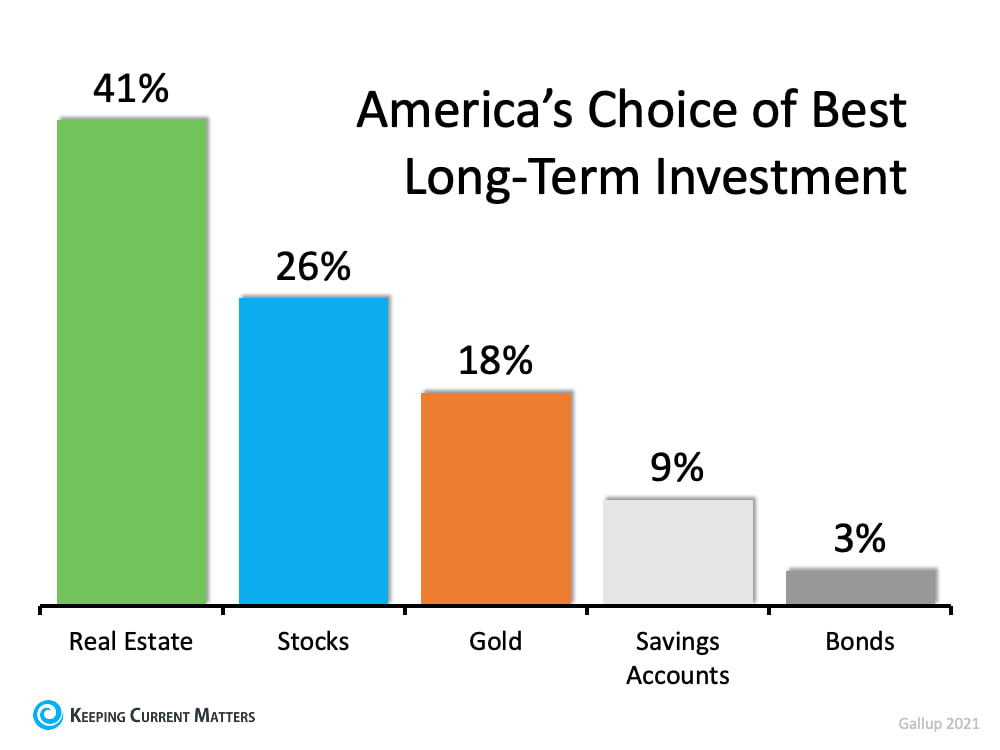

Last month, in a post on the Liberty Street Economics blog, the Federal Reserve Bank of New York noted that Americans believe buying a home is definitely or probably a better investment than buying stocks. Last week, a Gallup Poll reaffirmed those findings. In an article on the current real estate market, Gallup reports: “Gallup usually finds that Americans regard real estate as the best long-term investment among several options — seeing it as superior to stocks, gold, savings accounts and bonds. This year, 41% choose real estate as the best investment, up from 35% a year ago, with stocks a distant second.” Here’s the breakdown:  The article goes on to say:

“The 41% choosing real estate is the highest selecting any of the five investment options in the 11 years Gallup has asked this question.” Is real estate really a secure investment right now? Some question American confidence in real estate as a good long-term investment right now. They fear that the build-up in home values may be mirroring what happened right before the housing crash a little more than a decade ago. However, according to Merrill Lynch, J.P. Morgan, Morgan Stanley, and Goldman Sachs, the current real estate market is strong and sustainable. As Morgan Stanley explains to their clients in a recent Thoughts on the Market podcast: “Unlike 15 years ago, the euphoria in today’s home prices comes down to the simple logic of supply and demand. And we at Morgan Stanley conclude that this time the sector is on a sustainably, sturdy foundation . . . . This robust demand and highly challenged supply, along with tight mortgage lending standards, may continue to bode well for home prices. Higher interest rates and post pandemic moves could likely slow the pace of appreciation, but the upward trajectory remains very much on course.” Bottom Line America’s belief in the long-term investment value of homeownership has been, is, and will always be, very strong. SOURCE KCM #ForBuyersandSellers #Pricing #SimardRealtyGroup #RealBrokerLLC

0 Comments

It's a great time to make the dream of homeownership a reality. Let's connect if your heart is set on homeownership this year.

#TopGranbyRealtor #StephenSimard #RealBrokerLLC #GranbyRealEstate #GranbyConnecticut #FindyourGranbyhome #Newhomesforsale #SimardRealtyGroup #Granbyhomesforsale #JoinRealBrokerLLC #Simsburyhomes  When buying a home, it’s important to have a budget and make sure you plan ahead for certain homebuying expenses. Saving for a down payment is the main cost that comes to mind for many, but budgeting for the closing costs required to get a mortgage is just as important.

What Are Closing Costs? According to Trulia: “When you close on a home, a number of fees are due. They typically range from 2% to 5% of the total cost of the home, and can include title insurance, origination fees, underwriting fees, document preparation fees, and more.” For example, for someone buying a $300,000 home, they could potentially have between $6,000 and $15,000 in closing fees. If you’re in the market for a home above this price range, your closing costs could be greater. As mentioned above, closing costs are typically between 2% and 5% of your purchase price. Trulia gives more great advice, explaining: “There will be lots of paperwork in front of you on closing day, and not enough time to read them all. Work closely with your real estate agent, lender, and attorney, if you have one, to get all the documents you need ahead of time. The most important thing to read is the closing disclosure, which shows your loan terms, final closing costs, and any outstanding fees. You’ll get this form about three days before closing since, once you (the borrower) sign it, there’s a three-day waiting period before you can sign the mortgage loan docs. If you have any questions about the numbers or what any of the mortgage terms mean, this is the time to ask—your real estate agent is a great resource for getting you all the answers you need.” Bottom Line As home prices are rising and more buyers are finding themselves competing in bidding wars, it’s more important than ever to make sure your plan includes budgeting for closing costs. Work with your lender and a local real estate professional to be sure you have everything you need to land your dream home. SOURCE KCM #BuyingMyths #Pricing #FirstTimeHomeBuyers #SimardRealtyGroup #RealBrokerLLC  Some Highlights

SOURCE KCM #FSBO #SellingMyths #ForSellers #SimardRealtyGroup #RealBrokerLLC

Today's housing market makes it easy to win as a seller. Let's connect if you're ready to make a move this year.

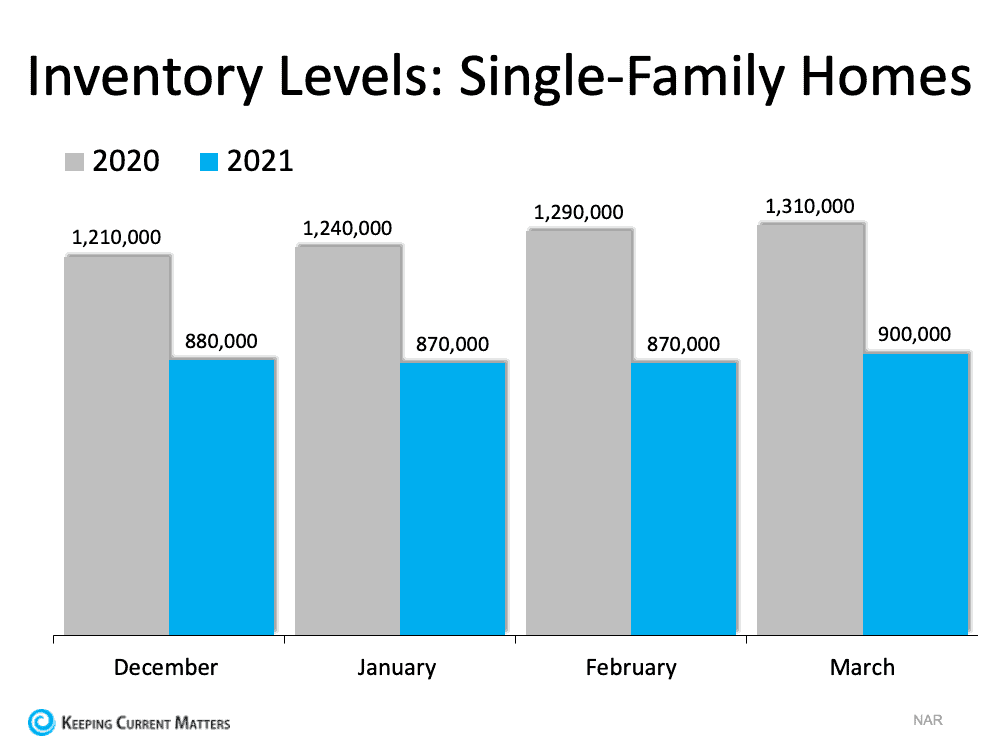

#TopGranbyRealtor #StephenSimard #RealBrokerLLC #GranbyRealEstate #GranbyConnecticut #FindyourGranbyhome #Newhomesforsale #SimardRealtyGroup #Granbyhomesforsale #JoinRealBrokerLLC #Simsburyhomes  Homebuyers are flooding the housing market right now to take advantage of record-low mortgage rates. Many have a sense of urgency to find a home soon since experts forecast a steady rise in both rates and home prices this year and next. As a result, buyer demand greatly outweighs the current housing supply. Here’s how the shortage of houses for sale sets yours up to be the oasis in an inventory desert. According to the National Association of Realtors (NAR), today’s housing inventory sits at an incredibly low 2.1-month supply, far below the 6-month mark for a neutral market. Inventory of single-family homes a year ago was already very low, and as you can see in the graph below, this year’s levels are even lower:  Due to these market conditions, today’s buyers frequently enter fierce bidding wars while trying to purchase a home. This in turn drives up home prices and gives sellers incredible leverage in the negotiation process, two big wins if you’re going to sell your house this year.

Bottom Line In such a hot market, it can feel as though the supply of homes has virtually dried up, leaving buyers to wander in an inventory desert. That’s why there’s never been a better time to sell. To a parched buyer needing to secure a home as soon as possible, your house could be a true oasis. SOURC KCM #ForSellers #MoveUpBuyers #HousingMarketUpdates #SimardRealtyGroup #RealBrokrLLC  Over the past year, the pandemic made it challenging for some homeowners to make their mortgage payments. Thankfully, the government initiated a forbearance program to provide much-needed support. Unless they’re extended once again, some of these plans and the corresponding mortgage payment deferral options will expire soon. That said, there’s still time to request assistance. If your loan is backed by HUD/FHA, USDA, or VA, you can apply for initial forbearance by June 30, 2021.

Recently, the Consumer Finance Institute of the Federal Reserve Bank of Philadelphia surveyed a national sample of 1,172 homeowners with mortgages. They discussed their familiarity with and understanding of lender accommodations that might be available under the Coronavirus Aid, Relief, and Economic Security (CARES) Act. The results indicate that some borrowers didn’t take advantage of the support available through forbearance: “Most borrowers who had not used forbearance during the pandemic reported that it was because they simply did not need it. However, among the remainder, a lack of understanding about available accommodations may also be playing a role. Around 2 out of 3 in this group reported not seeking forbearance because they were unsure or pessimistic about whether they would qualify — even though a high fraction of borrowers are eligible for forbearance under the Coronavirus Aid, Relief, and Economic Security (CARES) Act.” Here are some of the reasons why those borrowers didn’t opt for forbearance:

If you’re concerned forbearance may be costly:The Consumer Financial Protection Bureau (CFPB) explains: “For most loans, there will be no additional fees, penalties, or additional interest (beyond scheduled amounts) added to your account, and you do not need to submit additional documentation to qualify. You can simply tell your servicer that you have a pandemic-related financial hardship.” It’s important to contact your mortgage provider (the company you send your mortgage payment to every month) to explain your current situation and determine the best plan available for your needs. If you’re not sure how to request forbearance:Here are 5 steps to follow when requesting mortgage forbearance:

If you don’t understand how the plans work and/or whether you will qualify:This is how the Consumer Financial Protection Bureau (CFPB) explains the program: “Forbearance is when your mortgage servicer or lender allows you to pause or reduce your mortgage payments for a limited time while you build back your finances… Forbearance doesn’t mean your payments are forgiven or erased. You are still obligated to repay any missed payments, which, in most cases, may be repaid over time or when you refinance or sell your home. Before the end of the forbearance, your servicer will contact you about how to repay the missed payments.” The CFPB also addresses who qualifies for forbearance relief: “You may have a right to a COVID hardship forbearance if:

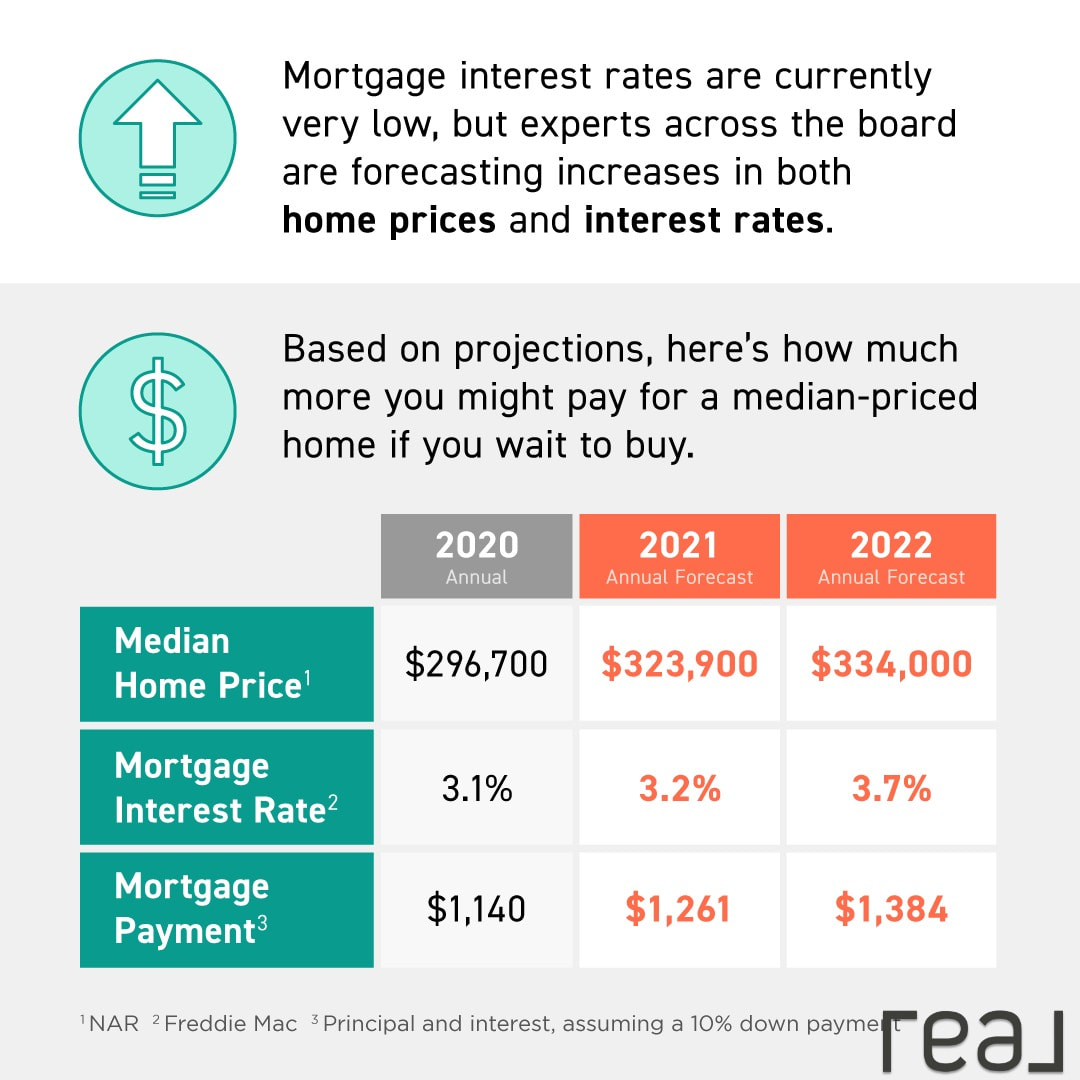

Bottom Line Like many Americans, your home may be your biggest asset. By acting quickly, you might be able to take advantage of critical relief options to help keep you in your home. Even if you tried to apply at the beginning of the pandemic and for some reason it didn’t work out, try again. Contact your mortgage provider today to determine if you qualify. If you have additional concerns, let’s connect to answer your questions and determine if there are other mortgage relief options in our area as well. SOURCE KCM #DistressedProperties #Foreclosures #HousingMarketUpdates #SimardRealtyGroup #RealBrokerLLC   If you’re thinking that waiting a year or two to purchase a home might mean you’ll save some money, think again. Experts project both home prices and mortgage rates will continue to rise, which means this is the best time to secure a more affordable home. DM me if you have questions about the best way to achieve your homebuying goals.

#buyingahome #affordability #firsttimehomebuyer #opportunity #housingmarket #househunting #makememove #homegoals #houseshopping #housegoals #locationlocationlocation #newlisting #homeforsale #curbappeal #keepingcurrentmatters  It’s clear that consumers are concerned about how quickly home values are rising. Many people fear the speed of appreciation may lead to a crash in prices later this year. In fact, Google reports that the search for “When is the housing market going to crash?” has actually spiked 2450% over the past month.

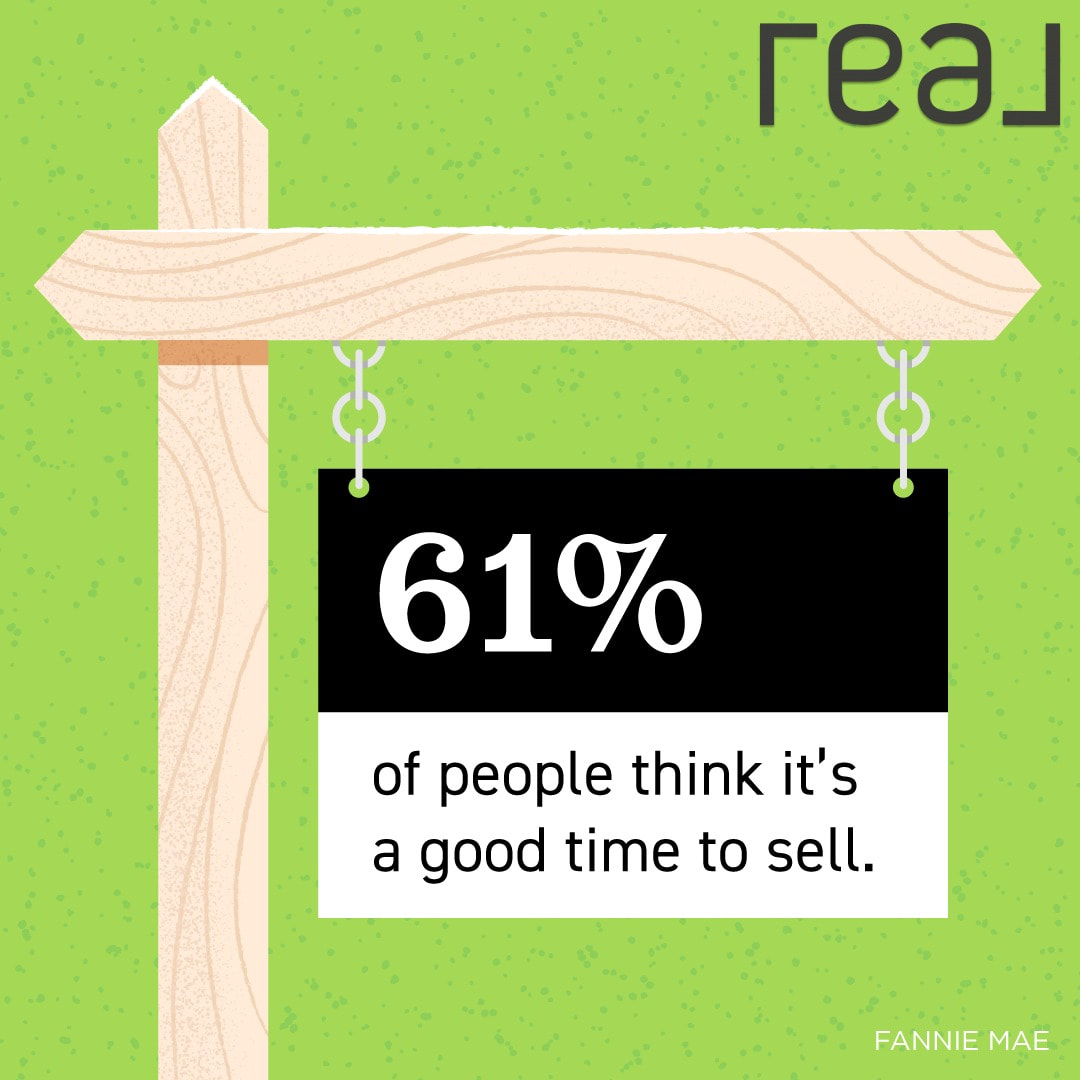

In addition, Jim Dalrymple II of Inman News notes: “One of the most noteworthy things that came up in Inman’s conversations with agents was that every single one said they’ve had conversations with clients about whether or not the market is heading into a bubble.” To alleviate some of these concerns, let’s look at what several financial analysts are saying about the current residential real estate market. Within the last thirty days, four of the major financial services giants came to the same conclusion: the housing market is strong, and price appreciation will continue. Here are their statements on the issue: Goldman Sachs’ Research Note on Housing: “Strong demand for housing looks sustainable. Even before the pandemic, demographic tailwinds and historically-low mortgage rates had pushed demand to high levels. … consumer surveys indicate that household buying intentions are now the highest in 20 years. … As a result, the model projects double-digit price gains both this year and next.” Joe Seydl, Senior Markets Economist, J.P.Morgan: “Homebuyers—interest rates are still historically low, though they are inching up. Housing prices have spiked during the last six-to-nine months, but we don’t expect them to fall soon, and we believe they are more likely to keep rising. If you are looking to purchase a new home, conditions now may be better than 12 months hence.” Morgan Stanley, Thoughts on the Market Podcast: “Unlike 15 years ago, the euphoria in today’s home prices comes down to the simple logic of supply and demand. And we at Morgan Stanley conclude that this time the sector is on a sustainably, sturdy foundation . . . . This robust demand and highly challenged supply, along with tight mortgage lending standards, may continue to bode well for home prices. Higher interest rates and post pandemic moves could likely slow the pace of appreciation, but the upward trajectory remains very much on course.” Merrill Lynch’s Capital Market Outlook: “There are reasons to believe that this is likely to be an unusually long and strong housing expansion. Demand is very strong because the biggest demographic cohort in history is moving through the household-formation and peak home-buying stages of its life cycle. Coronavirus-related preference changes have also sharply boosted home buying demand. At the same time, supply is unusually tight, with available homes for sale at record-low levels. Double-digit price gains are rationing the supply.” Bottom Line If you’re concerned about making the decision to buy or sell right now, contact your trusted real estate professional to discuss what’s happening in your local market. SOURCE KCM #ForBuyers #ForSellers #Pricing #SimardRealtyGroup #RealBrokerLLC  61% of people think it’s a good time to sell – and they’re right. Virtually every factor in today’s housing market benefits homeowners ready to make a move thanks to high buyer demand and low housing supply. DM me so you can get started in the selling process today.

#goodtimetosell #realestate #realestategoals #realestatetips #realestateagent #realestateexpert #realestateagency #realestatemarket #realestateexperts #realestateagents #instarealestate #instarealtor #realestatetipsoftheday #realestatetipsandadvice #keepingcurrentmatters |

Archives

October 2022

Categories

All

|

RSS Feed

RSS Feed