|

Today's housing market belongs to homeowners ready to sell. Let's connect to talk about why this spring is a great time to sell your house.

#TopGranbyRealtor #StephenSimard #RealBrokerLLC #GranbyRealEstate #GranbyConnecticut #FindyourGranbyhome #Newhomesforsale #SimardRealtyGroup #Granbyhomesforsale #JoinRealBrokerLLC #Simsburyhomes

0 Comments

Today’s housing market belongs to homeowners ready to sell. With the average home receiving multiple offers from buyers, sellers have serious leverage right now to set terms that work for them. DM me today to learn about the best options for selling your house this spring.

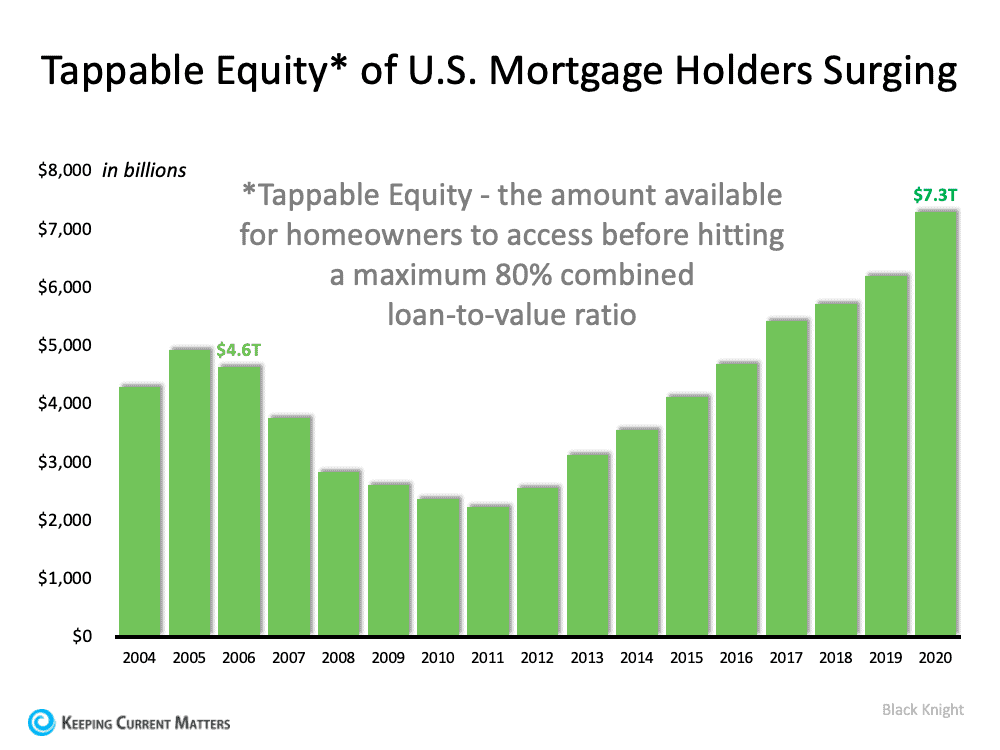

#sellyourhouse #sellersmarket #moveuphome #dreamhome #realestate #homeownership #realestategoals #realestatetips #realestatelife #realestatenews #realestateagent #realestatetipsoftheday #realestatetipsandadvice #justsold #keepingcurrentmatters  Freddie Mac recently released their Quarterly Refinance Statistics report which covers refinances through 2020. The report explains that the dollar amount of cash-out refinances was greater in 2020 than in recent years. A cash-out refinance, as defined by Investopia, is: “a mortgage refinancing option in which an old mortgage is replaced for a new one with a larger amount than owed on the previously existing loan, helping borrowers use their home mortgage to get some cash.” The Freddie Mac report led to articles like the one published by The Real Deal titled, House or ATM? Cash-Out Refinances Spiked in 2020, which reports: “Americans treated their homes like ATMs last year, withdrawing $152.7 billion amid a cash-out refinancing spree not seen since before the 2008 financial crisis.” Whenever you combine the terms “spiked,” “homes like ATMs,” and “financial crisis,” it conjures up memories of the housing crash we experienced in 2008. However, that comparison is invalid for three reasons: 1. Americans are sitting on much more home equity today. Mortgage data giant Black Knight just issued information on the amount of tappable equity U.S. homeowners with a mortgage have. Tappable equity is the amount of equity available for homeowners to use and still have 20% equity in their home. Here’s a graph showing the findings from their report:  In 2006, directly before the crash, tappable home equity in the U.S. topped out at $4.6 trillion. Today, that number is $7.3 trillion.

As Black Knight explains: “At year’s end, some 46 million homeowners held a total $7.3 trillion in tappable equity, the largest amount ever recorded…That’s an increase of more than $1.1 trillion (+18%) since the end of 2019, the largest percentage gain since 2013 and – you guessed it – the largest dollar value gain in history, to boot. All in all, it works out to roughly $158,000 on average per homeowner with tappable equity, up nearly $19,000 from the end of 2019.” 2. Homeowners cashed-out a much smaller amount this time. In 2006, Americans cashed-out a total of $321 billion. In 2020, that number was less than half, totaling $153 billion. The $321 billion made up 7% of the total tappable equity in the country in 2006. On the other hand, the $153 billion made up only 2% of the total tappable equity last year. 3. Fewer homeowners tapped their equity in 2020 than in 2006. Freddie Mac reports that 89% of refinances in 2006 were cash-out refinances. Last year, that number was less than half at 33%. As a percentage of those who refinanced, many more Americans lowered their equity position fifteen years ago as compared to last year. Bottom Line It’s true that many Americans liquidated a portion of the equity in their homes last year for various reasons. However, less than half of them tapped their equity compared to 2006, and they cashed-out less than one-third of that available equity. Today’s cash-out refinance situation bears no resemblance to the situation that preceded the housing crash. SOURCE KCM #ForBuyers #ForSellers #HousingMarketUpdate #SimardRealtyGroup  Don’t let the recent rise in #mortgagerates derail your plans to buy a home. In reality, rates are still lower than they’ve been in decades. DM me to get started on the homebuying process and still get a great mortgage rate.

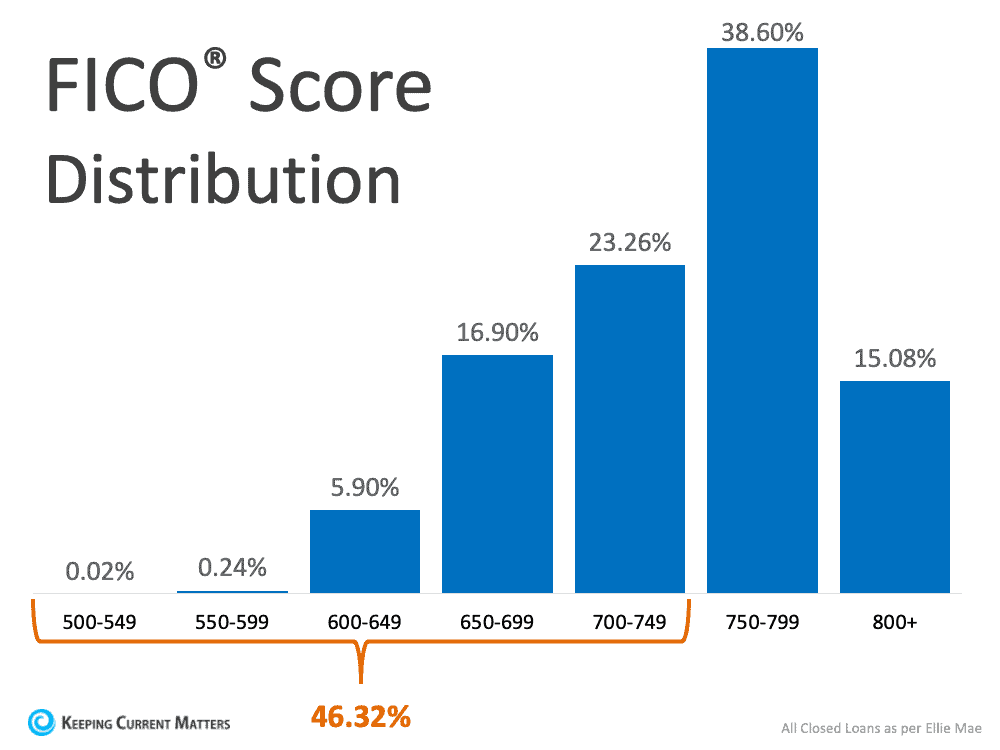

#interestrates #recordlowrates #buyingahome #homebuying #firsttimehomebuyer #opportunity #housingmarket #househunting #makememove #homegoals #houseshopping #housegoals #dreamhome #keepingcurrentmatters  According to data from the most recent Origination Insight Report by Ellie Mae, the average FICO® score on closed loans reached 753 in February. As lending standards have tightened recently, many are concerned over whether or not their credit score is strong enough to qualify for a mortgage. While stricter lending standards could be a challenge for some, many buyers may be surprised by the options that are still available for borrowers with lower credit scores. The fact that the average American has seen their credit score go up in recent years is a great sign of financial health. As someone’s score rises, they’re building toward a stronger financial future. As more Americans with strong credit enter the housing market, we see a natural increase in the FICO® score distribution of closed loans, as shown in the graph below:  If your credit score is below 750, it’s easy to see this data and fear that you may not be able to qualify for a mortgage. However, that’s not always the case. While the majority of borrowers right now do have a score above 750, there’s more to qualifying for a mortgage than just the credit score, and there are still options that allow people with lower credit scores to buy their dream home. Here’s what Experian, a global leader in consumer and business credit reporting, says:

Bottom Line Don’t let assumptions about whether your credit score is strong enough put a premature end to your homeownership goals. Contact your local real estate professional today to discuss the options that are best for you. SOURCE: KCM #BuyingMyths #ForBuyers #SimardRealtyGroup #RealBrokerLLC  If you’re ready to sell your house, there’s no need to wait for the best time to do so – it’s already here. Buyers are in the market waiting eagerly for your home. DM me today so we can get started on the best plan for selling your house this spring.

#timetosell #expertanswers #stayinformed #staycurrent #powerfuldecisions #confidentdecisions #realestate #homevalues #homeownership #realestatelife #realestatenews #realestateagent #realestatemarket #realestateexperts #keepingcurrentmatters  Some Highlights

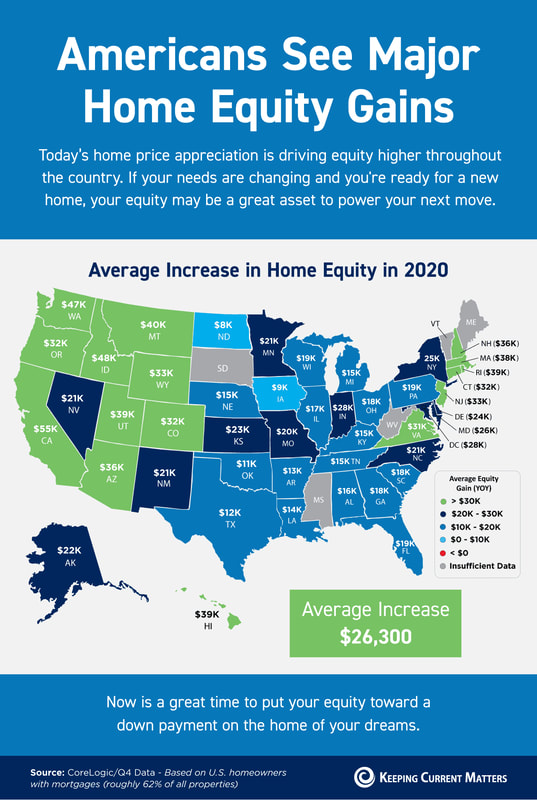

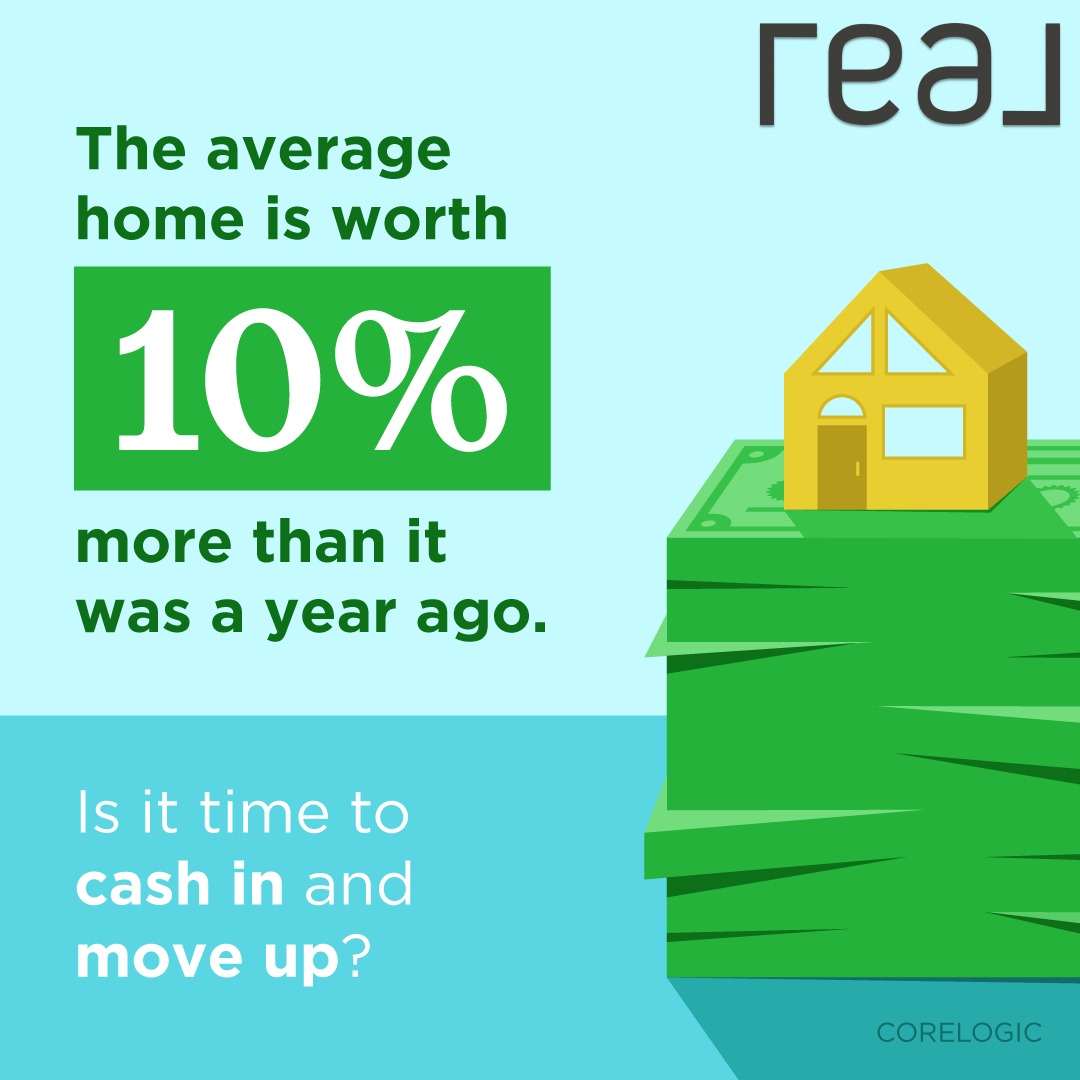

SOURCE KCM #ForSellers #HousingMarketUpdate #Pricing #SimardRealtyGroup  The average home is worth almost 10% more than it was a year ago. If you own a home, this surge in value has gone straight into your pocket as #equity. Equity can be used to fund major life events, including your next move. DM me to learn more about your home equity and how it can help you accomplish your real estate goals.

#homeequity #homeprices #homevalues #sellyourhouse #timetomove #dreamhome #moveuphome #realestate #homeownership #realestategoals #realestatetips #realestatetipsoftheday #realestatetipsandadvice #keepingcurrentmatters  When thinking about selling, homeowners often feel they need to get their house ready with some remodeling to make it more appealing to buyers. However, with so many buyers competing for available homes right now, renovations may not be as vital as they would be in a more normal market. Here are two things to keep in mind if you’re thinking of selling this season.

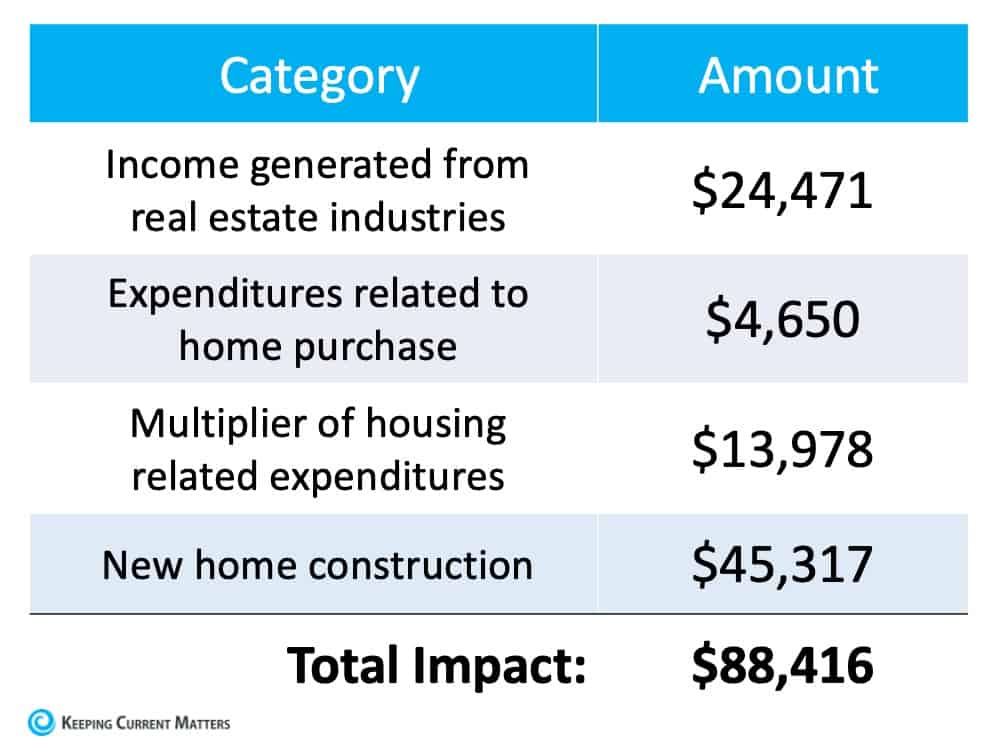

1. There aren’t enough homes for sale right now. A normal market has a 6-month supply of houses for sale, but today’s housing inventory sits far below that benchmark. According to the National Association of Realtors (NAR), there’s only a 1.9-month supply of homes available today. As a result, buyer competition is high and homes are only on the market for about 21 days, during which time many receive multiple offers from hopeful buyers. In a competitive market that’s moving so quickly, it makes sense to sell your house when buyers are scooping homes up as fast as they’re being listed. Spending costly time and money on renovations before you sell might just mean you’ll miss your key window of opportunity. While certain repairs on your house may be important, your best move right now is to work with a real estate advisor to determine which improvements are truly necessary, and which ones are not likely to be deal-breakers for buyers. Today, many buyers are more willing to take on home improvement projects themselves in order to get the home they’re after, even if it means putting in a little extra work. Home Advisor explains: “When it comes to the number of home improvement projects completed, Gen Z homeowners are leading the pack, completing an average of 3.5 projects. Millennials closely follow Gen Z, taking on an average of 3.3 projects, followed by Gen X at 2.8 projects. Boomers completed an average of 2 projects, and the Silent Generation completed the fewest projects, on average, at 1.8 per household. Compared to 2019, millennials are spending 60% more on home improvement and doing on average 30% more projects.” In this market, it may be wise to let future homeowners remodel the bathroom or the kitchen to make design decisions that are best for their specific taste and lifestyle. As a seller, your dollars and time might be better spent working on small cosmetic updates, like refreshing some paint and power washing the exterior. Instead of over-investing in your home with upgrades that the buyers may change anyway, work with a real estate professional to determine the key projects that will maximize your listing, without overdoing it. 2. Focus on getting a good return on your investment. When planning any bigger projects to tackle, you and your real estate agent will want to discuss the potential return on your investment and if those projects are worth the cost. Some homes do need a kitchen or bathroom renovation, roof repairs, or other major work, but definitely not all of them. You might be surprised by how well your house could fair in today’s sellers’ market. Hanley Wood states: “The 2020 Cost vs. Value report shows a predictable increase in costs for all 22 remodeling projects but a consistent dip in the perceived value of those projects at the time of home sale, as estimated by real-estate professionals in more than 100 metro areas across the U.S. This results in a slight downturn on the return on investment for nearly all projects relative to the trends we saw in last year’s report.” Ideally, homeowners getting ready to move should try to avoid over-investing in big renovations if they won’t make that money back when they sell their house. According to the 2020 State of Home Spending report from Home Advisor: “The average household spending on home services rose to $13,138, an increase over last year’s survey results, where homeowners who did projects spent $9,081 on average in 2019.” Before you renovate, contact a local real estate professional to see if it’s the best course of action. You may find out that putting your house on the market as-is will help you sell quickly, and it may result in the best return on your investment. Every home is different, but a conversation with your agent is mission-critical to make sure you make the right moves when selling this season. Bottom Line We’re in a strong sellers’ market, and that means you have the leverage to sell your house on your terms. Talk with a local real estate professional today to determine if renovating is really the best way to spend your time and money before you sell. SOURCE KCM #ForSellers #Pricing #SellingMyths #SimardRealtyGroup  Last year started off with a bang. Unemployment was under 4%, forecasters were giddy with their projections for the economy, and the residential housing market had the strongest January and February activity in over a decade. Then came the announcement on March 11, 2020, from the World Health Organization declaring COVID-19 a worldwide pandemic. Two days later, the White House declared it a national emergency. Businesses and schools were forced to close, shelter-in-place mandates were enacted, and the economy came to a screeching halt. As a result, unemployment in this country skyrocketed to 14.9%. A year later, the economy is recovering, and the U.S. has regained more than half of the jobs that were originally lost. However, some businesses are still closed, and many schools are still struggling to reopen. Despite the past and current challenges, there is one industry that’s proven to be a tailwind helping to counter all of these headwinds to our economy. That industry is housing. Remarkably, the residential real estate market (including existing homes and new construction) has flourished over the last twelve months. Sales are up, prices are appreciating, and more new homes are being built. The housing market has been a pillar of strength in an otherwise slowly recovering economy. How does the real estate market help the economy? At the beginning of the pandemic, the National Association of Realtors (NAR) released a report that explained: “Real estate has been, and remains, the foundation of wealth building for the middle class and a critical link in the flow of goods, services, and income for millions of Americans. Accounting for nearly 18% of the GDP, real estate is clearly a major driver of the U.S. economy.” The report calculated the total economic impact of real estate-related industries on the economy as well as the expenditures that resulted from a single home sale. At a national level, their research revealed that a single newly constructed home had an economic impact of $88,416. Here’s how it breaks down:   The impact of an existing home sale is approximately $40,000.

Real estate has done more for our economic wellbeing than virtually any other industry over the last year. It’s been a beacon of light during a very challenging time in our nation’s history. Bottom Line Whether you’re buying a newly constructed home or one that already exists, you’re making a positive economic impact in your local community – and it’s a step toward your homeownership goals as well. SOURCE KCM #NewConstruction #ForSeller #ForBuyer #SimardRealtyGroup |

Archives

October 2022

Categories

All

|

RSS Feed

RSS Feed