Some Highlights:

SOURCE KCM #BuyingMyths #RentVSBuy #SimardRealtyGroup #joineXpRealty

0 Comments

The U.S. Census Bureau recently released their 2019 Q2 Homeownership Report. Some began to see the sky falling, believing the report showed Americans may be stepping back from their belief in homeownership. The national homeownership rate (Americans who owned vs. rented their primary residence) increased significantly during the housing boom, reaching its peak of 69.2% in 2004. The Census Bureau reported that the second quarter of 2019 ended with a homeownership rate of 64.1%, which is down from the 64.8% rate for the fourth quarter of 2018. Based on this news, some started to question the consumer’s belief in the idea of homeownership as a major part of the American Dream. Everyone Calm Down… It is true the homeownership rate did fall. However, if you look at the national rate over the last 35 years (1984-2019), you can see that the current homeownership rate has returned to historical norms. The 64.1% rate is equivalent to the rates in 1984 and 1994.  What Will the Future Bring?

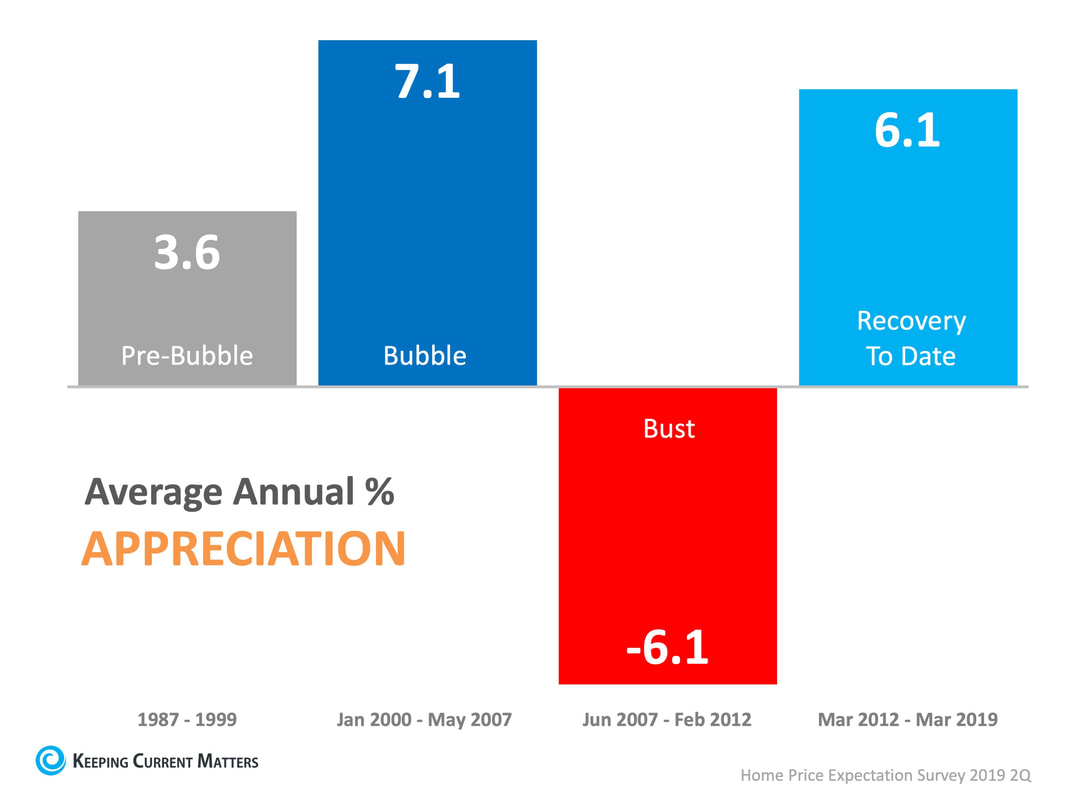

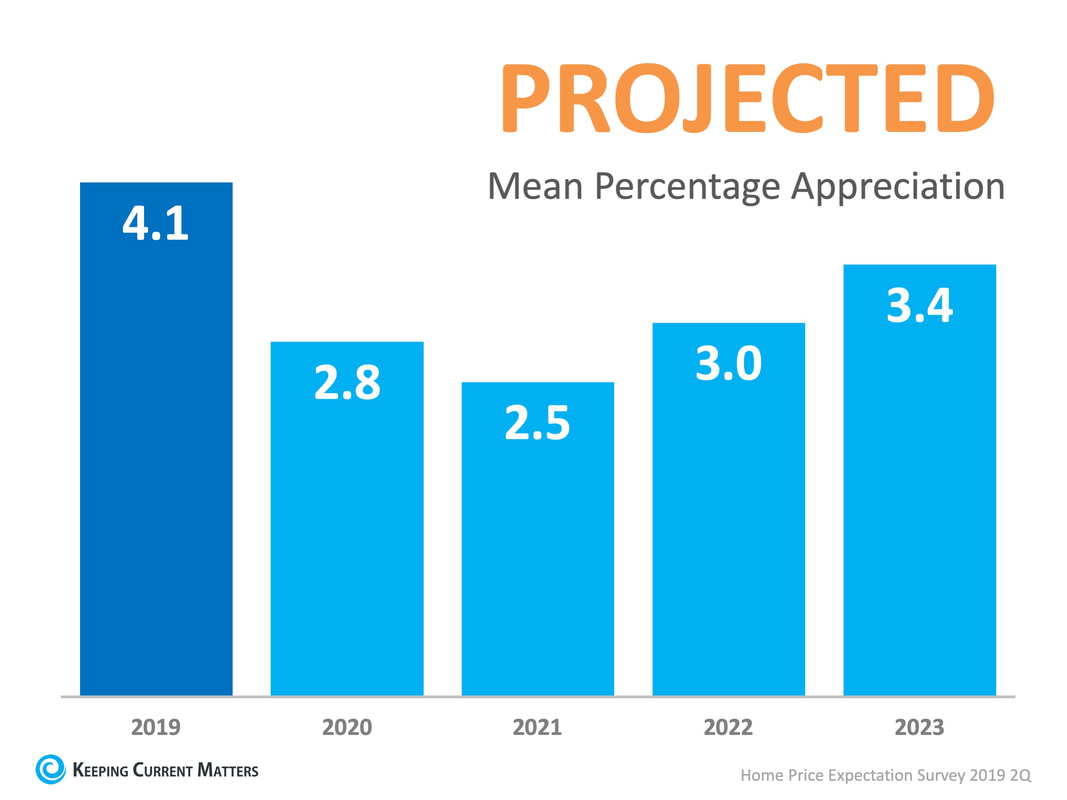

Part of the reason the homeownership rate slipped is a lack of inventory available for purchase for first-time home buyers. The demand is there, but currently, the supply is not. It seems, however, that is about to change. In a recent report, Ivy Zelman explained that builders have finally started to increase the number of homes they’re constructing at the lower-end price points: “Robust growth in the entry-level price point of late should translate to a reacceleration in homeownership rates moving forward.” Bottom Line Today, the homeownership rate sits at historic norms. In all probability, it will increase as more inventory becomes available. There is no reason for concern. SOURCE KCM #BuyingMyths #SellingMyths #BuyerandSelller #SimardRealtyGroup #eXpRealty  There’s no doubt that today’s housing market is changing, and everything we see right now indicates it is time to sell. Here’s a look at why selling now is likely to drive the greatest return on your largest investment. Home values have been appreciating for several years now, growing at a strong, steady, and impressive pace. In fact, the average annual appreciation rate since 2012 has nearly doubled the average rate from the more normal market of the 1990s (think: pre-bubble).  Appreciation, however, is projected to shift back toward normal, meaning home prices will likely keep climbing over the next few years, but they are not projected to continue to increase at such a high rate. Here’s What That Means for Homeowners: As noted in the latest Home Price Expectation Survey (HPES) powered by Pulsenomics, experts forecast an average annual appreciation rate closer to 3.2% over the next five years, which is more in line with a historically normal market (3.6%). The good news is, there’s still time to take advantage of the current strength of home prices by selling your house now.  Looking at the projections as they stand today, 2019 is slated to drive the strongest appreciation as compared to the upcoming few years. With average home prices still on the rise, the pace at which they are predicted to continue increasing will likely soften by 2020.

Bottom Line If you’re thinking about selling your house, now is a great time to make your move. Don’t get stuck waiting until projected home price appreciation rates potentially re-accelerate again in 2023. You’ll likely earn the greatest return on your investment by selling now before the prices start to normalize next year. SOURCE KCM #HousingMarketUpdates #SellingMyths #SimardRealtyGroup #eXpRealty

Many people assume their credit score is too low to qualify to purchase a home. In reality, 84% of Americans have a credit score that would allow them to become homeowners.! If you'd like to find out more about what your credit score really means, let's get together to chat about the opportunities.

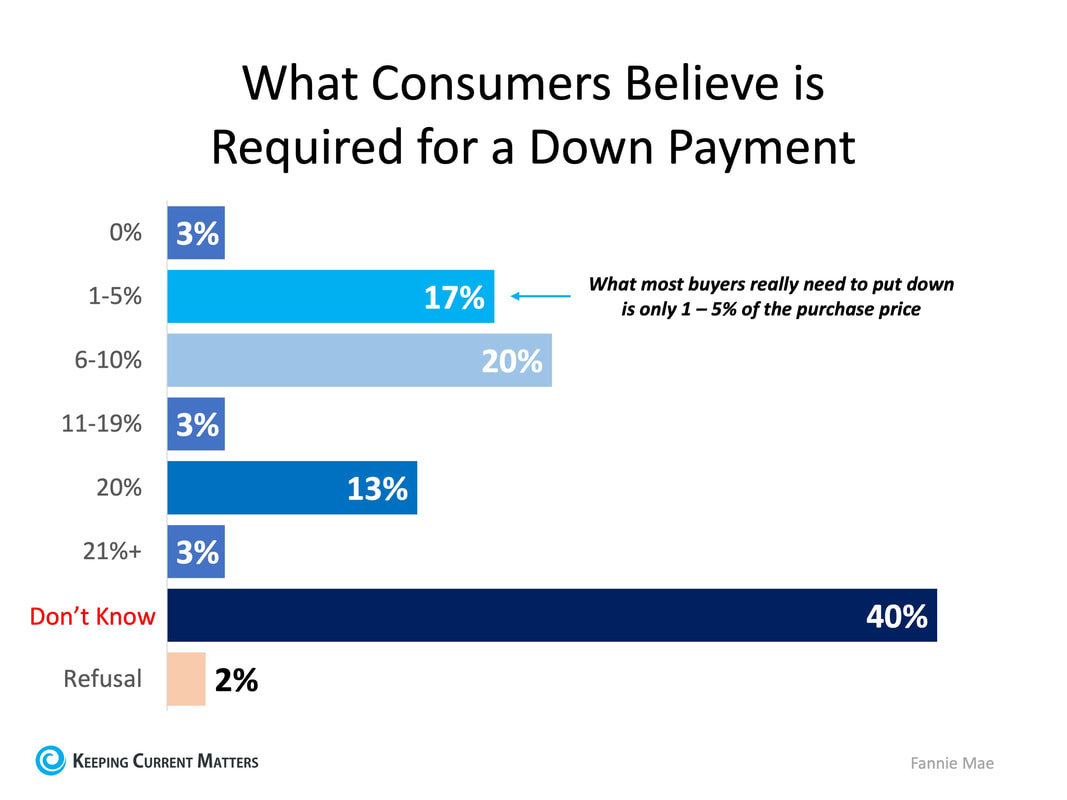

Contact your Simsbury Top Realtor today at 860-919-0991 for more info. #GranbyHomes #Homesforsale #Realestate #Simsburyhomes #HomeValues #RealEstateAdvise #RealtorGranby #RealEstateSimsbury #StephenSimard #eXpRealty  Whether you’ve owned a home before, or you’re ready to jump into homeownership for the first time, there are always a lot of questions swirling around about what is truly required for a down payment, and how to best source down payment assistance. Let’s tackle these two today. 1. How much do you really need for a down payment? There is a long-standing misconception about down payment requirements. A survey from Fannie Maeshows only 17% of consumers know the minimum options are actually between 1 – 5% of the purchase price and 40% don’t know how much they need at all.  There are many mortgage loans available that require as little as 3% down for first-time buyers, and some ask for only 3.5% down from repeat buyers. There are even loans available for Veterans that provide 0% down payment options too.

We’ve mentioned recently that you don’t need to come up with a 20% down payment to buy, and we’ve also shared how quickly you can save for a 3% or 10% down payment, depending on where you live. If you’re planning to put down just 3%, the research shows it may be possible in most states to have enough saved for a down payment in less than a year. That puts homeownership in a much closer reach for many potential buyers, maybe even you! 2. How can I get help with my down payment? Regardless of the loans available, many buyers still need assistance with a down payment. The great news is, there are a lot of ways to tap into down payment assistance options. Here are just a couple of them: Assistance from Family Members The National Association of Realtors (NAR) said, “a third of recent first-time buyers received down payment assistance from family members.” They also mentioned, “the average net worth of those aged 75 and over stands at $264,800…They just might offer the boost the next generation needs to become homeowners.” That means one of the ways to find help with a down payment is to accept a gift from a family member. If this is an option for you, make sure you talk to your loan officer before you accept the money, to ensure you document the process the way it is required by your loan. This way, it will be received properly and you can still potentially qualify. Down Payment Assistance Programs The reality is, not everyone has a loved one or a family member who can provide help with a down payment. There are, however, more than 2,500 down payment assistance programs available (by local areas like city, county, or neighborhood), and some of them are even specifically for first-time buyers. The gap, as mentioned in the same survey, is “only 23% of consumers are familiar with low down payment programs.” That’s why it is so important to get familiar with these options by doing your homework before you plan to buy a home. Determine what is available in the area where you ultimately want to live, so you have all the details you need to take advantage of the down payment assistance option that is best for your family. Bottom Line If buying a home is one of your long-term goals, you may be able to get there sooner than you think by tapping into one of the many down payment assistance programs available. SOURCE KCM #BuyingMyths #DownPayments #SimardRealtyGroup #joineXpRealty  On his personal website, self-made millionaire David Bach makes a striking statement:

“Not prioritizing homeownership is the single biggest mistake millennials are making.” He further stated, “Buying a home is an escalator to wealth.” Bach explains: “Young adults in particular aren’t hopping on this escalator, and it’s a costly mistake…If millennials don’t buy a home, their chances of actually having any wealth in this country are little to none.” He then elaborates on the game of homeownership: “Start by crunching the numbers…actually do the math…This way, you’re really clear on your goals and you won’t just say to yourself, ‘I’ll never afford this!’ A good rule of thumb is to make sure your total monthly housing payment doesn’t consume more than 30 percent of your take-home pay.” Bach concludes by saying, “Oftentimes, buying your first home means you’re not buying your dream home…You’re just getting into the market.” Bottom Line Whenever a well-respected millionaire gives investment advice, listeners usually clamor to hear it. This millionaire shares some simple and straightforward insights: “The fact is, you aren’t really in the game of building wealth until you own some real estate.” SOURCE KCM #BuyingMyths #Millenials #RentVSBuy #SimardRealtyGroup #joineXpRealty  Just Listed!

15 Harrison St, Bristol CT @ $245k "Take a look at this great multi unit home perfect for owner occupant. Live on one floor and have most of the mortgage paid by the tenant! This two family home is conveniently located in the Federal Hill area very close to Bristol hospital. " Read more property info here: https://15harrisonst.worldsbestlisting.com/ #JustListed #ForSale #SellingCT #SimardRealtyGroup #eXpRealty  We’ve experienced economic growth for almost a decade, which is the longest recovery in the nation’s history. Experts know a recession can’t be too far off, but when will this economic slowdown actually occur?

Pulsenomics just released a special report revealing that nearly 6 out of 10 of the 90 economists, investment strategists, and market analysts surveyed believe the next recession will occur by the end of next year. Here’s the breakdown:

When asked what would trigger the next recession, the three most common responses by those surveyed were:

How might the recession impact real estate? Challenges in the housing and mortgage markets were major triggers of the last recession. However, a housing slowdown ranked #9 on the list of potential triggers for the next recession, behind such possibilities as fiscal policy and political gridlock. As far as the impact the recession may have on home values, the experts surveyed indicated home prices would continue to appreciate over the next few years. They called for a 4.1% appreciation rate this year, 2.8% in 2020, and 2.5% in 2021. Bottom Line On the same day, in the same survey, the same experts who forecasted a recession happening within the next 18 months also claimed housing will not be the trigger, and home values will still continue to appreciate. SOURCE KCM #BuyingMyths #SellingMyths #SimardRealtyGroup #eXpRealty |

Archives

October 2022

Categories

All

|

RSS Feed

RSS Feed