If you thought about selling your house this year, now more than ever may be the time to do it! The inventory of homes for sale is well below historic norms and buyer demand is skyrocketing. We were still in high school when we learned about the concept of supply and demand, so we understand that the best time to sell something is when the supply of that item is low and demand for that item is high. That defines today’s real estate market.

Lawrence Yun, Chief Economist at the National Association of Realtors, recently commented: “Contract signings inched backward once again last month, as declines in the South and West weighed down on overall activity.” Yun goes on to say: “The reason sales are falling off last year’s pace is that multiple years of inadequate supply in markets with strong job growth have finally driven up home prices to a point where an increasing number of prospective buyers are unable to afford it.” In this type of market, a seller may hold a major negotiating advantage when it comes to price and other aspects of the real estate transaction, including the inspection, appraisal and financing contingencies. Bottom Line As a potential seller, you are in the driver’s seat right now. It might be time to hit the gas. SOURCE KCM #ForSellers #Buyers #SimardRealtyGroup #eXpRealty

0 Comments

Some Highlights:

SOURCE KCM #infographic #BuyingAHome #SimardRealtyGroup #eXpRealty  For the last several years, buyer demand has far exceeded the housing supply available for sale. This low supply and high demand have led to home prices appreciating by an average of 6.2% annually since 2012.

With this being said, three of the four major reports used to measure buyer activity have revealed that purchasing demand may be softening. Here are the four indices, how they measure demand (methodology), what their latest reports said, and a quick synopsis of the report. The Foot Traffic Report by the National Association of RealtorsMethodology: Every month SentriLock, LLC provides NAR Research with data on the number of properties shown by a REALTOR®. Lockboxes made by SentriLock, LLC are used in roughly a third of home showings across the nation. Foot traffic has a strong correlation with future contracts and home sales, so it can be viewed as a peek ahead at sales trends two to three months into the future. Latest Report: “Foot Traffic climbed 3.2 points to 55.8 mid-summer in July. Additionally, the diffusion index is higher than last year by 13.5 points. Despite a healthy economy and labor market, supply and new construction remains unable to keep up with buyer demand.” Synopsis: Buyer demand remains strong. The Showing Index by ShowingTimeMethodology: The ShowingTime Showing Index® tracks the average number of buyer showings on active residential properties on a monthly basis, a highly reliable leading indicator of current and future demand trends. Latest Report: “Showing activity throughout the country increased by 0.3 percent year over year in July, the third consecutive month that the U.S. ShowingTime Showing Index recorded buyer interest deceleration compared to the previous year. The June 2018 figures revealed a 0.0 percent change in showing traffic from 2017, while May showed a 1.2 percent year-over-year increase. The 12-month average year-over-year increase was 4.6 percent.” Synopsis: Buyer demand is softening Realtors Confidence Index by the National Association of RealtorsMethodology: The REALTORS Confidence Index is a key indicator of housing market strength based on a monthly survey sent to over 50,000 real estate practitioners. Practitioners are asked about their expectations for home sales, prices and market conditions. Latest Report: “REALTORS reported slower homebuying activity in July 2018…The REALTORS® Buyer Traffic Index registered at 62, down from the same month one year ago (69). This is the fifth straight month (since March 2018) that Realtors reported a decline in buyer activity compared to conditions one year ago.” Synopsis: Buyer demand is softening The Real Estate Broker Survey in the ‘Z’ Report by Zelman and Associates (subscription needed)Methodology: Proprietary survey results of real estate executives. Latest Report: “While we continue to expect a resumption of growth in resale transactions on the back of easing inventory in 2019 and 2020, our real-time view into the market through our Real Estate Broker Survey does suggest that buyers have grown more discerning of late and a level of “pause” has taken hold in many large housing markets. Indicative of this, our broker contacts rated buyer demand at 69 on a 0-100 scale, still above average but down from 74 last year and representing the largest year-over-year decline in the two-year history of our survey.” Synopsis: Buyer demand is softening Bottom Line Again, three of the four most reliable measures of buyer activity are reporting that demand is softening. We had a strong buyers’ market directly after the housing crash which was immediately followed by a strong sellers’ market over the last six years. If demand continues to soften and supply begins to grow (as is projected to happen), we will return to a more neutral market which will favor neither buyers nor sellers. This “more normal” market will be better for real estate in the long term. SOURCE KCM #ForBuyers #HousingMarketUpdates #SimardRealtyGroup #eXpRealty  Here are four great reasons to consider buying a home today instead of waiting.

1. Prices Will Continue to Rise CoreLogic’s latest Home Price Insights report reveals that home prices have appreciated by 6.2% over the last 12 months. The same report predicts that prices will continue to increase at a rate of 5.1% over the next year. Home values will continue to appreciate for years. Waiting no longer makes sense. 2. Mortgage Interest Rates Are Projected to Increase Freddie Mac’s Primary Mortgage Market Survey shows that interest rates for a 30-year mortgage have already increased by half of a percentage point, to around 4.5% in 2018. Most experts predict that rates will rise over the next 12 months. The Mortgage Bankers Association, Fannie Mae, Freddie Mac and the National Association of Realtors are in unison, projecting that rates will increase by half a percentage point to around 5.1% by this time next year. An increase in rates will impact your monthly mortgage payment. A year from now, your housing expense will increase if a mortgage is necessary to buy your next home. 3. Either Way, You Are Paying a Mortgage There are some renters who have not yet purchased homes because they are uncomfortable taking on the obligation of a mortgage. Everyone should realize that unless you are living with your parents rent-free, you are paying a mortgage – either yours or your landlord’s. As an owner, your mortgage payment is a form of ‘forced savings’ that allows you to build equity in your home which you can then tap into later in life. As a renter, you guarantee your landlord is the person building that equity. Are you ready to put your housing cost to work for you? 4. It’s Time to Move on with Your Life The ‘cost’ of a home is determined by two major components: the price of the home and the current mortgage rate. It appears that both are on the rise. But what if they weren’t? Would you wait? Look at the actual reason you are buying and decide if it is worth waiting. Whether you want to have a great place for your children to grow up, you want your family to be safer, or you just want to have control over renovations, maybe now is the time to buy. If the right thing for you and your family is to purchase a home this year, buying sooner rather than later could lead to substantial savings. SOURCE KCM #ForBuyers #BuyingAHome #SimardRealtyGroup #joineXpRealty  Home prices are at the top of everyone’s minds. Can they maintain their current pace of appreciation? Will rising mortgage rates negatively impact home values? Will the next economic slowdown cause prices to crash?

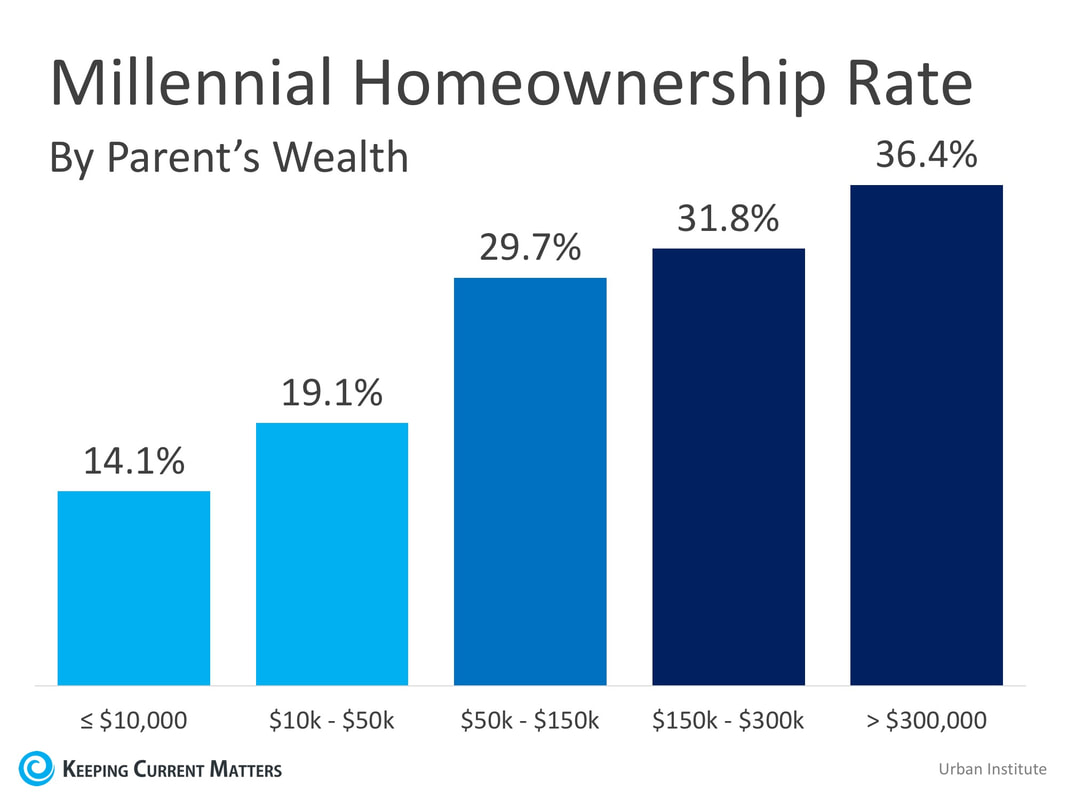

Let’s try to answer these questions based on what has happened in the past as well as what we know about the current real estate market. The Impact of Rising Interest Rates We explained earlier this year that rising mortgage rates have not negatively impacted home prices in the past and probably wouldn’t this time either. Freddie Mac’s comments were very direct: “In the current housing market, the driving force behind the increase in prices is a low supply of both new and existing homes combined with historically low rates. As mortgage rates increase, the demand for home purchases will likely remain strong relative to the constrained supply and continue to put upward pressure on home prices.” They were correct. So far this year, home values have continued to appreciate above normal historic percentages and it appears the gradual increase in rates has had little impact on prices. The Impact of an Economic Slowdown Many people fear that when the economy turns, we may see the same depreciation in home values as we did a decade ago. However, we recently reported that the same group of economists, real estate experts, and investment & market strategists who predicted the next recession will occur in the next 18-24 months have also projected that house prices will continue to appreciate for the next five years, albeit at smaller percentages. It Comes Down to Supply and Demand As always, home prices will be determined by the demand to purchase compared to the available inventory of homes for sale. For the last six years, demand has far exceeded the available supply which has resulted in the average annual appreciation to top 6% since 2012. That is far greater than the historic norm of 3.6% annual appreciation that we saw prior to the housing boom. There are currently small signs that housing inventory is slowly beginning to increase. Months supply of houses for sale matched last year’s numbers for the last two months after 37 consecutive months of decreasing inventory. New construction data has also shown positive signs that inventory will be increasing. As inventory begins to meet demand, we will see appreciation return to more normal levels. We are already seeing projections coming in lower than the 6.2% annual average we have seen more recently. CoreLogic is predicting that home values will appreciate by 5.1% over the next twelve months and the Home Price Expectation Survey calls for values to increase by 4.2% in 2019. Bottom Line Mark Fleming, Chief Economist at First American, explained it best: “We’re seeing the first indications that price appreciation may be slowing, but the underlying fundamental housing market conditions support a natural moderation of house prices rather than a sharp decline.” SOURCE KCM #ForBuyers #Pricing #SimardRealtyGroup #eXpRealty  There are many things that factor into the decision to buy a home. New research from the Urban Institutesuggests that one of those things may be inherited from your parents. Children are More Likely to Own a Home if Their Parents Did According to an analysis of millennial homeowners, the homeownership rate of those whose parents rent their homes is 14.4%, while the rate amongst millennials whose parents are homeowners is 31.7%! “A young adult’s odds of homeownership are highly correlated with their parent’s homeownership. Without controlling for such factors as age, income, education, marital status, and race or ethnicity, there is a 17 percentage-point gap between the homeownership rate for young adults whose parents are renters and young adults whose parents are homeowners.” The study also revealed that as a parent’s net worth increases, so does the likelihood that their child will own a home. These two findings are not surprising as we know from the Survey of Consumer Finances that a homeowner’s net worth is 44x greater than that of a renter. So, a parent who is a homeowner will have more wealth which will, in turn, increase the chances that their children will own their own homes in the future. Below is a breakdown of the relationship between a parent’s wealth and a millennial’s likelihood to own a home.  The Good News: The high homeownership rate amongst baby boomers (likely the parents of many millennials) is a great sign that millennials will want to own homes. We are already seeing this in the high-demand environment that we are currently experiencing in the starter and trade-up markets.

Bottom Line Even though millennials took longer than many of the generations before them to start home searches of their own, the data shows that they will not be waiting much longer! SOURCE KCM #ForBuyers #SimardRealtyGroup #joineXpRealty  There are many benefits to homeownership, but one of the top benefits is protecting yourself from rising rents by locking in your housing cost for the life of your mortgage.

Don’t Become Trapped A recent article by Apartment List addressed rising rents by stating: “Our national rent index is up 0.1 percent month-over-month, marking the sixth straight month of increasing rents. Year-over-year growth now stands at 1.2 percent.” The article continues, explaining that: “Rents increased month-over-month in 62 of the nation’s 100 largest cities, down significantly from the 85 cities that saw rents rise last month. That said, rents are still up year-over-year in most of the nation’s largest markets — 77 of the 100 largest cities have seen rents increase over the past twelve months.” Additionally, Urban Land Magazine explained that, “Currently, nearly half (47 percent) of renter households are cost burdened (i.e., paying more than 30 percent of income for housing), while 25 percent (totaling 11 million households) are severely cost burdened, paying over 50 percent of their total household income for rent.” These households struggle to save for a rainy day and pay other bills, including groceries and healthcare. It’s Cheaper to Buy Than Rent As we have previously mentioned, the results of the latest Rent vs. Buy Report from Trulia show that homeownership remains cheaper than renting with a traditional 30-year fixed rate mortgage in the 100 largest metro areas in the United States. The updated numbers show that the range is an average of 2% less expensive in Honolulu (HI), all the way up to 48.9% less expensive in Detroit (MI), and 26.3% nationwide! Know Your Options Perhaps you have already saved enough to buy your first home. A nationwide survey of about 1,166 renters found that 34% said they rent because they cannot afford to buy, 29% said they cannot afford to buy where they live, and nearly a quarter (24%) were saving to buy. Many first-time homebuyers who believe that they need a large down payment may be holding themselves back from their dream homes. As we have reported before, in many areas of the country, a first-time homebuyer can save for a 3% down payment in less than two years. You may have already saved enough! Bottom Line Don’t get caught in the trap that so many renters are currently in. If you are ready and willing to buy a home, find out if you are able. Have a professional help you determine if you are eligible for a mortgage today. SOURCE KCM #ForBuyers #SimardRealtyGroup #eXpRealty |

Archives

October 2022

Categories

All

|

RSS Feed

RSS Feed