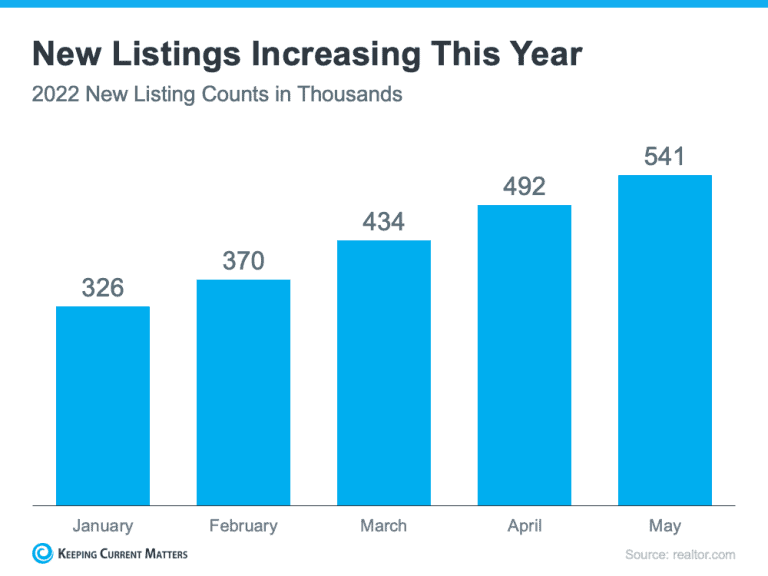

Are you thinking about selling your current home? If so, the biggest question on your mind may be: if I sell now, where will I go? If this resonates with you, there’s something you should know. The number of homes coming onto the market is increasing and that could make it easier for you to move up this summer. According to the latest data from realtor.com, the number of homes being listed for sale, known as new listings, has increased consistently this year (see graph below):  While this news has clear benefits for buyers who are craving more options for their home search, what does that mean for current homeowners like you? It gives you two distinct opportunities in today’s housing market.

Opportunity #1: Take Advantage of More Options for Your Move Up If your current house no longer meets your needs or lacks the space and features you want, this gives you even more opportunity to sell and move up into the home of your dreams. As more options come to market, you’ll have more to choose from when you search for your next home. Partnering with a local real estate professional can help make sure you see these listings as soon as they come onto the market. And when you do find the one, that professional can advise you on how to write a winning offer to seal the deal. Opportunity #2: Sell Before You Have More Competition Just know that, in order to make sure your house shines above the rest, it may make sense to put your home up for sale before your neighbors do the same, creating more competition in your area. The increase in the number of homes being listed for sale is expected to continue, and a recent study from realtor.com says two-thirds of homeowners looking to sell say they’ll do so by August. A real estate professional can advise you on what you need to tackle to get your house ready to list so they can put that for sale sign up in your yard sooner rather than later. That’s because the process of getting a home ready to sell isn’t taking as long as you may think. As a result, you can capitalize on today’s sellers’ market and get ahead of the competition. Bottom Line If you’re a current homeowner looking to sell, reach out to a local real estate professional to begin the process. You have a unique opportunity to benefit from the additional homes being listed today and sell before your house has more competition. Source: KCM #ForBuyers#ForSellers#HousingMarketUpdates#MoveUpBuyers#StephenSimardRealtor #RealBrokerLLC

0 Comments

June is #PrideMonth, and as we celebrate, let’s help make sure everyone can proudly pursue the dream of homeownership by strengthening our communities through diversity and inclusion.

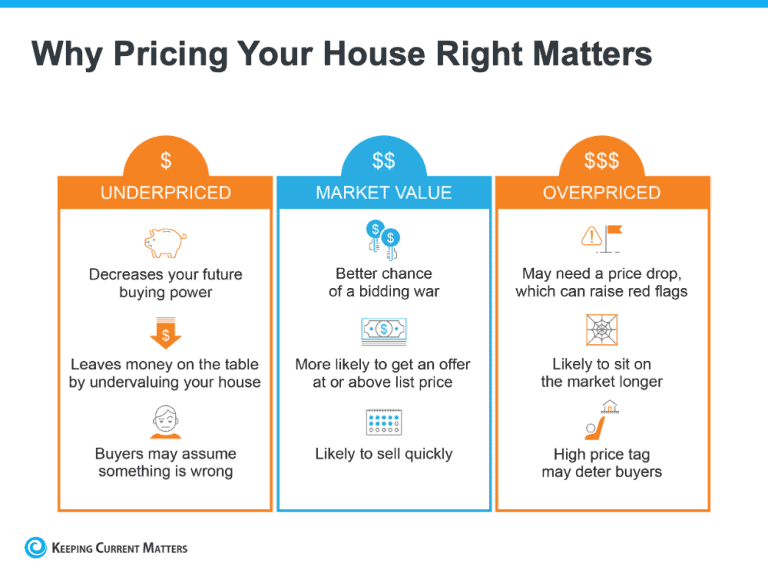

Source: KCM #homeownership #Pride #homeownershipmonth #diversity #community #realestate #homebuying #realestategoals #realestatetips #realestatelife #realestatenews #realestateagent #realestatetipsandadvice #keepingcurrentmatters #StephenSimardRealtor #RealBrokerLLC  If your lifestyle has changed recently and you’re ready to make a move, taking advantage of today’s sellers’ market might be just the answer for your summer plans. With homes continuing to get multiple offers, this could be your moment to get the contract you’re looking for on your house if you’re ready to sell. And here’s the thing – you need an expert on your side to ensure you make all the right moves when you do, especially when it comes to pricing your house. Even in this competitive market, you can’t stick just any price tag on your home and get the deal you want. A key piece of the puzzle is setting the right asking price so you can help buyers notice your home (and get excited about it) from the very first time they view the listing. That’s where a real estate professional comes in. Why Pricing Your House Right Is Important The price you set for your house sends a message to potential buyers. Price it too low and you might raise questions about your home’s condition or lead buyers to assume something is wrong with the property. Not to mention, if you undervalue your house, you could leave money on the table which decreases your future buying power. On the other hand, price it too high, and you run the risk of deterring buyers. When that happens, you may have to do a price drop to try to re-ignite interest in your house when it sits on the market for a while. But be aware that a price drop can be seen as a red flag for some buyers who will wonder why the price was reduced and what that means about the home. In other words, think of pricing your home as a target. Your goal is to aim directly for the center – not too high, not too low, but right at market value. Pricing your house fairly based on market conditions increases the chance you’ll have more buyers who are interested in purchasing it. That makes it more likely you’ll see multiple offers, too. And if a bidding war happens, you’ll likely get an even higher final sale price. Plus, when homes are priced right, they tend to sell quickly. To get a look into the potential downsides of over or underpricing your house and the perks that come with pricing it at market value, see the chart below:  Lean on a Professional’s Expertise

There are several factors that go into pricing your house, and balancing them is the key. That’s why it’s important to lean on an expert real estate advisor when you’re ready to move. A local real estate advisor is knowledgeable about:

A real estate professional will balance these factors to make sure the price of your house makes the best first impression and gives you the greatest return on your investment in the end. Bottom Line If you’re thinking about selling, pricing your house appropriately is key. Work with a trusted real estate advisor to make sure your house is priced right for the local market, your home’s condition, and to stand out from the competition. Source: KCM #ForSellers#Pricing#SellingMyths#StephenSimardRealtor #RealBrokerLLC  Some Highlights

Source: KCM #ForBuyers#ForSellers#HousingMarketUpdates#Infographics#Pricing#StephenSimardRealtor #RealBrokerLLC  June is National Homeownership Month, and it’s the perfect time to reflect on how impactful owning a home can truly be. When you purchase a house, it becomes more than just a space you occupy. It’s your stake in the community, an investment, and a place you can put your stamp on.

If you’re thinking about buying a home this year, here are some of the benefits you’ll experience when you do. The Emotional Benefits of Homeownership Because it’s a place that’s uniquely yours, owning a home can give you a sense of pride and happiness in several ways. Your Home Can Reflect Your Tastes and Personality Investopedia puts it like this: “One often-cited benefit of homeownership is the knowledge that you own your little corner of the world.” That knowledge can lead to a powerful, emotional connection to the place where you live. But so can the realization that your home will grow with you. Because it’s yours, you have the freedom to make updates to it as your needs and tastes change. As Logan Mohtashami, Lead Analyst for HousingWire, says: “The psychology is that this is yours and you’re going to make it as good as possible because you’re in for a long time, . . . “ And that can create a greater sense of ownership, pride, and connection with your home and your community. It Can Enhance Your Neighborhood and Civic Engagement Homeownership can lead you to get even more involved with your local area. After all, you’re putting your roots down in a location and will want to do what you can to help improve it, much like your home. In a recent report, the National Association of Realtors (NAR) says: “Living in one place for a longer amount of time creates and [sic] obvious sense of community pride, which may lead to more investment in said community.” The Financial Benefits of Homeownership When you choose to become a homeowner, you’re making a financial decision as well. That’s because your home is also an investment. It Can Help You Feel Financially Stable Homeownership is truly one of the best ways to improve your long-term financial position. Not only will you have a predictable monthly housing expense that can benefit your budget in the short term, but you’ll also gain equity as your home appreciates in value and you make your monthly mortgage payment. As Freddie Mac says: “Building equity through your monthly principal payments and appreciation is a critical part of homeownership that can help you create financial stability.” It Can Grow Your Wealth Because of your growing equity, you can build your net worth as a homeowner. And when you compare the difference in net worth between a renter and a homeowner, it’s clear that owning a home truly offers a great way to build your long-term financial position. According to the latest data from NAR, the median household net worth of a homeowner is roughly $300,000, while the median net worth of renters is only about $8,000. That means a homeowner’s net worth is nearly 40 times that of a renter. Bottom Line Homeownership is truly a way to find greater satisfaction and happiness and to build financial freedom. If National Homeownership Month has you dreaming about purchasing a home, contact a local real estate professional to begin the process today Source: KCM #FirstTimeHomeBuyers#ForBuyers#MoveUpBuyers#StephenSimardRealtor #RealBrokerLLC

Source: KCM

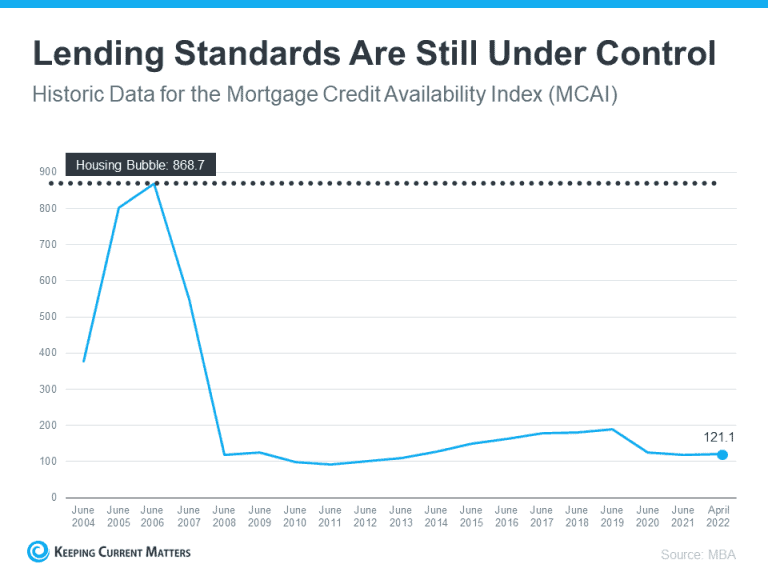

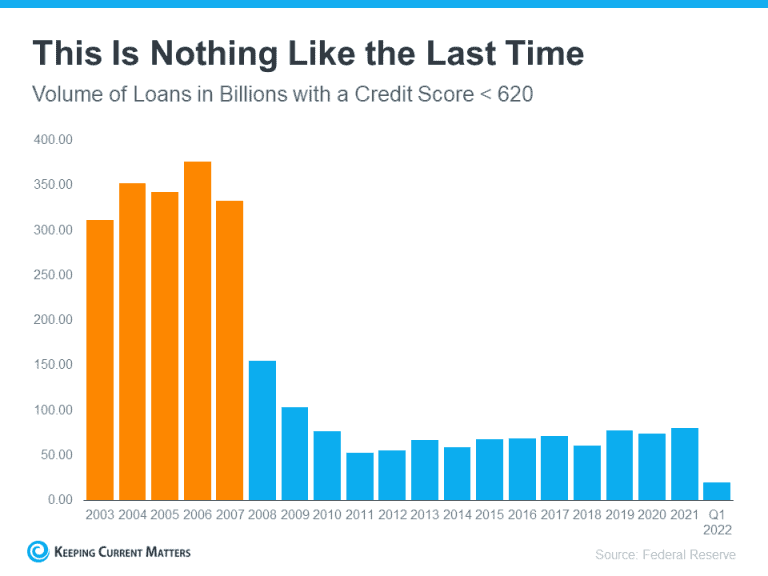

#GranbyRealtor#StephenSimardRealtor #RealBrokerLLC #ThinkingofMovingUpThisSummer  In today’s housing market, many are beginning to wonder if we’re returning to the riskier lending habits and borrowing options that led to the housing crash 15 years ago. Let’s ease those concerns. Several times a year, the Mortgage Bankers Association (MBA) releases an index titled the Mortgage Credit Availability Index (MCAI). According to their website: “The MCAI provides the only standardized quantitative index that is solely focused on mortgage credit. The MCAI is . . . a summary measure which indicates the availability of mortgage credit at a point in time.” Basically, the index determines how easy it is to get a mortgage. The higher the index, the more available mortgage credit becomes. Here’s a graph of the MCAI dating back to 2004, when the data first became available:  As the graph shows, the index stood at about 400 in 2004. Mortgage credit became more available as the housing market heated up, and then the index passed 850 in 2006. When the real estate market crashed, so did the MCAI as mortgage money became almost impossible to secure. Thankfully, lending standards have eased somewhat since then, but the index is still low. In April, the index was at 121, which is about one-seventh of what it was in 2006. Why Did the Index Get out of Control During the Housing Bubble? The main reason was the availability of loans with extremely weak lending standards. To keep up with demand in 2006, many mortgage lenders offered loans that put little emphasis on the eligibility of the borrower. Lenders were approving loans without always going through a verification process to confirm if the borrower would likely be able to repay the loan. An example of the relaxed lending standards leading up to the housing crash is the FICO® credit score associated with a loan. What’s a FICO® score? The website myFICO explains: “A credit score tells lenders about your creditworthiness (how likely you are to pay back a loan based on your credit history). It is calculated using the information in your credit reports. FICO® Scores are the standard for credit scores—used by 90% of top lenders.” During the housing boom, many mortgages were written for borrowers with a FICO score under 620. While there are still some loan programs that allow for a 620 score, today’s lending standards are much tighter. Lending institutions overall are much more attentive about measuring risk when approving loans. According to the latest Household Debt and Credit Report from the New York Federal Reserve, the median credit score on all mortgage loans originated in the first quarter of 2022 was 776. The graph below shows the billions of dollars in mortgage money given annually to borrowers with a credit score under 620.  In 2006, buyers with a score under 620 received $376 billion dollars in loans. In 2021, that number was only $80 billion, and it’s only $20 billion in the first quarter of 2022.

Bottom Line In 2006, lending standards were much more relaxed with little evaluation done to measure a borrower’s potential to repay their loan. Today, standards are tighter, and the risk is reduced for both lenders and borrowers. These are two very different housing markets, and today is nothing like the last time. Source: KCM #ForBuyers#ForSellers#HousingMarketUpdates#StephenSimardRealtor #RealBrokerLLC |

Archives

October 2022

Categories

All

|

RSS Feed

RSS Feed