Congratulations! You’ve found a home to buy and have applied for a mortgage! You’re undoubtedly excited about the opportunity to decorate your new home, but before you make any large purchases, move your money around, or make any big-time life changes, consult your loan officer – someone who will be able to tell you how your decisions will impact your home loan.

Below is a list of Things You Shouldn’t Do After Applying for a Mortgage. Some may seem obvious, but some may not. 1. Don’t Change Jobs or the Way You Are Paid at Your Job. Your loan officer must be able to track the source and amount of your annual income. If possible, you’ll want to avoid changing from salary to commission or becoming self-employed during this time as well. 2. Don’t Deposit Cash into Your Bank Accounts. Lenders need to source your money, and cash is not really traceable. Before you deposit any amount of cash into your accounts, discuss the proper way to document your transactions with your loan officer. 3. Don’t Make Any Large Purchases Like a New Car or Furniture for Your New Home. New debt comes with it, including new monthly obligations. New obligations create new qualifications. People with new debt have higher debt to income ratios…higher ratios make for riskier loans…and sometimes qualified borrowers no longer qualify. 4. Don’t Co-Sign Other Loans for Anyone. When you co-sign, you are obligated. As we mentioned, with that obligation comes higher ratios as well. Even if you swear you will not be the one making the payments, your lender will have to count the payments against you. 5. Don’t Change Bank Accounts. Remember, lenders need to source and track assets. That task is significantly easier when there is consistency among your accounts. Before you even transfer any money, talk to your loan officer. 6. Don’t Apply for New Credit. It doesn’t matter whether it’s a new credit card or a new car. When you have your credit report run by organizations in multiple financial channels (mortgage, credit card, auto, etc.), your FICO® score will be affected. Lower credit scores can determine your interest rate and maybe even your eligibility for approval. 7. Don’t Close Any Credit Accounts. Many clients erroneously believe that having less available credit makes them less risky and more likely to be approved. Wrong. A major component of your score is your length and depth of credit history (as opposed to just your payment history) and your total usage of credit as a percentage of available credit. Closing accounts has a negative impact on both of those determinants in your score. Bottom Line Any blip in income, assets, or credit should be reviewed and executed in a way that ensures your home loan can still be approved. The best advice is to fully disclose and discuss your plans with your loan officer before you do anything financial in nature. They are there to guide you through the process. SOURCE KCM #FirstTimeHomeBuyer #ForSellers #SimardRealtyGroup #eXpRealty

0 Comments

Granby Open Farm Day offers a behind the scenes glimpse into life on the farms in Granby, Connecticut: See the fields where your food grows and the facilities where milk turns into cheese. Watch a horse-training clinic and a sheep shearing demonstration. Take a wagon ride, taste a new wine or the first apples of the season, try out spinning some wool, or take your photo on a tractor.  Follow these steps for the best Open Farm Day yet! Get a map + schedule brochure and pick a farm where you'd like to start. Print your passport at home or pick one up at your first stop. Be sure to get it stamped! Follow the signs from farm to farm. Catch tours, demos and tastings, all while collecting stamps in your passport at each stop. Turn in your passport at your final farm. Make sure you provide your name and contact info so we can reach you if you're a lucky prize winner this year!  Some Highlights:

SOURCE KCM #HousingMarket #ForSellers #ForBuyers #SimardRealtyGroup #eXpRealty  For Sale! 57 George St, Bristol CT priced @ $264,900.

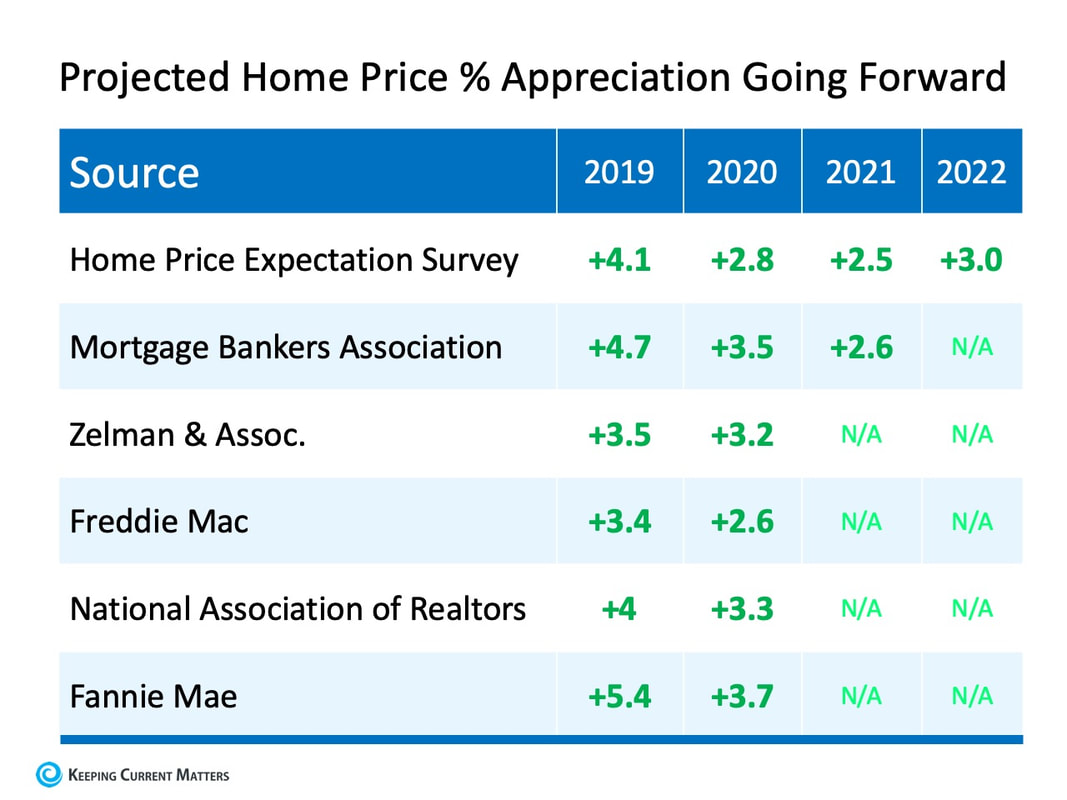

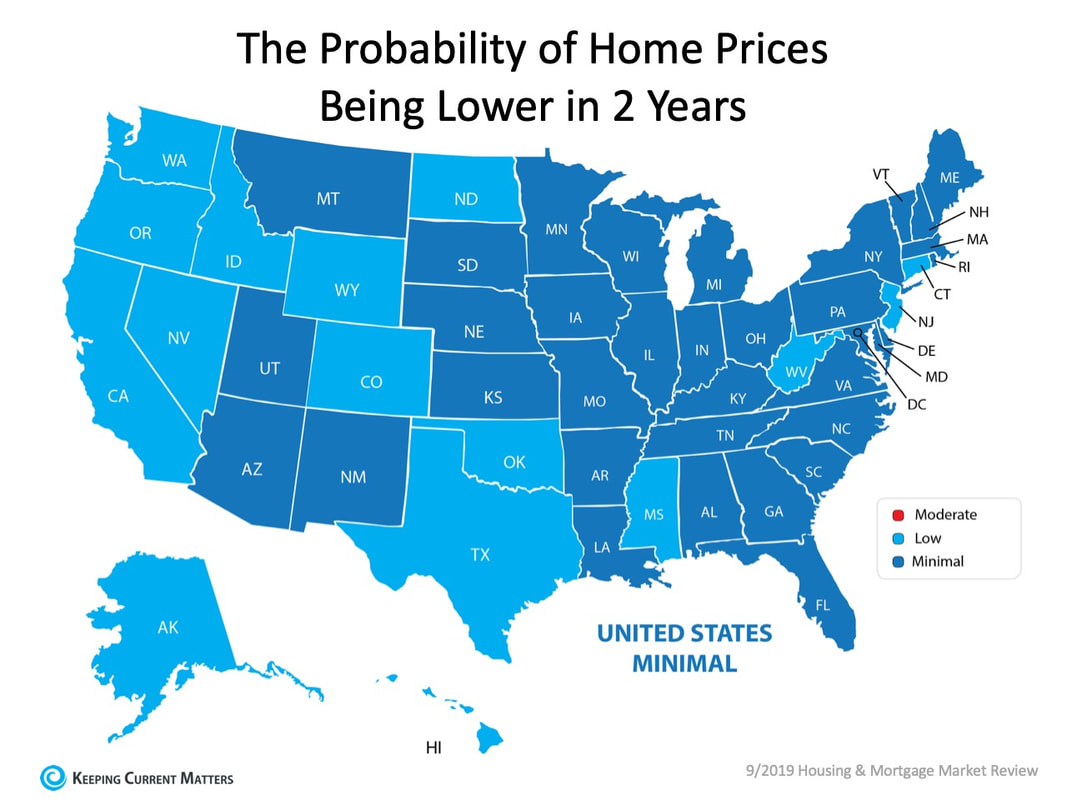

"Stately, well cared for five bedroom Colonial with over 3200 + sq ft. Character and charm resound throughout. So much home here, a must see. Featuring crown molding, built-ins, large rooms, hardwood floors,etailed Woodwork, and generous sized pantry. Walk in closets." See more photos and property info here: https://57georgest.thebestlisting.com/ #Bristol #SellingCT #SimardRealtyGroup #eXpRealty  With the current uncertainty about the economy triggered by a potential trade war, some people are waiting to purchase their first home or move-up to their dream house because they think or hope home prices will drop over the next few years. However, the experts disagree with this perspective. Here is a table showing the predicted levels of appreciation from six major housing sources:  As we can see, every source believes home prices will continue to appreciate (albeit at lower levels than we have seen over the last several years). But, not one source is calling for residential real estate values to depreciate. Additionally, ARCH Mortgage Insurance Company in their current Housing and Mortgage Market Review revealed their latest ARCH Risk Index, which estimates the probability of home prices being lower in two years. There was not one state that even had a moderate probability of home prices lowering. In fact, 34 of the 50 states had a minimal probability.  Bottom LineThose waiting for prices to fall before purchasing a home should realize that the probability of that happening anytime soon is very low. With mortgage rates already at near historic lows, now may be the time to act.

SOURCE KCM #BuyingMyths #HousingMarketUpdates #SimardRealtyGroup #joineXpRealty  Today we pray for the families and remember the victims of 9/11.

We will never forget.  In a recent article by Realtor Magazine, Mark Fleming, Chief Economist of First American Financial Corporation, notes,

“The largest group of millennials by birth year will turn 30 in 2020, which puts them entering their prime homebuying years”. The article continues to describe how millennials have more buying-power than the generations that preceded them, making their interest in embracing homeownership stronger than ever, “Millennials—the most educated generation—have the highest incomes across their generational cohorts, even when salaries are adjusted for inflation.” This combination of power and desire has the potential to drive positive growth in the homeownership rate heading into the near future. According to Fleming, ‘“The gap between the potential and actual homeownership in 2018 narrowed slightly as the growth in homeownership modestly exceeded the increase in potential demand,” he says, citing First American’s Homeownership Progress Index. “We expect the homeownership rate to further close the gap with potential in the years ahead as millennials continue to make important decisions, such as attaining an education and, later in life, getting married and having children.”’ That said, the shortage of sellable inventory in the entry and mid-range levels that’s attractive to potential millennial buyers may be a contributing factor as to why many millennials haven’t yet purchased a home. According to another recent report citing Frank Martell, President and CEO of CoreLogic, “Lower rates are certainly making it more affordable to buy homes and millennial buyers are entering the market with increasing force. These positive demand drivers, which are occurring against a backdrop of persistent shortages in housing stock, are the major drivers for higher home prices, which will likely continue to rise for the foreseeable future.” With millennials aging-up into mortgage-ready and home-buying territory, along with their strong buying interest and buying power, this generation is poised and ready to have positive impact on homeownership rates across the country. Many of them just need to find a home they’re excited to buy in this competitive end of the market. Bottom Line If you’re thinking of selling, reach out to a local real estate professional to determine if now is a great time for you to list your house and move-up. More millennials are getting ready to jump into the market and join the ranks of homeownership, so demand for homes in the starter and mid-level range will continue to be strong. SOURCE KCM #Homeownership #Millennials #MoveUpBuyers #SimardRealtyGroup #eXpRealty  For Sale! 11 Granby Farms Rd, Granby, CT @$417,399

"Fantastic opportunity to call this sought after Granby Farms Colonial home! Spacious sun filled rooms highlight the first floor living space of this meticulously cared for home. The kitchen boasts plenty of cabinet space, stainless steel appliances, island seating, a breakfast nook, & flows nicely into the formal living room. " View more photos and info here: https://11granbyfarmsrd.thebestlisting.com/ #ForSale #Granby #SimardRealtyGroup #eXpRealty  #5StarReview #HappyClient #SellingCT #SimardRealtyGroup #eXpRealty

So, you’ve decided to sell your house. You’ve hired a real estate professional to help you with the entire process and you’ve been asked what level of access you want to provide to potential buyers.

There are four elements to a quality listing. At the top of the list is Access, followed by Condition, Financing, and Price. There are many levels of access you can provide to your agent to be able to show your home. Here are five levels of access you can provide to a buyer, each with a brief description:

SOURCE KCM #ForBuyers #ForSellers #SimardRealtyGroup #joineXpRealty |

Archives

October 2022

Categories

All

|

RSS Feed

RSS Feed