There are many potential homebuyers, and even sellers, who believe that you need at least a 20% down payment in order to buy a home, or move on to their next home. Time after time, we have dispelled this myth by showing that there are many loan programs that allow you to put down as little as 3% (or 0% with a VA loan).

If you have saved up your down payment and are ready to start your home search, one other piece of the puzzle is to make sure that you have saved enough for your closing costs. Freddie Mac defines closing costs as: “Closing costs, also called settlement fees, will need to be paid when you obtain a mortgage. These are fees charged by people representing your purchase, including your lender, real estate agent, and other third parties involved in the transaction. Closing costs are typically between 2 and 5% of your purchase price.” We’ve recently heard from many first-time homebuyers that they wished that someone had let them know that closing costs could be so high. If you think about it, with a low down payment program, your closing costs could equal the amount that you saved for your down payment. Here is a list of just some of the fees/costs that may be included in your closing costs, depending on where the home you wish to purchase is located:

Is there any way to avoid paying closing costs? Work with your lender and real estate agent to see if there are any ways to decrease or defer your closing costs. There are no-closing mortgages available, but they end up costing you more in the end with a higher interest rate, or by wrapping the closing costs into the total cost of the mortgage (meaning you’ll end up paying interest on your closing costs). Home buyers can also negotiate with the seller over who pays these fees. Sometimes the seller will agree to assume the buyer’s closing fees in order to get the deal finalized. Bottom Line Speak with your lender and agent early and often to determine how much you’ll be responsible for at closing. Finding out you’ll need to come up with thousands of dollars right before closing is not a surprise anyone is ever looking forward to. Source KCM #ClosingCost #RealEstateAdvice #SimardRealtyGroup

0 Comments

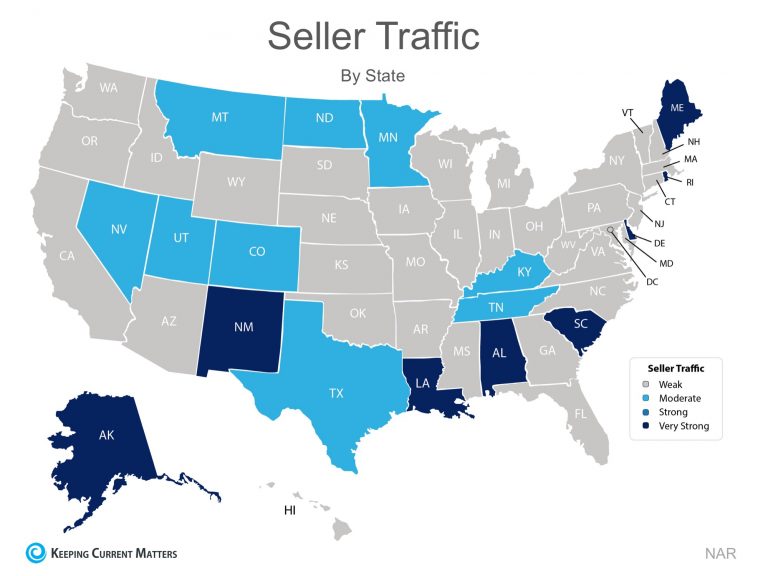

The price of any item is determined by the supply of that item, as well as the market demand. The National Association of REALTORS (NAR) surveys “over 50,000 real estate practitioners about their expectations for home sales, prices and market conditions” for their monthly REALTORS Confidence Index. Their latest edition sheds some light on the relationship between Seller Traffic (supply) and Buyer Traffic (demand). Buyer Demand The map below was created after asking the question: “How would your rate buyer traffic in your area?” The darker the blue, the stronger the demand for homes in that area. Only four states came in with a weak or moderate demand level. Seller Supply The Index also asked: “How would your rate seller traffic in your area?” As you can see from the map below, the majority of the country has weak Seller Traffic, meaning there are far fewer homes on the market than what is needed to satisfy the buyers who are out looking for their dream homes.  Bottom Line

Looking at the maps above, it is not hard to see why prices are appreciating in many areas of the country. Until the supply of homes for sale starts to meet the buyer demand, prices will continue to increase. If you are debating listing your home for sale, meet with a local real estate professional in your area who can help you capitalize on the demand in the market now! Source KCM #ForSellers #ForBuyers #HousingMarketUpdate #SimardRealtyGroup  In today’s market, with home prices rising and a lack of inventory, some homeowners may consider trying to sell their home on their own, known in the industry as a For Sale by Owner (FSBO). There are several reasons why this might not be a good idea for the vast majority of sellers.

Here are the top five reasons: 1. Exposure to Prospective Buyers Recent studies have shown that 88% of buyers search online for a home. That is in comparison to only 21% looking at print newspaper ads. Most real estate agents have an internet strategy to promote the sale of your home. Do you? 2. Results Come from the Internet Where did buyers find the home they actually purchased?

3. There Are Too Many People to Negotiate With Here is a list of some of the people with whom you must be prepared to negotiate if you decide to For Sale By Owner:

The paperwork involved in selling and buying a home has increased dramatically as industry disclosures and regulations have become mandatory. This is one of the reasons that the percentage of people FSBOing has dropped from 19% to 8% over the last 20+ years. The 8% share represents the lowest recorded figure since NAR began collecting data in 1981. 5. You Net More Money When Using an Agent Many homeowners believe that they will save the real estate commission by selling on their own. Realize that the main reason buyers look at FSBOs is because they also believe they can save the real estate agent’s commission. The seller and buyer can’t both save the commission. Studies have shown that the typical house sold by the homeowner sells for $210,000, while the typical house sold by an agent sells for $249,000. This doesn’t mean that an agent can get $39,000 more for your home, as studies have shown that people are more likely to FSBO in markets with lower price points. However, it does show that selling on your own might not make sense. Bottom LineBefore you decide to take on the challenges of selling your house on your own, sit with a real estate professional in your marketplace and see what they have to offer. SOURCE KCM #FSBOYayorNay #HireARealtor #SimardRealtyGroup |

Archives

October 2022

Categories

All

|

RSS Feed

RSS Feed