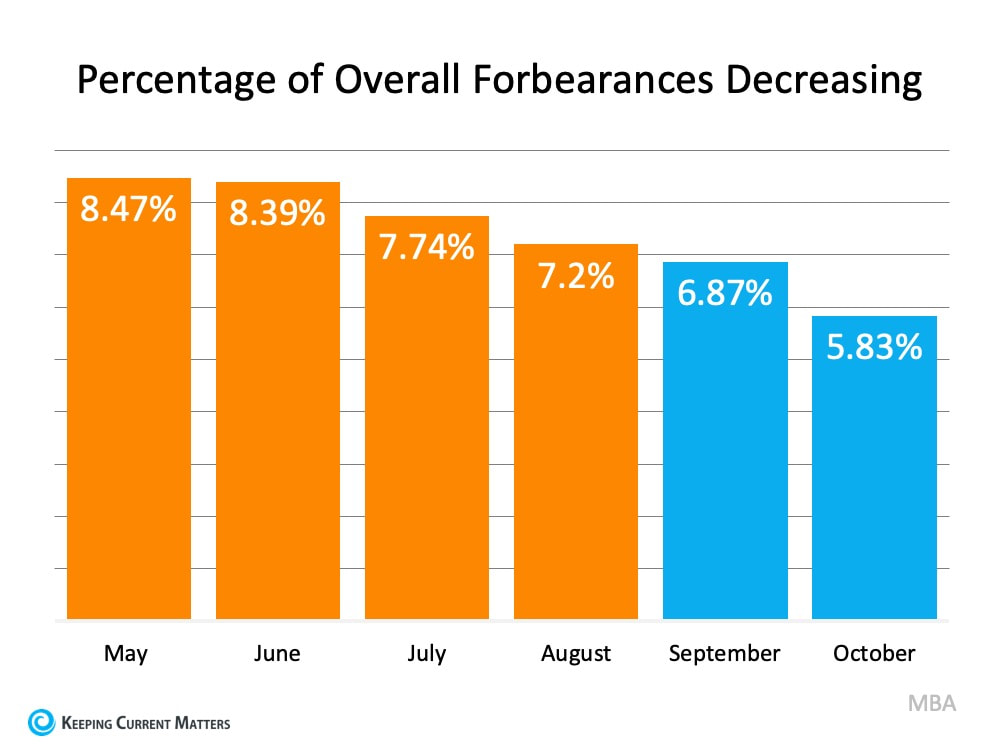

#mortgagerates #homeaffordability #expertanswers #purchasingpower #buyingpower #homepriceappreciation #affordability #realestate #homevalues #homeownership #homebuying #realestatetipsandadvice #keepingcurrentmatters  As the current forbearance mortgage relief options come to an end, many are wondering if we’ll face a foreclosure crisis next year. This is understandable, especially for those who remember the housing crisis that began in 2008. The reality is, plans have been put in place through forbearance to ensure history doesn’t repeat itself. This year, homeowners are able to request 180 days of mortgage relief through forbearance. Upon expiration of that timeframe, they’re also entitled to request 180 additional days, bringing the total to 360 days of deferred payment eligibility. As forbearance expires, homeowners should stay in touch with their lender, because creating a plan for the deferred payments is a critical next step to avoiding foreclosure. There are multiple options for homeowners to pursue at this point, and with the right planning and communication with the lender, foreclosure doesn’t have to be one of them. Many homeowners are concerned that they’ll have to pay the deferred payments back in a lump sum payment at the end of forbearance. Thankfully, that’s not the case. Fannie Mae explains: “You don’t have to repay the forbearance amount all at once upon completion of your forbearance plan…Here’s the important thing to remember: If you receive a forbearance plan, you will have options when it comes to repaying the missed amount. You don’t have to pay the forbearance amount at once unless you are able to do so.” When looking at the percentage of people in forbearance, we can also see that this number has been decreasing steadily throughout the year. Fewer people than initially expected are still in forbearance, so the number of homeowners who will need to work out alternative payment options is declining (See graph below):  This means there are fewer and fewer homeowners at risk of foreclosure, and many who initially applied for forbearance didn’t end up needing it. Mike Fratantoni, Senior Vice President and Chief Economist at the Mortgage Bankers Association (MBA), explains:

“Nearly two-thirds of borrowers who exited forbearance remained current on their payments, repaid their forborne payments, or moved into a payment deferral plan. All of these borrowers have been able to resume – or continue – their pre-pandemic monthly payments.” For those who are still in forbearance and unable to make their payments, foreclosure isn’t the only option left. In their Homeowner Equity Insights Report, CoreLogic indicates: “In the second quarter of 2020, the average homeowner gained approximately $9,800 in equity during the past year.” Many homeowners have enough equity in their homes today to be able to sell their houses instead of foreclosing. Selling and protecting the overall financial investment may be a very solid option for many homeowners. As Ivy Zelman, Founder of Zelman & Associates, mentioned in a recent podcast: “The likelihood of us having a foreclosure crisis again is about zero percent.” Bottom Line If you’re currently in forbearance or think you should be because you’re concerned about being able to make your mortgage payments, reach out to your lender to discuss your options and next steps. Having a trusted and knowledgeable professional on your side to guide you is essential in this process and might be the driving factor that helps you stay in your home. SOURCE KCM #DistressedProperties #ForSellers #ForeClosures #HousingMarketUpdates  Compared to this time last year, houses are pretty much flying off the market at a record-breaking pace. This isn’t just a good time to sell your house – it is THE time to sell it. DM me to learn what to expect and how you can win in today’s sellers’ market.

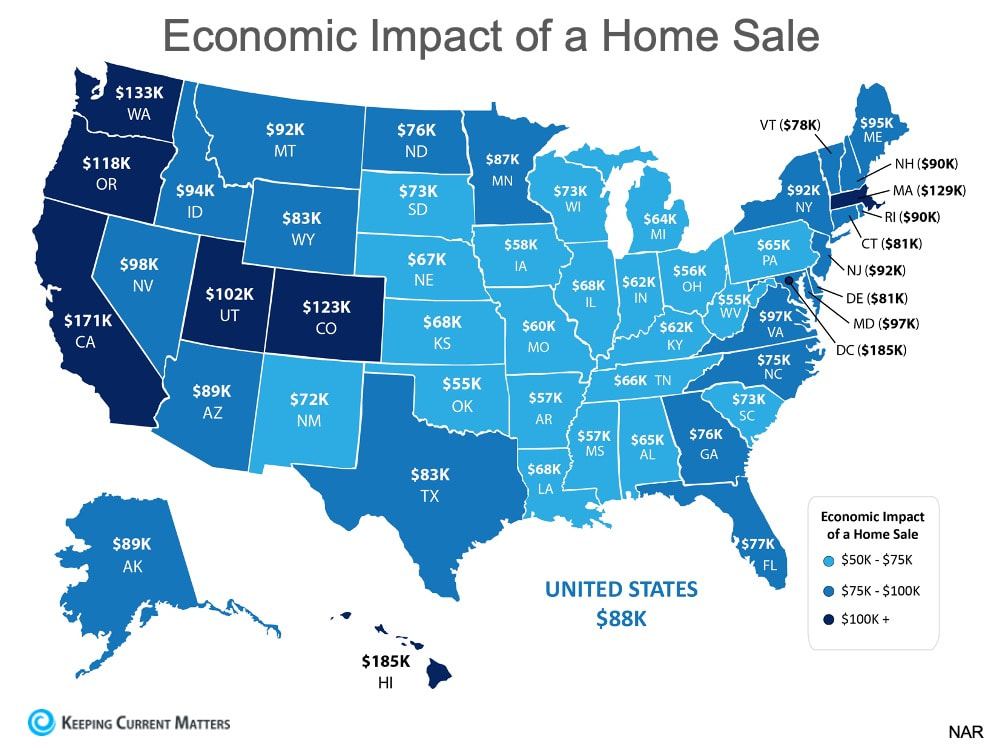

#buyerdemand #sellingyourhouse #expertanswers #stayinformed #staycurrent #powerfuldecisions #confidentdecisions #realestate #realestateexpert #realestateagency #realestateadvice #realestatemarket #instarealestate #keepingcurrentmatters  As the economy recovers from this year’s health crisis, the housing market is playing a leading role in the turnaround. It’s safe to say that what we call “home” is taking on a new meaning, causing many of us to consider buying or selling sooner rather than later. Housing, therefore, has thrived in an otherwise down year. Today’s high buyer demand combined with low housing inventory means we’re seeing home prices appreciate at an above-average pace. This demand is being driven by those who want to take advantage of historically low mortgage rates. According to Freddie Mac: “The record low mortgage rate environment is providing tangible support to the economy at a critical time, as housing continues to propel growth.” These factors are driving a positive impact on the economy as a whole. According to the National Association of Realtors (NAR), the real estate industry provided $3.7 billion dollars of economic impact to the country last year. To break it down, in 2019, the average newly constructed home contributed just over $88,000 per build to local economies. Across the country, real estate clearly makes a significant impact (See map below):  In addition, last week, the Bureau of Economic Analysis announced the U.S. Gross Domestic Product increased at an annual rate of 33.1% in the 3rd quarter of this year, after decreasing by 31.4% in the second quarter. There’s no doubt the growing economy is being fueled in part by the soaring housing market. Experts forecast this housing growth to carry into 2021, continuing to make a big impact on the economy next year as well.

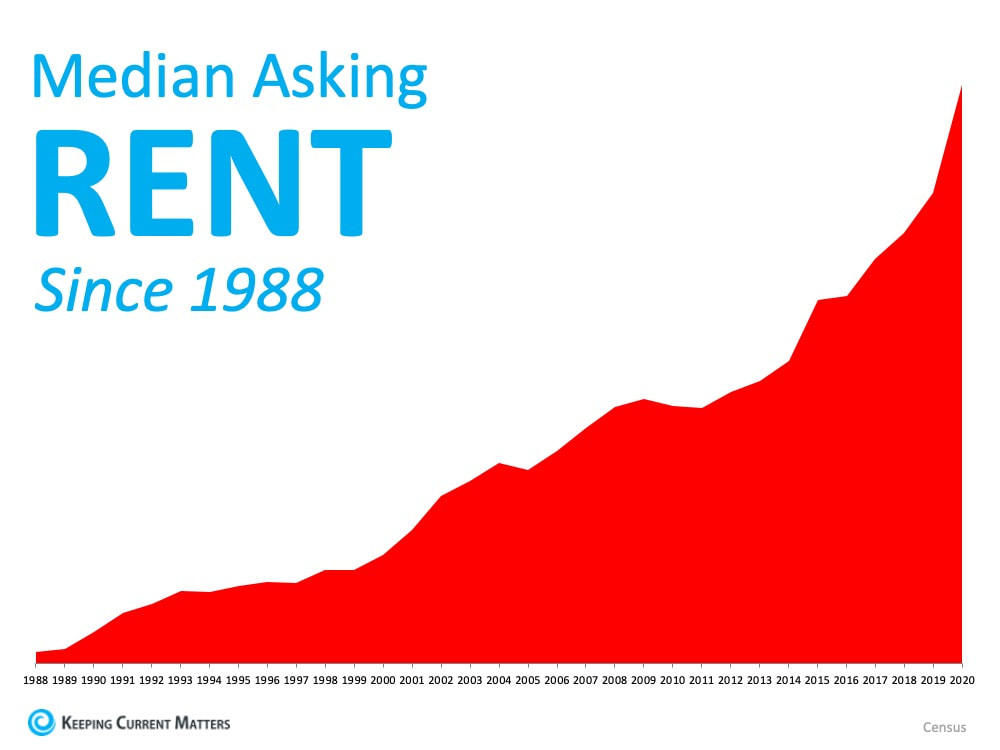

Bottom Line The American Dream of homeownership has continued to thrive in the midst of this year’s economic downturn, and “home” has taken on a new meaning for many of us during this time. Best of all, the housing market is making a significant impact as the economy recovers. #NewConstruction #ForSellers #ForBuyers #SimardRealtyGroup #eXpRealty  According to the U.S. Census Bureau, median rent continues to rise. With today’s low mortgage rates, there’s great opportunity for current renters to make a move into homeownership that stretches each dollar a little bit further. While the best timeline to buy a home is different for everyone, the question remains: Should I continue renting or is it time for me to buy? The answer depends on your current situation and your future plans, so here are some thoughts to help you decide if you’re ready to own a home of your own. 1. Rent Will Continue to Increase This is one of the top reasons why renters decide to move because in most cases, rent will continue increasing each year. As noted above, the U.S. Census Bureau recently released its quarterly homeownership report, and as the graph below shows, median rent is climbing year after year. When you own a home, you’ll lock in your monthly payment for the life of your loan, creating consistency and predictability in your payments.  2. Freedom to Customize

This is a big decision-making point for many people who want to be able to paint, renovate, and make home upgrades. In many cases, landlords determine all of these selections and prefer you do not alter them as a renter. As a homeowner, you have the freedom to decorate and personalize your home to truly make it your own. 3. Privacy When renting, your landlord has access to your space in case of an emergency. If you own your home, however, you’re the one to decide who can come inside. Given today’s health concerns around the pandemic, this may be a growing priority for you. 4. Flexibility for Relocation If you’re renting, it may be easier to move quickly should you have a job transfer or simply decide it’s time for a change. When you’re a homeowner and need to sell your house, this might take a little more time. Today, however, with the housing market’s low inventory, this may no longer be the case. Homes are selling at a record-breaking pace, so you may have more flexibility than you think. 5. Building Equity When you pay your rent, your landlord earns the equity the property gains. If you own your home, the benefits of your investment go directly toward your net worth. This is savings you’ll be able to use in the future for things like sending children to college, starting a new business, buying a bigger home, or simply downsizing to save for retirement. 6. Tax Advantages When you own your home, there are additional that work in your favor as well. You can deduct things like your property taxes and mortgage interest (Always make sure you check with your accountant to see which tax-deductible benefits apply to your situation). When you rent, however, the tax benefits are directed to your landlord. Bottom Line It’s up to you to decide if you’d prefer to rent or buy, and it’s different for every person. If you’d like to learn more about the pros and cons of each, as well as resources to help you along the way, contact a local real estate professional to discuss your options. This way, you can make a confident and informed decision with a trusted expert on your side. SOURCE KCM #BuyingMyths #Pricing #RentVSBuy #SimardRealtyGroup #eXpRealty  Mortgage rates have hit all-time lows over and over again this year, meaning it continues to get less expensive to borrow money for a home loan. DM me if you’re ready to learn more about saving on your next home purchase by taking advantage of today’s low mortgage rates.

#mortgagerates #purchasingpower #buyingpower #expertanswers #interestrates #affordability #realestate #homevalues #homeownership #homebuying #realestategoals #realestatetips #realestatetipsoftheday #realestatetipsandadvice #keepingcurrentmatters  Tomorrow, Americans will decide our President for the next four years. That decision will have a major impact on many aspects of life in this country, but the residential real estate market will not be one of them.

Analysts will try to measure the impact feasible changes in regulations might have on housing, the effect of a possible first-time buyer program, and any number of other situations based on who wins. The housing market, however, will remain strong for four reasons: 1. Demand Is Strong among Millennials The nation’s largest generation began entering the housing market last year as they reached the age to marry and have children – two key drivers of homeownership. As the Wall Street Journal recently reported: “Millennials, long viewed as perennial home renters who were reluctant or unable to buy, are now emerging as a driving force in the U.S. housing market’s recent recovery.” 2. Mortgage Rates Are Historically Low All-time low interest rates are also driving demand across all generations. Strong demand created by this rate drop has countered other economic disruptions (e.g., pandemic, recession, record unemployment). In addition, Freddie Mac just forecasted mortgage rates to remain low through next year: “One of the main drivers of the strong housing recovery is historically low mortgage interest rates…Given weakness in the broader economy, the Federal Reserve’s signal that its policy rate will remain low until inflation picks up, and no signs of inflation, we forecast mortgage rates to remain flat over the next year. From the third quarter of 2020 through the end of 2021, we forecast mortgage rates to remain unchanged at 3%.” 3. Prices Continue to Appreciate The continued lack of supply of existing homes for sale coupled with the surge in buyer demand has experts forecasting strong price appreciation over the next twelve months. 4. History Says So Though it’s true that the market slows slightly in November when it’s a Presidential election year, the pace returns quickly. Here’s an explanation as to why from the Homebuilding Industry Report by BTIG: “This may indicate that potential homebuyers may become more cautious in the face of national election uncertainty. This caution is temporary, and ultimately results in deferred sales, as the economy, jobs, interest rates and consumer confidence all have far more meaningful roles in the home purchase decision than a Presidential election result in the months that follow.” Ali Wolf, Chief Economist for Meyers Research, also notes: “History suggests that the slowdown is largely concentrated in the month of November. In fact, the year after a presidential election is the best of the four-year cycle. This suggests that demand for new housing is not lost because of election uncertainty, rather it gets pushed out to the following year as long as the economy stays on track.” Bottom Line There’s no doubt this is one of the most contentious presidential elections in our nation’s history. The outcome will have a major impact on many sectors of the economy. However, as Matthew Speakman, an economist at Zillow, explained last week: “While the path of the overall economy is likely to be most directly dictated by coronavirus-related and political developments in the coming months, recent trends suggest that the housing market – which has basically withstood every pandemic-related challenge to this point – will continue its strong momentum in the months to come.” SOURCE KCM #InterestRates #Millennials #ForSellers #ForBuyers #SimardRealtyGroup #eXpRealty |

Archives

October 2022

Categories

All

|

RSS Feed

RSS Feed