UNDER CONTRACT! 29 Byron Drive, Granby, CT

Congrats to our client! "Come home to this charming Colonial set in desired Poet's Corner. You will appreciate a few of the recent upgrades such as a newer roof 2018, new furnace, new easy care vinyl siding 2018. Inside find a generous sized kitchen with ample cabinet space, stainless refrigerator, and eat in area. Additional features included hardwood floors, a wood burning fireplace in the formal living room, built in shelving, and a family room. " Read more of this gorgeous property here: https://29byrondrive.isthebest.house/ #UnderContract #SellingCT #Granby #SimardRealtyGroup #eXpRealty

0 Comments

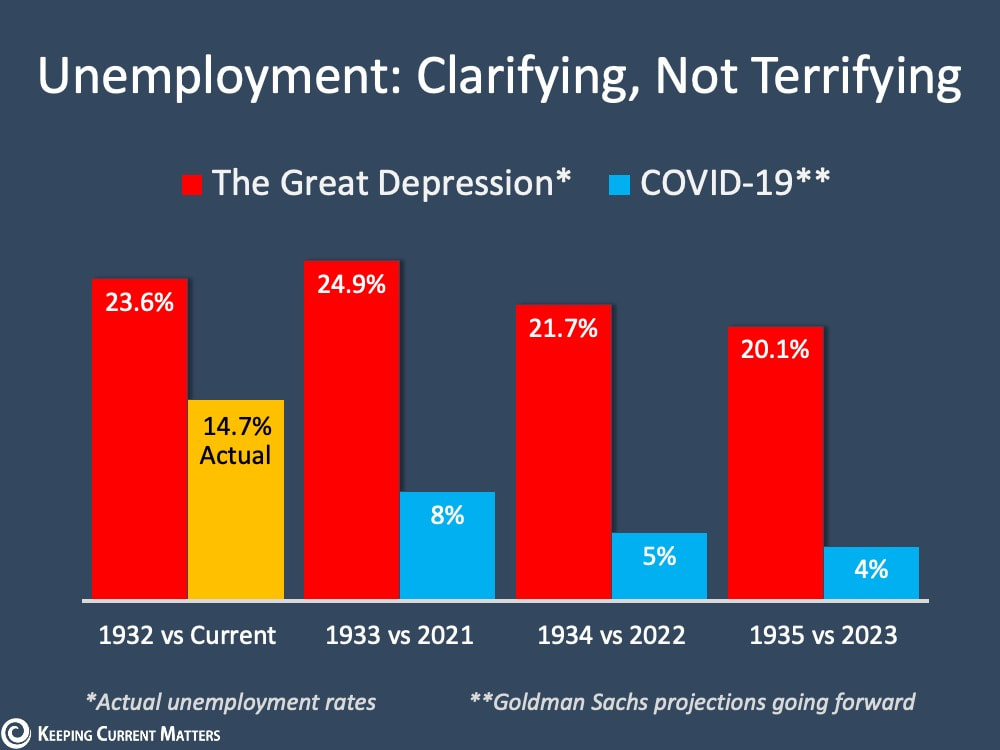

Last Friday, the Bureau of Labor Statistics (BLS) released its latest jobs report. It revealed that the economic shutdown made necessary by COVID-19 caused the unemployment rate to jump to 14.7%. Many anticipate that next month the percentage could be even higher. These numbers represent the extreme hardship so many families are experiencing right now. That pain should not be understated. However, the long-term toll the pandemic will cause should not be overstated either. There have been numerous headlines claiming the current disruption in the economy is akin to the Great Depression, and many of those articles are calling for total Armageddon. Some experts are stepping up to refute those claims. In a Wall Street Journal (WSJ) article this past weekend, Josh Zumbrun, a national economics correspondent for the Journal explained: “News stories often describe the coronavirus-induced global economic downturn as the worst since the Great Depression…the comparison does more to terrify than clarify.” Zumbrun goes on to explain: “From 1929 to 1933, the economy shrank for 43 consecutive months, according to contemporaneous estimates. Unemployment climbed to nearly 25% before slowly beginning its descent, but it remained above 10% for an entire decade…This time, many economists believe a rebound could begin this year or early next year.” Here is a graph comparing current unemployment numbers (actual and projected) to those during the Great Depression:  Clearly, the two unemployment situations do not compare.

What makes this time so different? This was not a structural collapse of the economy, but instead a planned shutdown to help mitigate the virus. Once the virus is contained, the economy will immediately begin to recover. This is nothing like what happened in the 1930s. In the same WSJ article mentioned above, former Federal Reserve Chairman Ben Bernanke, who has done extensive research on the depression in the 1930s, explained: “The breakdown of the financial system was a major reason for both the Great Depression and the 2007-09 recession.” He went on to say that today – “the banks are stronger and much better capitalized.” What about the families and small businesses that are suffering right now? The nation’s collective heart goes out to all. The BLS report, however, showed that ninety percent of the job losses are temporary. In addition, many are getting help surviving this pause in their employment status. During the Great Depression, there were no government-sponsored unemployment insurance or large government subsidies as there are this time. Today, many families are receiving unemployment benefits and an additional $600 a week. The stimulus package is helping many companies weather the storm. Is there still pain? Of course. The assistance, however, is providing much relief until most can go back to work. Bottom Line We should look at the current situation for what it is – a predetermined pause placed on the economy. The country will recover once the pandemic ends. Comparisons to any other downturn make little sense. Bernanke put it best: “I don’t find comparing the current downturn with the Great Depression to be very helpful. The expected duration is much less, and the causes are very different.” SOURCE KCM #HousingMarketUpdate #Covid19 #ForSellersandBuyers #SimardRealtyGroup #joineXpRealty Congrats to the Lawtons! What a great home they just purchased last week in West Granby. I see a lot of homes and this one has one of the best layouts. It was a pleasure working with good friends and getting this home to close. I’m sure many happy memories will be made in your new home.

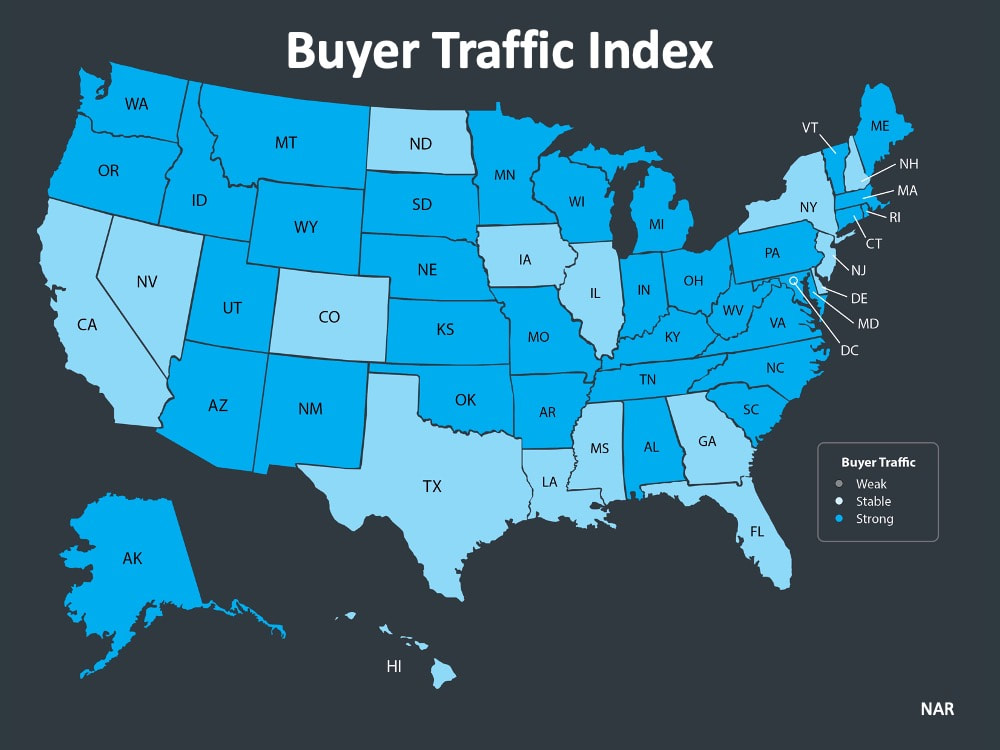

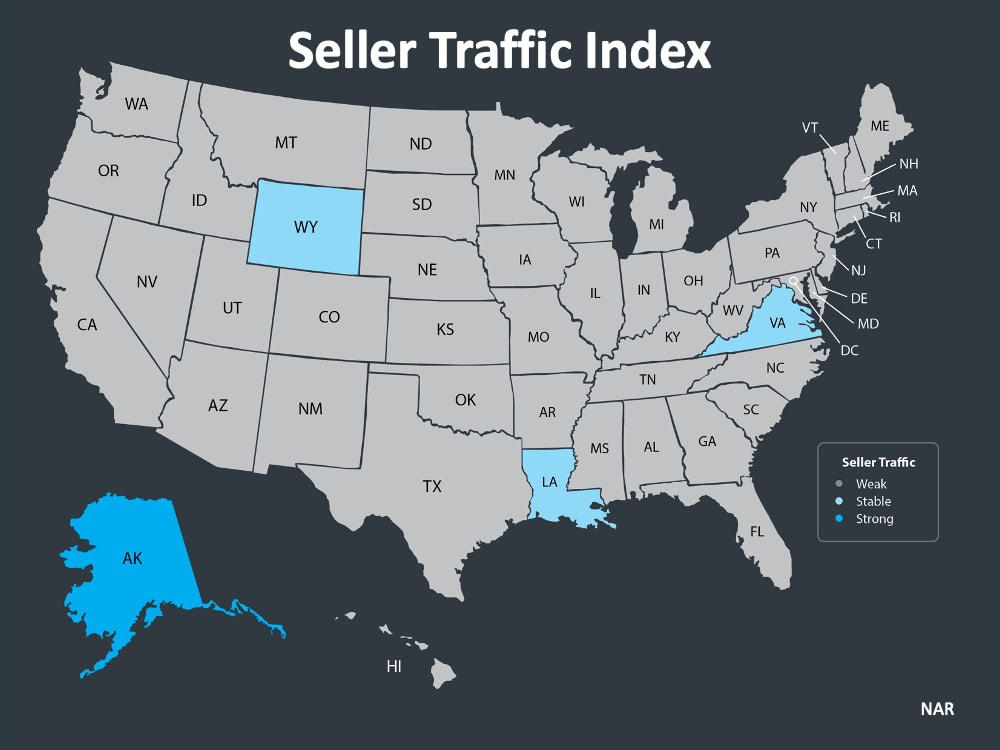

#Sold #HappyClients #Congratulations #SimardRealtyGroup #eXpRealty  With the housing market staggered to some degree by the health crisis the country is currently facing, some potential purchasers are questioning whether home values will be impacted. The price of any item is determined by supply as well as the market’s demand for that item. Each month the National Association of Realtors (NAR) surveys “over 50,000 real estate practitioners about their expectations for home sales, prices and market conditions” for the REALTORS Confidence Index. Their latest edition sheds some light on the relationship between seller traffic (supply) and buyer traffic (demand) during this pandemic. Buyer Demand The map below was created after asking the question: “How would you rate buyer traffic in your area?”  The darker the blue, the stronger the demand for homes is in that area. The survey shows that in 34 of the 50 U.S. states, buyer demand is now ‘strong’ and 16 of the 50 states have a ‘stable’ demand. Seller Supply The index also asks: “How would you rate seller traffic in your area?”  As the map above indicates, 46 states and Washington, D.C. reported ‘weak’ seller traffic, 3 states reported ‘stable’ seller traffic, and 1 state reported ‘strong’ seller traffic. This means there are far fewer homes on the market than what is needed to satisfy the needs of buyers looking for homes right now. With demand still stronger than supply, home values should not depreciate.

What are the experts saying? Here are the thoughts of three industry experts on the subject: Ivy Zelman: “We note that inventory as a percent of households sits at the lowest level ever, something we believe will limit the overall degree of home price pressure through the year.” Mark Fleming, Chief Economist, First American: “Housing supply remains at historically low levels, so house price growth is likely to slow, but it’s not likely to go negative.” Freddie Mac: “Two forces prevent a collapse in house prices. First, as we indicated in our earlier research report, U.S. housing markets face a large supply deficit. Second, population growth and pent up household formations provide a tailwind to housing demand.” Bottom Line Looking at these maps and listening to the experts, it seems that prices will remain stable throughout 2020. If you’re thinking about listing your home, let’s connect to discuss how you can capitalize on the somewhat surprising demand in the market now. SOURCE KCM #HomeValues #Pricing #Buyer #Seller #SimardRealtyGroup #eXpRealty  Price Improved for 9 Candlewood Ln, Granby CT! Now @ $339,900

Check out Candlewood Lane in Granby. Pottery barn decor and neutral paint color throughout. A practical floor plan boasts the perfect blend of casual living and elegance. The kitchen features an island, stainless steel appliances, and a tiled backsplash. The living room features a gas fireplace and hardwood floors. Check full property details here: https://9candlewoodl.thebestlisting.com/ #PriceImproved #Candlewood #Granby #SellingCT #SimardRealtyGroup #joineXpRealty Have you seen the March issue of Connecticut Magazine? Stephen Simard is featured as a 2020 Five Star Real Estate Agent! Be sure to check it out.

Learn more about this award winner here: www.SimardRealtyGroup.com. #TopGranbyRealtor #StephenSimard #ExpRealty #GranbyRealEstate #GranbyConnecticut #FindyourGranbyhome #Newhomesforsale #SimardRealtyGroup #Granbyhomesforsale #JoinExpRealty #Simsburyhomes  Some Highlights

SOURCE KCM #ForBuyers #ForSellers #SimardRealtyGroup #eXpRealty  Tomorrow, the unemployment rate for April 2020 will be released by the U.S. Bureau of Labor Statistics. It will hit a peak this country has never seen before, with data representing real families and lives affected by this economic slowdown. The numbers will alarm us. There will be headlines and doomsday scenarios in the media. There is hope, though, that as businesses reopen, most people will become employed again soon. Last month’s report indicated we initially lost over 700,000 jobs in this country, and the unemployment rate quickly rose to 4.4%. With the release of the new data, that number will climb even higher. Experts forecast this report will show somewhere between a 15% – 20% national unemployment rate, and some anticipate that number to be even greater (see graph below):  What’s happened over the last several weeks? Here’s a breakdown of this spring’s weekly unemployment filings:  The good news shown here indicates the number of additional unemployment claims has decreased week over week since the beginning of April. Carlos Rodriguez, CEO of Automatic Data Processing (ADP) says based on what he’s seeing: “It’s possible that companies are already anticipating some kind of normalization, opening in certain states and starting to post jobs.” He goes on to say that this doesn’t mean all companies are hiring, but it could mean they are at the point where they’re not cutting jobs anymore. Let’s hope this trend continues. What will the future bring? Most experts predict that while unemployment is high right now, it won’t be that way for long. The length of unemployment during this crisis is projected to be significantly shorter than the duration seen in the Great Recession and the Great Depression.  While forecasts may be high, the numbers are trending down and the length of time isn’t expected to last forever.

Bottom Line Don’t let the headlines rattle you. There’s hope coming as we start to safely reopen businesses throughout the country. Unemployment affects our families, our businesses, and our country. Our job is to rally around those impacted and do our part to support them through this time. SOURCE KCM #ForBuyers #ForSellers #HousingMarketUpdates #SimardRealtyGroup #eXpRealty  Concerns about a recession are valid, but know that housing isn’t the driver. This is not 2008 all over again. If you have questions about what it means for your family’s homebuying or selling plans, let’s connect to discuss your needs. Your trusted advisor is here to help.

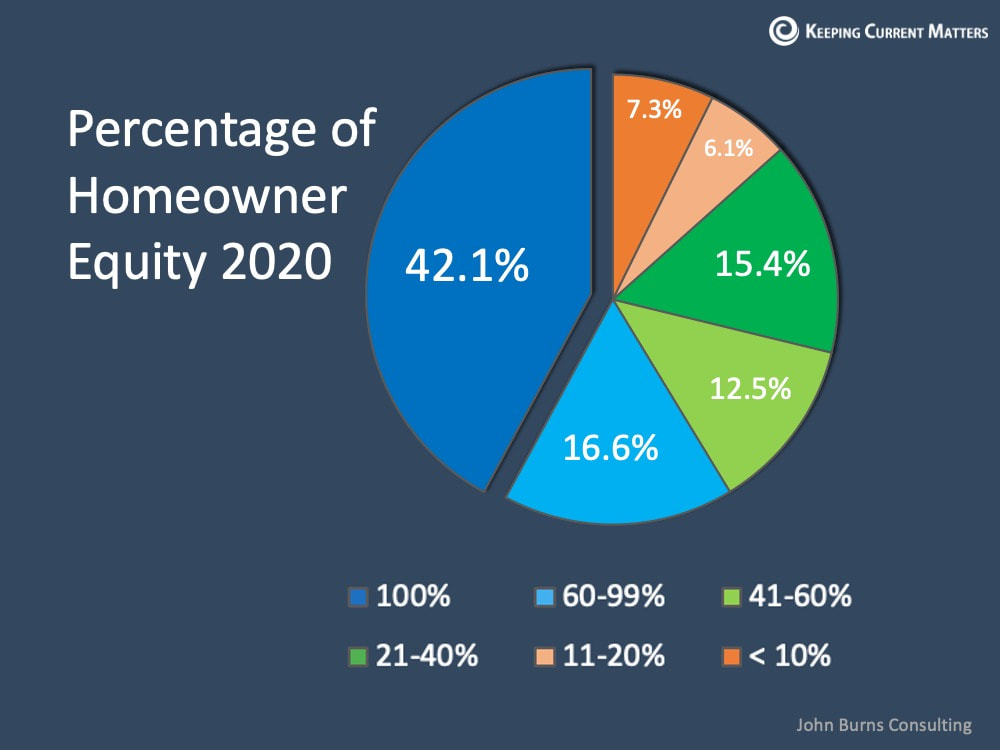

#covid19 #coronavirus #not2008 #realestate #timetobuyahome #homeownership #homebuying #realestategoals #realestatetips #realestatelife #realestatenews #realestateagent #realestateexpert #realestateagency #realestateadvice #realestateblog #realestatemarket #realestateexperts #realestateagents #instarealestate #instarealtor #realestatetipsoftheday #realestatetipsandadvice #keepingcurrentmatters  Given how we have seen more unemployment claims than ever before over the past several weeks, fear is spreading widely. Some good news, however, shows that more than 4 million initial unemployment filers have likely already found a new job, especially as industries such as health care, food and grocery stores, retail, delivery, and more increase their employment opportunities. Breaking down what unemployment means for homeownership, and understanding the significant equity Americans hold today, are important parts of seeing the picture clearly when sorting through this uncertainty. One of the biggest questions right now is whether this historic unemployment rate will initiate a new surge of foreclosures in the market. It’s a very real fear. Despite the staggering number of claims, there are actually many reasons why we won’t see a significant number of foreclosures like we did during the housing crash twelve years ago. The amount of equity homeowners have today is a leading differentiator in the current market. Today, according to John Burns Consulting, 58.7% of homes in the U.S. have at least 60% equity. That number is drastically different than it was in 2008 when the housing bubble burst. The last recession was painful, and when prices dipped, many found themselves owing more on their mortgage than what their homes were worth. Homeowners simply walked away at that point. Now, 42.1% of all homes in this country are mortgage-free, meaning they’re owned free and clear. Those homes are not at risk for foreclosure (see graph below):  In addition, CoreLogic notes the average equity mortgaged homes have today is $177,000. That’s a significant amount that homeowners won’t be stepping away from, even in today’s economy (see chart below):  In essence, the amount of equity homeowners have today positions them to be in a much better place than they were in 2008.

Bottom Line The fear and uncertainty we feel right now are very real, and this is not going to be easy. We can, however, see strength in our current market through homeowner equity that has not been there in the past. That may be a bright spark to help us make it through. SOURCE KCM #ForSellers #HousingMarketUpdate #SiamrdRealtyGroup #eXpRealty |

Archives

October 2022

Categories

All

|

RSS Feed

RSS Feed