From a purely economic perspective, this is one of the best times in American history to buy a home. Black Night Financial Services discusses this in their most recent Monthly Mortgage Monitor.

Here are two of the report’s revelations:

The report explains: “Even though the value of the average home in the U.S. increased by about $13,500 over the last year, thanks to declining interest rates it actually costs almost exactly the same in principal and interest each month to purchase as it did this time last year. Even taking into account the fact that affordability can vary – sometimes significantly – across the country based upon the different rates of home price appreciation we’re seeing, that’s a pretty incredible balancing act between interest rates and home prices at the national level… Right now, it takes 20 percent of the median monthly income to cover monthly payments on the median-priced home, which is well below historical norms.” However, the report warns that affordability will be dramatically impacted by an increase in mortgage rates. “A half-point increase in interest rates would be equivalent to a $17,000 jump in the average home price, and bring that ratio to 21.5 percent. This increase is still below historical norms, but puts more pressure on homebuyers.” Bottom Line If you are ready and willing to purchase a home of your own, find out if you’re able to. Now is a great time to jump in. SOURCE KCM #HomeBuyers #ForBuyers #SimardRealtyGroup

0 Comments

The availability of mortgage credit is not at the same level that it was during the boom in housing (2005), and that’s good news. However, the constant headlines which talk about “tight credit” are causing some potential home buyers to doubt their ability to purchase. We want to rectify the misconception of what is required for a down payment in order to purchase a home in today’s market.

Freddie Mac recently discussed the confusion many first-time homebuyers have about the down payment they need in order to buy: “Did you know that the average down payment among first–time homebuyers is 6% and it's 13–14% for repeat buyers…It's possible to put down even less. Many potential homebuyers think that only the FHA helps make mortgage loans with low down payments. Not true. Freddie Mac's Home Possible mortgage products let qualified homebuyers put down as little as 3%.” Brenda Garcia Lemus of John Burns Real Estate Consulting reports that this is also the case with newly constructed homes: “Our home-builder clients sell hundreds of homes every weekend to buyers with 5% down payments and below average credit scores. Yet, many middle-income households with average credit and access to a 5% down payment assume they cannot become homeowners because of the ‘tight credit’ headlines.” Bottom Line Before you ‘disqualify’ yourself, check with a professional in your market to find out what is possible in mortgaging today. SOURCE KCM #Mortgage #MortgageCredit #SimardRealtyGroup  #MarketReport #EastGranby #SimardRealtyGroup

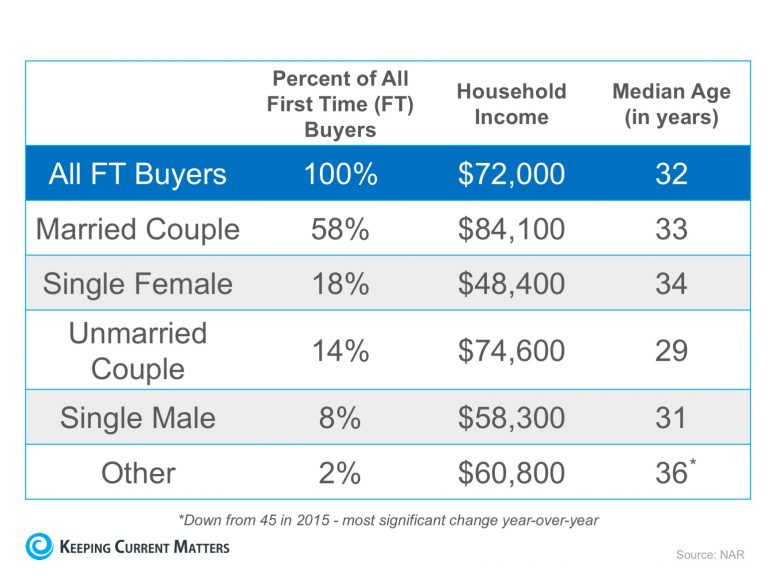

There are many people sitting on the sidelines trying to decide if they should purchase a home or sign a rental lease. Some might wonder if it makes sense to purchase a house before they are married and have a family. Others may think they are too young. And still, others might think their current income would never enable them to qualify for a mortgage. We want to share what the typical first-time homebuyer actually looks like based on the National Association of REALTORS most recent Profile of Home Buyers & Sellers. Here are some interesting statistics on the first-time buyer:  Unmarried couples jumped up to the third spot, right after their married counterparts and single women. Many couples are buying a home before spending what would be a down payment on a wedding.

Bottom Line You may not be much different than many people who have already purchased their first home. Meet with a local real estate professional today who can help determine if your dream home is within your grasp. SOURCE KCM #Buyers #Mortgage #SimardRealtyGroup  We all realize that the best time to sell anything is when demand is high and the supply of that item is limited. The last two major reports issued by the National Association of Realtors (NAR) revealed information that suggests that now continues to be a great time to sell your house.

Let’s look at the data covered by the latest Pending Home Sales Report and Existing Home Sales Report. THE PENDING HOME SALES REPORT The report announced that pending home sales (homes going into contract) are up 2.4% over last year, and have increased year-over-year now for 22 of the last 25 consecutive months. Lawrence Yun, NAR’s Chief Economist, had this to say: "The one major predicament in the housing market is without a doubt the painfully low levels of housing inventory in much of the country. It's leading to home prices outpacing wages, properties selling a lot quicker than a year ago and the home search for many prospective buyers being highly competitive and drawn out because of a shortage of listings at affordable prices." Takeaway: Demand for housing will continue throughout the end of 2016 and into 2017. The seasonal slowdown often felt in the winter months did not occur last winter and shows no signs of returning this year. THE EXISTING HOME SALES REPORT The most important data point revealed in the report was not sales, but was instead the inventory of homes for sale (supply). The report explained:

There were two more interesting comments made by Yun in the report: "Inventory has been extremely tight all year and is unlikely to improve now that the seasonal decline in listings is about to kick in. Unfortunately, there won't be much relief from new home construction, which continues to be grossly inadequate in relation to demand." In real estate, there is a guideline that often applies; when there is less than a 6-month supply of inventory available, we are in a seller’s market and we will see appreciation. Between 6-7 months is a neutral market, where prices will increase at the rate of inflation. More than a 7-month supply means we are in a buyer’s market and should expect depreciation in home values. As Yun notes, we are, and will remain, in a seller’s market with prices still increasing unless more listings come to the market. "There's hope the leap in sales to first-time buyers can stick through the rest of the year and into next spring. The market fundamentals — primarily consistent job gains and affordable mortgage rates — are there for the steady rise in first-timers needed to finally reverse the decline in the homeownership rate." Takeaway: Inventory of homes for sale is still well below the 6-month supply needed for a normal market. Prices will continue to rise if a ‘sizable’ supply does not enter the market. Bottom Line If you are going to sell, now may be the time to take advantage of the ready, willing, and able buyers that are still out looking for your house. SOURCE KCM #ForSellers #HousingMarketUpdates #SimardRealtyGroup  Every Hour in the US Housing Market:

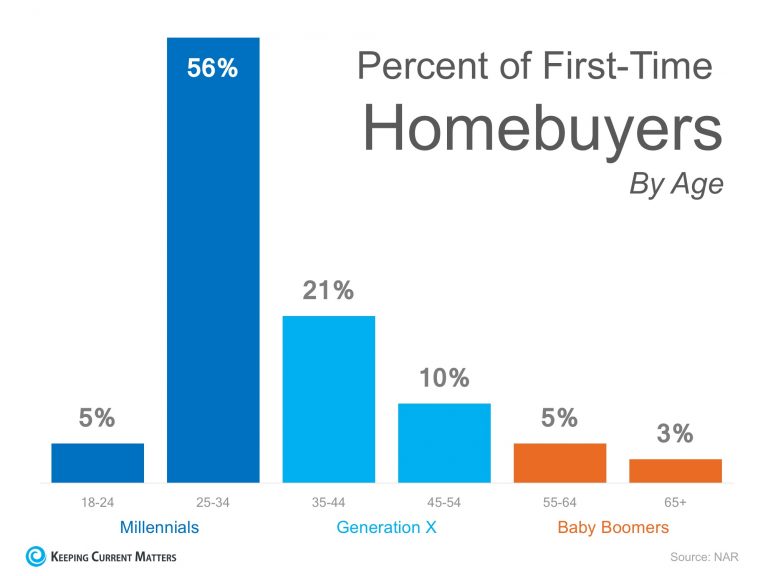

Source KCM #MarketReport #EverySecondCounts #SimardRealtyGroup  According to the Census Bureau, millennials have overtaken baby boomers as the largest generation in U.S. History. Millennials, or America's youth born between 1982-2000, now represent more than one quarter of the nation’s population, totaling 83.1 million. There has been a lot of talk about how, as a generation, millennials have ‘failed to launch’ into adulthood and have delayed moving out of their family’s home. Some experts have even questioned whether or not millennials want to move out. The great news is that not only do millennials want to move out… they are moving out! The National Association of Realtors (NAR) recently released their 2016 Profile of Home Buyers and Sellers in which they revealed that 61% of all first-time homebuyers were millennials in 2015! The median age of all first-time buyers in 2015 was 31 years old. Here is chart showing the breakdown by age:  Many social factors have contributed to millennials waiting to buy their first home. The latest Census results show that the median age of Americans at the time of their first marriage has increased significantly over the last 60 years, from 23 for men & 20 for women in 1955, to 29 & 27, respectively, in 2015.

Those who went to college and took out student loans are finally paying them off, as the terms on traditional student loans are 10 years. This means that a large portion of the generation is making its last loan payments and is working toward saving for a first home. As a whole, the first-time homebuyer share increased to 35% of all buyers, up from 32% in 2014. Not all millennials are first-time buyers, they also made up 12% of all repeat buyers! Bottom Line Millennials will continue to drive the housing market next year, as well as in the years to come. As more and more realize that owning a home is within their grasp, they will flock to own their piece of the American Dream. Are you ready to buy your first or even second home? SOURCE KCM #HomeBuyers #Millenials #SimardRealtyGroup  Price improvement for this move in ready Manchester home.

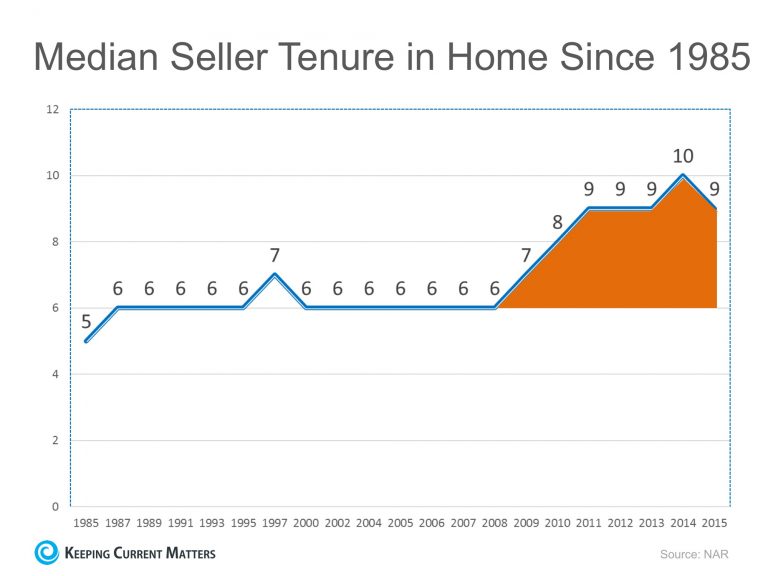

View full info: http://14walekfarmsroad.thebestlisting.com/ #PriceImproved #Manchester #SellingCT #SimardRealtyGroup  The National Association of Realtors (NAR) keeps historic data on many aspects of homeownership. One of the data points that has changed dramatically is the median tenure of a family in a home. As the graph below shows, for over twenty years (1985-2008), the median tenure averaged exactly six years. However, since 2008, that average is almost nine years – an increase of almost 50%.  Why the dramatic increase?

The reasons for this change are plentiful. The top two reasons are:

However, with home prices rising dramatically over the last several years, over 90% of homes with a mortgage are now in a positive equity situation with 70% of them having at least 20% equity. And, with the economy coming back and wages starting to increase, many homeowners are in a much better financial situation than they were just a few short years ago. What does this mean for housing? Many believe that a large portion of homeowners are not in a house that is best for their current family circumstances. They could be baby boomers living in an empty, four-bedroom colonial, or a millennial couple planning to start a family that currently lives in a one-bedroom condo. These homeowners are ready to make a move. Since the lack of housing inventory is a major challenge in the current housing market, this could be great news. SOURCE KCM #Tenureship #HomeSelling #HomeBuying #SimardRealtyGroup  Congrats Jen! We found the perfect condo for you, your going to love it!

#UnderContract #Bristol #SimardRealtyGroup |

Archives

October 2022

Categories

All

|

RSS Feed

RSS Feed