Some experts are calling for a slowdown in the economy later this year and most economists have predicted that the next recession could only be eighteen months away. The question is, what impact will a recession have on the housing market?

Here are the opinions of several experts on the subject: Ivy Zelman in her latest “Z Report”: “While economic activity appears to have accelerated so far in 2018, some prominent economic forecasters have become more cautious about growth prospects for 2019 and 2020… All told, while solid long-term demographic underpinnings support our positive fundamental outlook for housing, in the event micro-economic headwinds surface, we would expect housing transaction volumes and home prices to weather the storm.” Aaron Terrazas, Zillow’s Senior Economist: “While much remains unknown about the precise path of the U.S. economy in the years ahead, another housing market crisis is unlikely to be a central protagonist in the next nationwide downturn.” Mark Fleming, First American’s Chief Economist: “If a recession is to occur, it is unlikely to be caused by housing-related activity, and therefore the housing sector should be one of the leading sources to come out of the recession.” Mark J. Hulbert, Financial Analyst and Journalist: “Real estate may be one of your best investments during the next bear market for stocks. And by real estate, I mean your home or other residential properties.” U.S. News and World Report: “Fortunately – and hopefully – the history of recessions and current issues that could harm the economy don’t lead many to believe the housing market crash will repeat itself in an upcoming decline.” SOURCE KCM #ForBuyers #ForSellers #SimardRealtyGroup #eXpRealty

0 Comments

Care free living at The Hamlet! This 2BR Townhouse sits in one of the best spots in the complex. Backed up to open space and overlooking an expansive back yard area with a private deck. New price at $125k!

View photos and info here: https://4thehamlet.thebestlisting.com/ #PriceReduced #Enfield #SimardRealtyGroup #eXpRealty

Whether you’re buying or selling, it can be quite the adventure, which is why you need an experienced real estate professional to guide you on the path to achieving your goal.

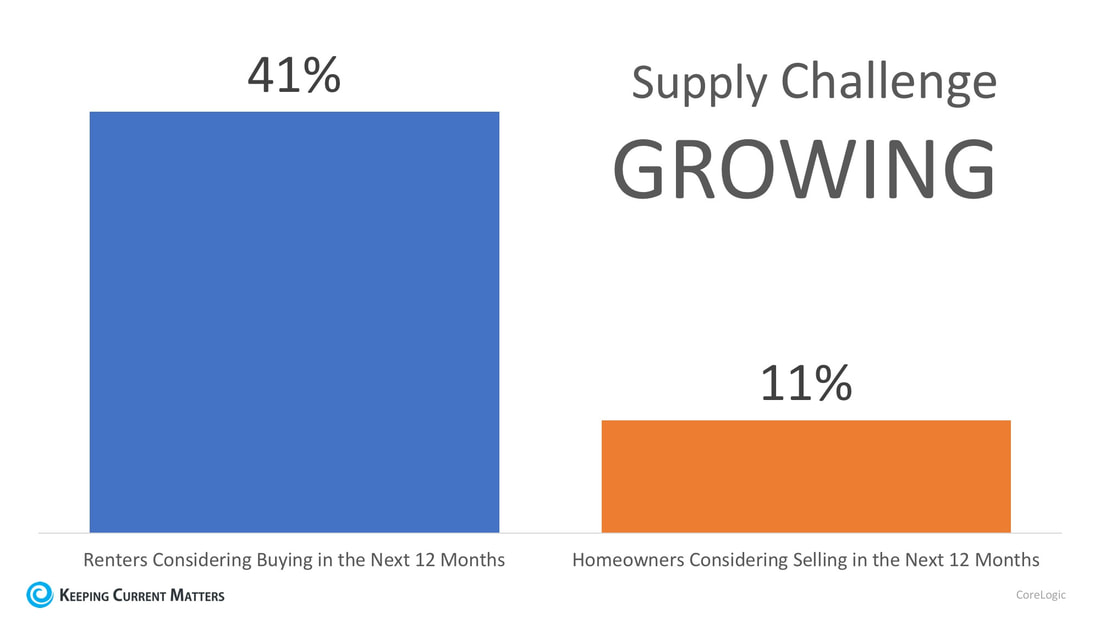

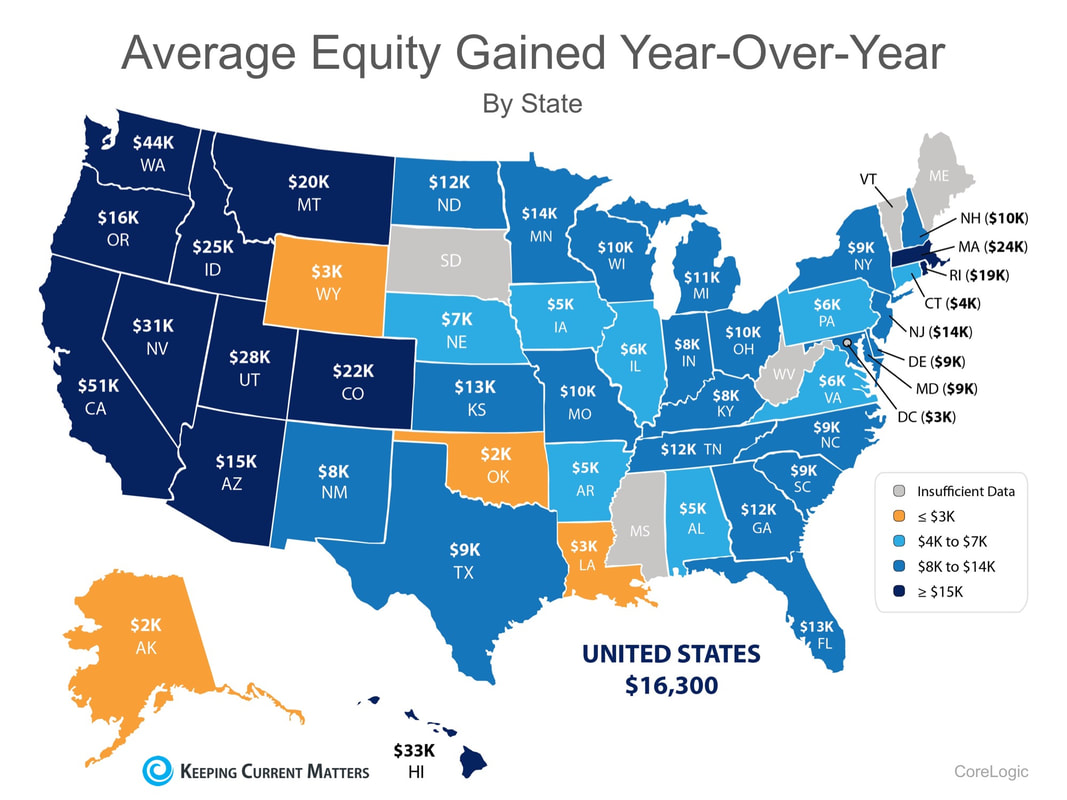

#HireApro #RealEstateProfessional #SimardRealtyGroup #eXpRealty  Across the United States, there is a severe mismatch between the low number of houses for sale and the high demand for those houses! First-time homebuyers are out in force and are being met with a highly competitive summer real estate market. According to the National Association of Realtors (NAR), the inventory of homes for sale “has fallen year-over-year for 36 consecutive months,” and now stands at a 4.1-month supply. A 6-month supply of inventory is necessary for a balanced market and has not been seen since August of 2012. NAR’s Chief Economist Lawrence Yun had this to say, “Inventory coming onto the market during this year’s spring buying season – as evidenced again by last month’s weak reading – was not even close to being enough to satisfy demand. That is why home prices keep outpacing incomes and listings are going under contract in less than a month – and much faster – in many parts of the country.” Is There Any Relief Coming? According to the CoreLogic’s 2018 Consumer Housing Sentiment Study, four times as many renters are considering buying homes in the next 12 months than homeowners who are planning to sell, “which is the crux of the available housing-supply imbalance.”  As more and more renters realize the benefits of homeownership, the demand for housing will continue to rise. Do homeowners realize demand is so high? With home prices rising across the country, homeowners gained over a trillion dollars in equity over the last 12 months, with the average homeowner gaining over $16,000! The map below shows the breakdown by state:  Many homeowners who have not thought about listing their homes may not even realize how much equity they have gained, or the opportunity available to them in today’s market!

Bottom Line If you are one of the many homeowners across the country who hasn’t quite found their forever home, now may be a great time to list your house for sale and find your dream home! #ForBuyers #ForSellers #SimardRealtyGroup #eXpRealty  We often talk about why it makes financial sense to buy a home, but more often than not, the emotional reasons are the more powerful or compelling ones.

No matter what shape or size your living space is, the concept and feeling of home can mean different things to different people. Whether it’s a certain scent or a favorite chair, the emotional reasons why we choose to buy our own homes are typically more important to us than the financial ones. 1. Owning your home offers you the stability to start and raise a family Between the best neighborhoods and the best school districts, even buyers without children at the time of purchase may have these things in mind as major reasons for choosing the locations of the homes that they purchase. 2. There’s no place like home Owning your own home offers you not only safety and security, but also a comfortable place that allows you to relax after a long day! 3. You have more space for you and your family Whether your family is expanding, an older family member is moving in, or you need to have a large backyard for your pets, you can take this all into consideration when buying your dream home! 4. You have control over renovations, updates, and style Looking to actually try one of those complicated wall treatments that you saw on Pinterest? Tired of paying an additional pet deposit in your apartment building? Or maybe you want to finally adopt that puppy or kitten you’ve seen online 100 times? Who’s to say that you can’t do just that in your own home? Bottom Line Whether you are a first-time homebuyer or a move-up buyer who wants to start a new chapter in your life, now is a great time to reflect on the intangible factors that make a house a home. #Buyers #OwningAHome #RentVSBuy #SimardRealtyGroup #eXpRealty  According to the Realtors Confidence Index from the National Association of Realtors, 61% of first-time homebuyers purchased their homes with down payments below 6% in 2017.

Many potential homebuyers believe that a 20% down payment is necessary to buy a home and have disqualified themselves without even trying, but in March, 71% of first-time buyers and 54% of all buyers put less than 20% down. Ralph McLaughlin, Chief Economist and Founder of Veritas Urbis Economics, recently shed light on why buyer demand has remained strong, “The fact that we now have four consecutive quarters where owner households increased while renters households fell is a strong sign households are making the switch from renting to buying. Households under 35 – which represent the largest potential pool of new homeowners in the U.S. – have shown some of the largest gains. While they only make up a third of all homebuyers, the steady uptick in their homeownership rate over the past year suggests their enormous purchasing power may be finally coming to [the] housing market.” It’s no surprise that with rents rising, more and more first-time buyers are taking advantage of low-down-payment mortgage options to secure their monthly housing costs and finally attain their dream homes. Bottom Line If you are one of the many first-time buyers unsure of whether or not they would qualify for a low-down payment mortgage, consult a local real estate professional who can set you on your path to homeownership! #BuyingMyths #DownPayments #SimardRealtyGroup #eXpRealty

The American Dream of homeownership is alive and well. Before you sign another lease, let’s get together to help you better understand all your options.

#HomeOwnership #SimardRealtyGroup #eXpRealty  Since the beginning of the year, mortgage interest rates have risen over a half of a percentage point (from 3.95% to 4.52%), according to Freddie Mac. Even a small rise in interest rates can greatly impact a buyer’s monthly mortgage payment.

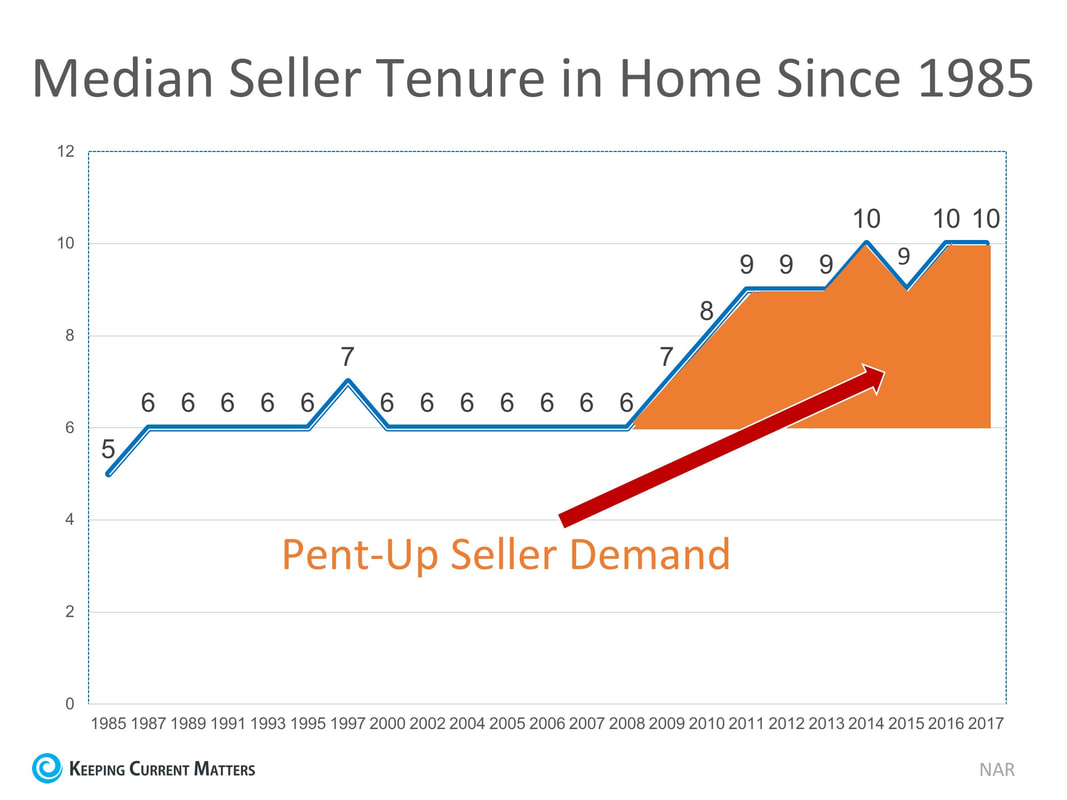

First American recently released the results of their quarterly Real Estate Sentiment Index (RESI), in which they surveyed title and real estate agents across the country about the impact of rising rates on first-time homebuyers. Real estate professionals around the country have not noticed a slowdown in demand for housing among young buyers; nearly 93% of all first-time homebuyers last quarter were between the ages of 21-35, with the largest share of buyers (51%) coming from those ages 26-30. First American’s Chief Economist Mark Fleming had this to say, “On a national level, mortgage rates would need to hit 5.6%, 1 percentage point above the current rate, before first-time homebuyers withdraw from the market.” So, what is slowing down sales? According to the last Existing Home Sales Report from the National Association of Realtors, sales are now down 3.0% year-over-year and have fallen for the last three months. If rising interest rates aren’t to blame, then what is? Fleming addressed the cause, saying that: “The housing market is facing its greatest supply shortage in 60 years of record keeping, according to the Federal Reserve Bank of Kansas City. The ongoing housing supply shortage will make it difficult for first-time buyers to find a home to buy, even when they are financially ready.” Bottom Line First-time homebuyers know the importance of owning their own homes and a spike in interest rates is not going to keep them from buying this year! Their biggest challenge is finding a home to buy! SOURCE KCM #FirstTimeHomeBuyers #Millennials #SimardRealtyGroup #eXpRealty  The National Association of Realtors (NAR) keeps historical data on many aspects of homeownership. One of their data points, which has changed dramatically, is the median tenure of a family in a home, meaning how long a family stays in a home prior to moving. As the graph below shows, over the last twenty years (1985-2008), the median tenure averaged exactly six years. However, since 2014, that average is almost ten years – an increase of almost 50%.  Why the dramatic increase?The reasons for this change are plentiful!

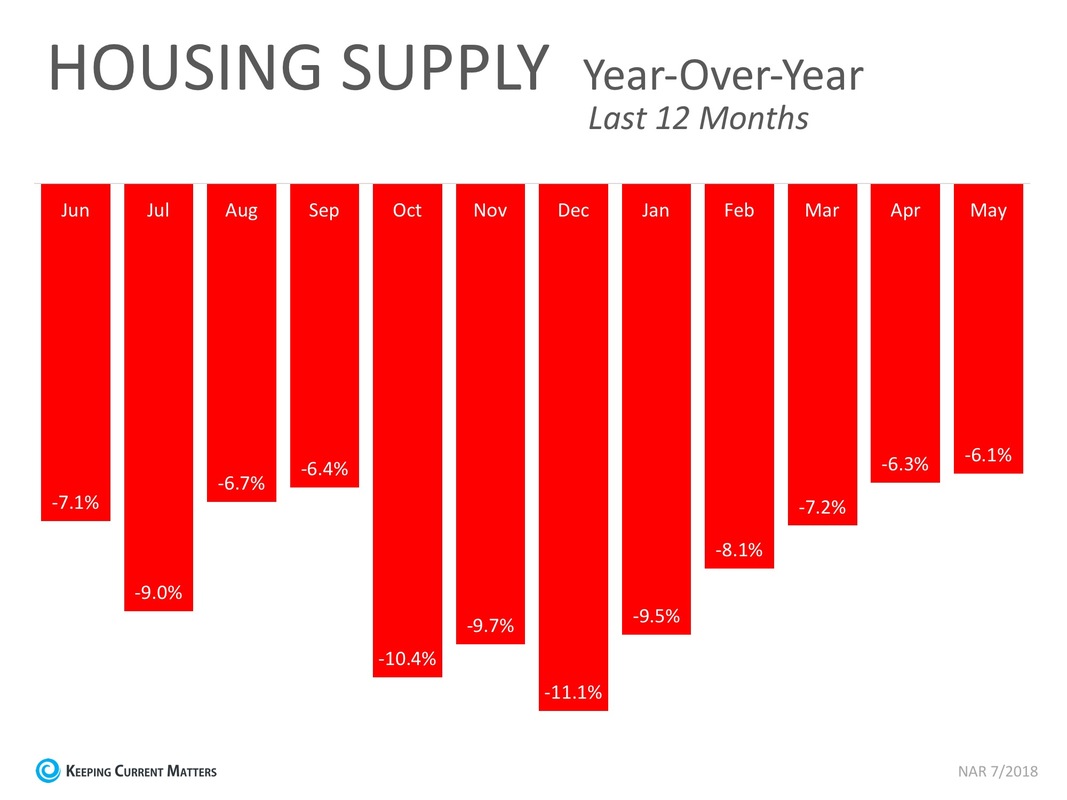

The fall in home prices during the housing crisis left many homeowners in a negative equity situation (where their home was worth less than the mortgage on the property). Also, the uncertainty of the economy made some homeowners much more fiscally conservative about making a move. With home prices rising dramatically over the last several years, 95.3% of homes with a mortgage are now in a positive equity situation, according to CoreLogic. With the economy coming back and wages starting to increase, many homeowners are in a much better financial situation than they were just a few short years ago. One other reason for the increase was brought to light by NAR in their 2018 Home Buyer and Seller Generational Trends Report. According to the report, “Sellers 37 years and younger stayed in their home for six years…” These homeowners, who are either looking for more space to accommodate their growing families or for better school districts to do the same, are likely to move more often (compared to typical sellers who stayed in their homes for 10 years). The homeownership rate among young families, however, has still not caught up to previous generations, resulting in the jump we have seen in median tenure! What does this mean for housing? Many believe that a large portion of homeowners are not in a house that is best for their current family circumstance; they could be baby boomers living in an empty, four-bedroom colonial, or a millennial couple living in a one-bedroom condo planning to start a family. These homeowners are ready to make a move, and since a lack of housing inventory is still a major challenge in the current housing market, this could be great news. SOURCE KCM #Sellers #HousingMarketUpdate #SimardRealtyGroup #eXpRealty  If you are debating whether or not to list your house for sale this year, here is the #1 reason not to wait! Buyer Demand Continues to Outpace the Supply of Homes for SaleThe National Association of Realtors’ (NAR) Chief Economist Lawrence Yun recently commented on the current lack of inventory: “Inventory coming onto the market during this year’s spring buying season – as evidenced again by last month’s weak reading – was not even close to being enough to satisfy demand. That is why home prices keep outpacing incomes and listings are going under contract in less than a month – and much faster – in many parts of the country.” The latest Existing Home Sales Report shows that there is currently a 4.1-month supply of homes for sale. This remains lower than the 6-month supply necessary for a normal market, and 6.1% lower than last year’s inventory level. The chart below details the year-over-year inventory shortages experienced over the last 12 months:  Anything less than a six-month supply is considered a “seller’s market.”

Bottom Line Meet with a local real estate professional who can show you the supply conditions in your neighborhood and assist you in gaining access to the buyers who are ready, willing, and able to buy right now! SOURCE KCM #ForSellers #HousingMarket #SimardRealtyGroup #eXpRealty |

Archives

October 2022

Categories

All

|

RSS Feed

RSS Feed