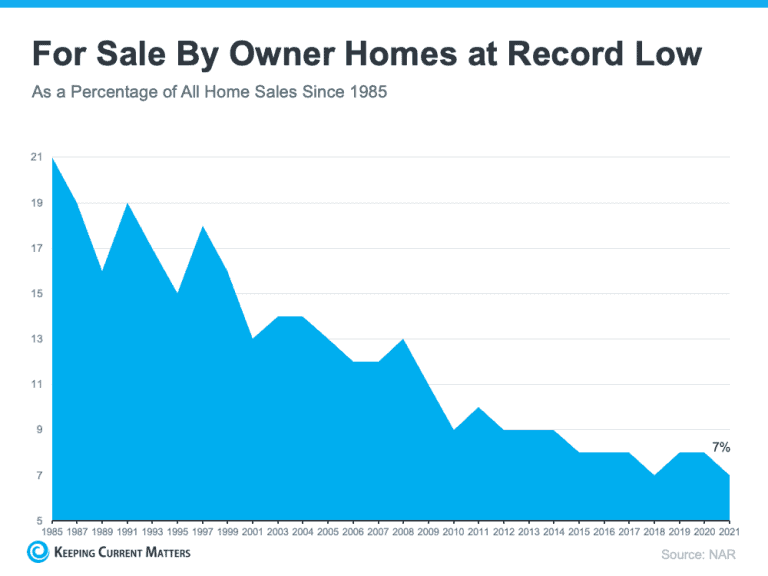

With today’s real estate market moving as fast as it is, working with a real estate professional is more essential than ever. They have the skills, experience, and expertise it takes to navigate the highly detailed and involved process of selling a home. That may be why the percentage of people who list their houses on their own, known as a FSBO or For Sale By Owner, has reached its lowest point since 1985 (see graph below):  Here are five reasons why selling with a real estate professional makes more sense, even in today’s hot market:

1. They Know What Buyers Want To See Before you decide which projects and repairs to take on, connect with a real estate professional. They have first-hand experience with today’s buyers, what they expect, and what you need to do to make sure your house shows well. If you don’t lean on their expertise, you may spend your time and money on something that isn’t essential. That’s because, in today’s low-inventory market, buyers are willing to take on more of the renovation work themselves. A survey from Freddie Mac finds that: “. . . nearly two-in-five potential homebuyers would consider purchasing a home requiring renovations.” A professional can help you decide what you need to tackle. It’s not canned advice you could find online – it’s recommendations specific to your house and your area. 2. They Help Maximize Your Buyer Pool Today, the average home is getting 4.8 offers per sale according to recent data from the National Association of Realtors (NAR), and that competition is pushing prices up. While that’s promising for you as a seller, it’s important to understand your agent’s role in bringing buyers in. Real estate professionals have an assortment of tools at their disposal, such as social media followers, agency resources, and the MLS to ensure your house is viewed by the most buyers. According to realtor.com: “Only licensed real estate agents can list homes on the MLS, which is a one-stop online shop of sorts for getting a house seen by thousands of agents and home buyers. . . . This is certainly one of many good reasons why the majority of home sellers decide to employ the services of a listing agent rather than going it alone.” Without access to these tools, your buyer pool is limited. And you want more buyers to view your house since buyer competition can drive your final sales price higher. 3. They Understand the Fine Print Today, more disclosures and regulations are mandatory when selling a house. That means the number of legal documents you’ll need to juggle is growing. That’s why Investopedia says: “One of the biggest risks of FSBO is not having the experience or expertise to navigate all of the legal and regulatory requirements that come with selling a home.” A real estate professional knows exactly what needs to happen, what all the paperwork means, and how to work through it efficiently. They’ll help you review the documents and avoid any costly missteps that could occur if you try to handle them on your own. 4. They’re Trained Negotiators If you sell without a professional, you’ll also be solely responsible for all the negotiations. That means you’ll have to coordinate with:

Instead of going toe-to-toe with all these parties alone, lean on an expert. They’ll know what levers to pull, how to address everyone’s concerns, and when you may want to get a second opinion. 5. They Know How To Set the Right Price for Your House If you sell your house on your own, you may over or undershoot your asking price. That could mean you’ll leave money on the table because you priced it too low or your house will sit on the market because you priced it too high. Pricing a house requires expertise. Investopedia explains it like this: “. . . There is no easy or universal way to determine market value for real estate.” Real estate professionals know the ins and outs of how to price your house accurately and competitively. To do so, they compare your house to recently sold homes in your area and factor in the current condition of your house. These factors are key to making sure it’s priced to move quickly while still getting you the highest possible final sale price. Bottom Line There’s a lot that goes into selling your house. Instead of tackling it alone, reach out to a trusted real estate advisor to make sure you have an expert on your side throughout the entire process. SOURCE: KCM #ForSellers #FSBOs #Pricing #SellingMyths #SimardRealtyGroup #RealBrokerLLC

0 Comments

If you’re looking to buy your first home, condos could be a great option for you. Condos can offer many amenities, lower maintenance, and an incredible way to break into the housing market and start building equity that can fuel a future move. DM me so we can explore all your options together.

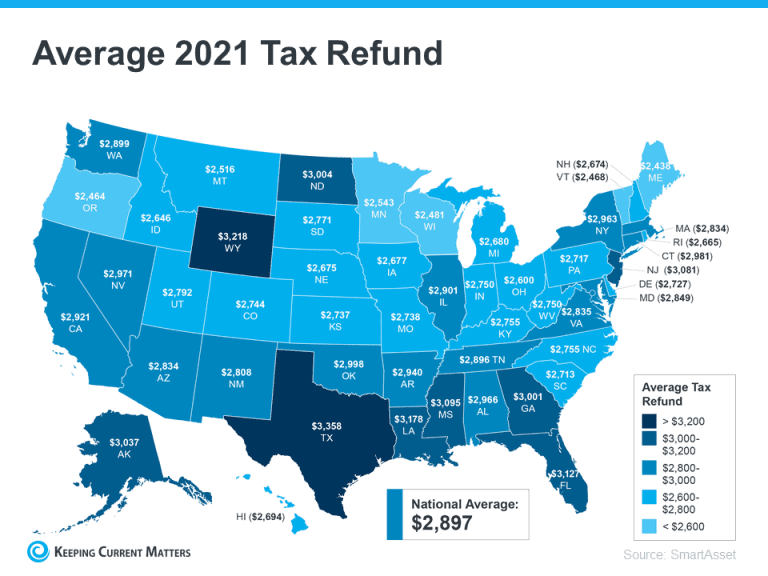

SOURCE: KCM #firsttimehomebuyer #considercondos #condobuying #condominiums #condoliving #housingmarket #househunting #makememove #homegoals #realestatetipsoftheday #realestatetipsandadvice #keepingcurrentmatters #SimardRealtyGroup #RealBrokerLLC  If you’re buying or selling a home this year, you’re likely saving up for a variety of expenses. For buyers, that might include things like your down payment and closing costs. And for sellers, you’re probably working on a bit of spring cleaning and maintenance to spruce up your house before you list it. Either way, any money you get back from your taxes can help you achieve your goals. Using a tax refund is a common tactic for buyers and sellers. SmartAsset estimates the average American will receive a $2,897 tax refund this year. The map below provides a more detailed estimate by state:  If you’re getting a refund this year, here are a few tips to help with your home purchase or sale this season.

How Buyers Can Use Their Tax Refund According to American Financing, there are multiple ways your refund check can help you as a homebuyer. A few include:

This list is a great start, but it isn’t exhaustive of all the costs you may encounter as you set out on your homebuying journey. The best way to prepare is to work with a trusted real estate professional to make sure you understand what’s to come in the process. How Sellers Can Use Their Tax Refund If you own a home and are planning to sell this spring, your tax refund can help you make sure your home is ready to list. Here are a few ways current homeowners can put their tax refund to good use:

Of course, it’s important to talk with your trusted real estate advisor before taking on any projects. They’ll make sure you can focus on areas that’ll help you receive the best possible price when you sell. Bottom Line Funding your home purchase or sale can feel like a daunting task, but it doesn’t have to be. Your tax refund can help you reach your goals. Connect with a local real estate advisor today to discuss how you can start on your journey. SOURCE: KCM #FirstTimeHomeBuyers #ForBuyers #ForSellers #HousingMarketUpdates #Move-UpBuyers #SimardRealtyGroup #RealBrokerLLC  Some Highlights

SOURCE : KCM #ForSellers #HousingMarketUpdates #Infographics #MoveUpBuyers #SimardRealtyGroup #RealBrokerLLC

There are simple ways you can make strong choices when selling your house. Let's connect to make sure you're set up for success when you sell this year.

SOURCE : KCM #StephenSimardRealtor #JoinRealBrokerLLC  Many consumers are wondering what will happen with home values over the next few years. Some are concerned that the recent run-up in home prices will lead to a situation similar to the housing crash 15 years ago. However, experts say the market is totally different today. For example, Odeta Kushi, Deputy Chief Economist at First American, tweeted just last week on this issue: “. . . We do need price appreciation to slow today (it’s not sustainable over the long run) but high price growth today is supported by fundamentals- short supply, lower rates & demographic demand. And we are in a much different & safer space: better credit quality, low DTI [Debt-To-Income] & tons of equity. Hence, a crash in prices is very unlikely.” Price appreciation will slow from the double-digit levels the market has seen over the last two years. However, experts believe home values will not depreciate (where a home would lose value). To this point, Pulsenomics just released the latest Home Price Expectation Survey – a survey of a national panel of over 100 economists, real estate experts, and investment and market strategists. It forecasts home prices will continue appreciating over the next five years. Below are the expected year-over-year rates of home price appreciation based on the average of all 100+ projections:

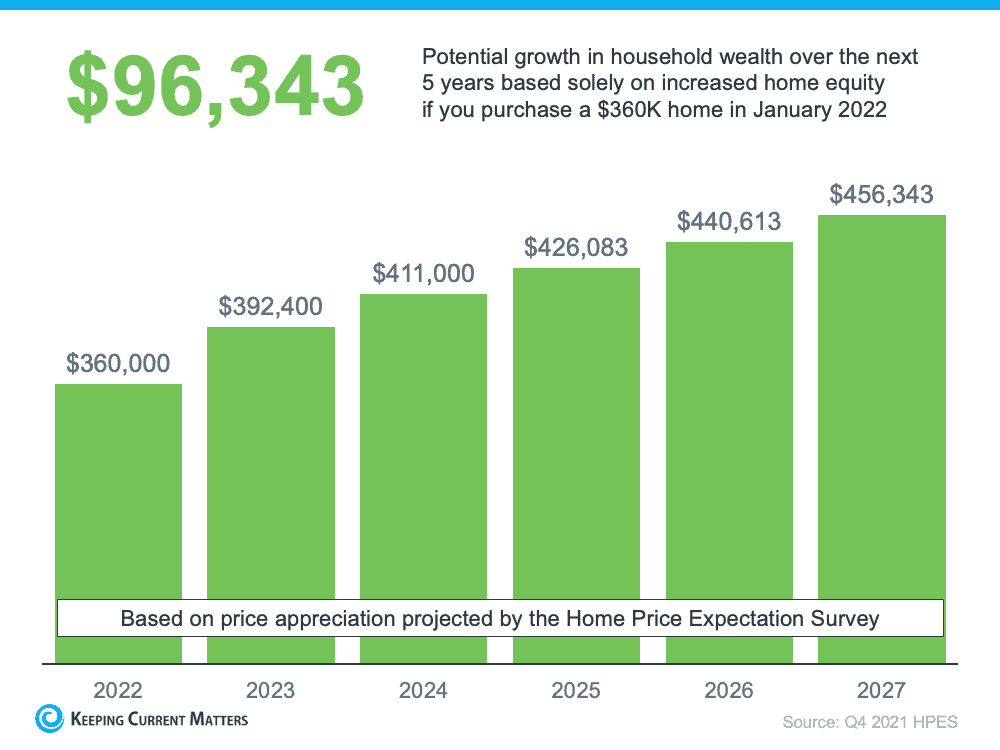

Those responding to the survey believe home price appreciation will still be relatively high this year (though half of what it was last year), and then return to more normal levels over the next four years. What Does This Mean for You as a Buyer? With a limited supply of homes available for sale and both prices and mortgage rates increasing, it can be a challenging market to navigate as a buyer. But buying a home sooner rather than later does have its benefits. If you wait to buy, you’ll pay more in the future. However, if you buy now, you’ll actually be in the position to make future price increases work for you. Once you buy, those rising home prices will help you build your home’s value, and by extension, your own household wealth through home equity. As an example, let’s assume you purchased a $360,000 home in January of this year (the median price according to the National Association of Realtors rounded up to the nearest $10K). If you factor in the forecast for appreciation from the Home Price Expectation Survey, you could accumulate over $96,000 in household wealth over the next five years (see graph below):  Bottom Line

If you’re trying to decide whether to buy now or wait, the key is knowing what’s expected to happen with home prices. Experts say prices will continue to climb in the years ahead, just at a slower pace. So, if you’re ready to buy, doing so now may be your best bet for your wallet. It’ll also give you the chance to use the future home price appreciation to build your own net worth through rising equity. If you want to get started, connect with a real estate professional today. SOURCE : KCM #FirstTimeHomeBuyers #ForBuyers #HousingMarketUpdates #MoveUpBuyers #Pricing #SimardRealtyGroup #RealBrokerLLC  In today’s competitive market, buyers are finding success by being persistent. That’s because data shows that, on average, the third try is the charm when it comes to getting an offer accepted. Stick with your home search and you will find the one. And if you want to partner with an expert who will help you navigate today’s market, DM me.

#housingmarket #housingmarketupdates #firsttimehomebuyer #opportunity #housingmarket #househunting #locationlocationlocation #newlisting #homeownership #homebuying #realestategoals #realestatetips #realestatelife #keepingcurrentmatters #SimardRealtyGroup #RealBrokerLLC  When it comes to buying a home, it can feel a bit intimidating to know how much you need to save and where to find that information. But you should know, you’re not expected to have all the answers yourself. There are many trusted professionals who can help you understand your finances and what you’ll need to budget for throughout the process.

To get you started, here are a few things experts say you should plan for along the way. 1. Down Payment As you set your savings goal for your purchase, your down payment is likely already top of mind. And, like many other people, you may believe you need to set aside 20% of the home’s purchase price for that down payment – but that’s not always the case. The National Association of Realtors (NAR) says: “One of the biggest misconceptions among housing consumers is what the typical down payment is and what amount is needed to enter homeownership. Having this knowledge is critical to know what to save . . .” The good news is, you may be able to put as little as 3.5% (or even 0%) down in some situations. To understand your options, partner with a trusted professional who can go over the various loan types, down payment assistance programs, and what each one requires. 2. Earnest Money Deposit Another item you may want to plan for is an earnest money deposit. While it isn’t required, it’s common in today’s highly competitive market because it can help your offer stand out in a bidding war. So, what is it? It’s money you pay as a show of good faith when you make an offer on a house. This deposit works like a credit. You’re using some of the money you already saved for your purchase to show the seller you’re committed and serious about their house. It’s not an added expense, it’s just paying some of that up front. First American explains what it is and how it works: “The deposit made from the buyer to the seller when submitting an offer. This deposit is typically held in trust by a third party and is intended to show the seller you are serious about purchasing their home. Upon closing the money will generally be applied to your down payment or closing costs.” In other words, an earnest money deposit could be the very first check you’ll write toward your purchase. The amount varies by state and situation. Realtor.com elaborates: “The amount you’ll deposit as earnest money will depend on factors such as policies and limitations in your state, the current market, what your real estate agent recommends, and what the seller requires. On average, however, you can expect to hand over 1% to 2% of the total home purchase price.” Work with a real estate advisor to understand any requirements in your local area and what they’ve recommended for other buyers in your market. They’ll help you determine if it’s something that could be a useful option for you. 3. Closing Costs The next thing to plan for is your closing costs. The Federal Trade Commission (FTC) defines closing costs as: “The upfront fees charged in connection with a mortgage loan transaction. …generally including, but not limited to a loan origination fee, title examination and insurance, survey, attorney’s fee, and prepaid items, such as escrow deposits for taxes and insurance.” Basically, your closing costs cover the fees for various people and services involved in your transaction. NAR has this to say about how much to budget for: “A home costs more than just the sale price. For example, closing costs—which make up about 2% to 5% of the home’s purchase price—are a major added expense…Lenders provide a Closing Disclosure at least three business days prior to closing on a mortgage. But buyers will need to budget for these added costs ahead of time to avoid sticker shock days before closing.” The key takeaway is savvy buyers plan ahead for these expenses so they can come into the process prepared. Freddie Mac sums it up like this: “If you’re in the market to buy a home, your down payment is probably top of mind. And rightly so – it’s likely the biggest cost of homebuying. However, it is not the only cost and it’s critical you understand all your expenses before diving in. The more prepared you are for your down payment, closing and other costs, the smoother your homebuying journey will be.” Bottom Line Knowing what to budget for in the homebuying process is essential. To make sure you understand these and any other expenses that may come up, partner with a real estate advisor for expertise on what to expect when you buy a home. SOURCE : KCM #BuyingMyths #DownPayments #FirstTimeHomeBuyers #ForBuyers #MoveUpBuyers #SimardRealtyGroup #RealBrokerLLC  Since the number of homes for sale is low today, it can feel challenging to find one that checks all your boxes. But if you know which features are absolutely essential in your next home and which ones are just nice bonuses, you can land a home that fits your needs.

Danielle Hale, Chief Economist for realtor.com, explains it like this: “Focus on the goal you set out for yourself, like your list of must-haves and nice-to-haves and your budget, . . . Stick to that. Be persistent.” So how do you go about creating your list of desired features? The first step is to get pre-approved for your mortgage. Pre-approval helps you better understand your budget, and that plays an important role in how you’ll craft your list. After all, you don’t want to fall in love with a home that’s too far out of reach. Once you have a good grasp of your budget, you can begin to list all the features of a home you would like. Here’s a great way to think about them before you begin:

Bottom Line Crafting your home search checklist may seem like a small task, but it can save you time and money. It’s also one of the keys to being successful in today’s competitive market. Connect with a real estate professional so you can work together to find a home that fits your wants and needs. SOURCE KCM #FirstTimeHomeBuyers #ForBuyers #StephenSimard #RealBrokerLLC  Some Highlights

Source: KCM #ForSellers#HousingMarketUpdates#Infographics#SimardRealtyGroup#RealBrokerLLC |

Archives

October 2022

Categories

All

|

RSS Feed

RSS Feed