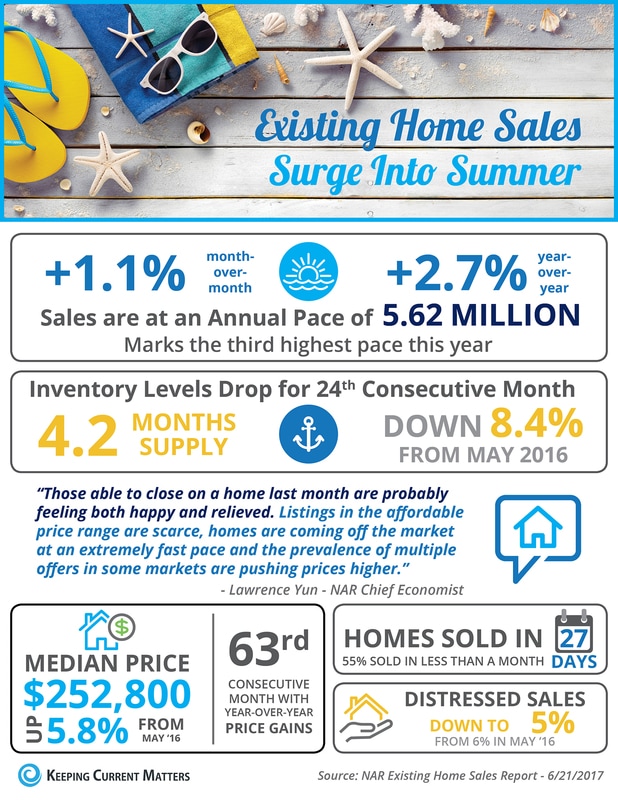

Some Highlights:

SOURCE KCM #HomeSales #Summer #SimardRealtyGroup #ExpRealty

0 Comments

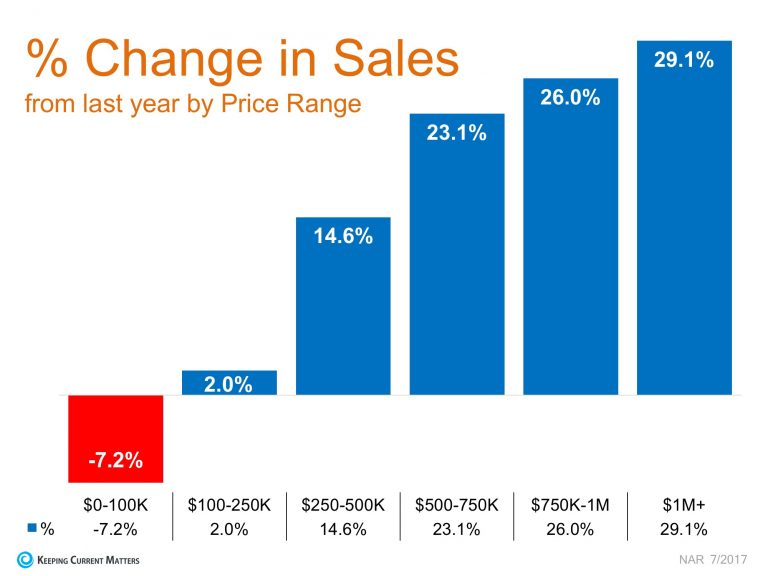

We previously reported how a shortage of inventory in the starter and trade-up home markets is driving prices up and causing bidding wars, creating a true seller’s market. At the same time, in the premium home market, an over-abundance of inventory has started to see prices come down and put buyers in the driver’s seat, creating the beginning of a buyer’s market. Last week, the National Association of Realtors released their Existing Home Sales Report which shed some additional light on the impact of inventory levels on sales in each price range. The chart below shows the year-over-year difference in sales at each price range.  The under $100K range has shown declines in recent years due to the shortage of distressed homes available for sale (just 5% of sales this past month, compared to 35% in January 2012). Sales in the next two price ranges are no doubt being hindered by low inventory as buyers compete for the same home.

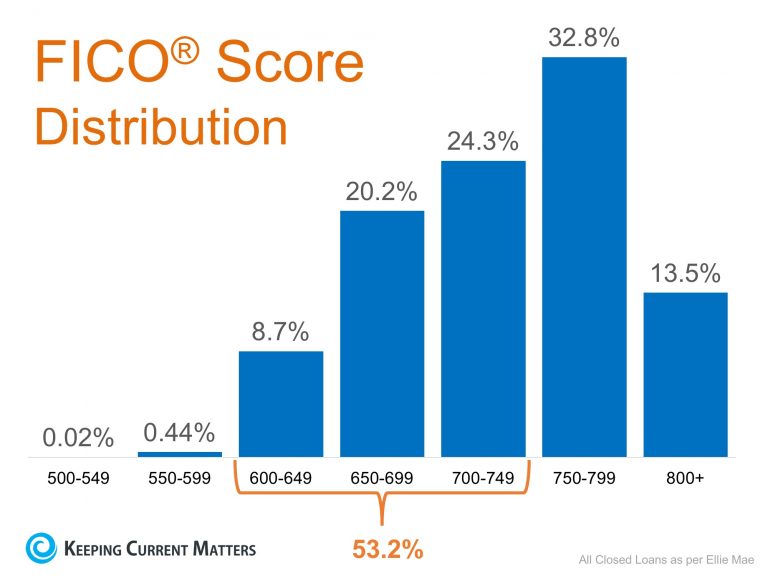

NAR’s Chief Economist, Lawrence Yun, explained: "Those able to close on a home last month are probably feeling both happy and relieved. Listings in the affordable price range are scarce, homes are coming off the market at an extremely fast pace and the prevalence of multiple offers in some markets are pushing prices higher." The biggest surprise? This is the first time in years where the $1M and up price range had the highest jump in sales when compared to last year and to all other price ranges (29.1%)! The two price ranges right underneath the $1M range were a close second and third. As the price went up, so did the sales! With additional inventory available in the higher price ranges, and the economy improving, many luxury buyers are finding it easier to find their dream homes. Yun commented, “The job market in most of the country is healthy and the recent downward trend in mortgage rates continues to keep buyer interest at a robust level.” Bottom Line If you are one of the many homeowners who is looking to sell your starter or trade up home and move up to a luxury home, now is the time! SOURCE KCM #Forbuyers #ForSellers #HomeSales #SimardRealtyGroup #JoinExpRealty  In Realtor.com’s recent article, “Home Buyers’ Top Mortgage Fears: Which One Scares You?” they mention that “46% of potential home buyers fear they won’t qualify for a mortgage to the point that they don’t even try.” Myth #1: “I Need a 20% Down Payment”Buyers overestimate the down payment funds needed to qualify for a home loan. According to the First Quarter 2017 Homeownership Program Index (HPI) from Down Payment Resource, saving for a down payment was the barrier that kept 70% of renters from buying. Rob Chrane, CEO of Down Payment Resource had this to say, “There are many mortgage-ready renters today, but they don’t know it. Often, homebuyers remain sidelined for years due to the down payment.” Many believe that they need at least 20% down to buy their dream home, but programs are available that allow buyers put down as little as 3%. Many renters may actually be able to enter the housing market sooner than they ever imagined with new programs that have emerged allowing less cash out of pocket. Myth #2: “I Need a 780 FICO® Score or Higher to Buy” The survey revealed that 59% of Americans either don’t know (54%) or are misinformed (5%) about what FICO® score is necessary to qualify. Many Americans believe a ‘good’ credit score is 780 or higher. To help debunk this myth, let’s take a look at Ellie Mae’s latest Origination Insight Report, which focuses on recently closed (approved) loans.  As you can see in the chart above, 53.2% of approved mortgages had a credit score of 600-749.

Bottom Line Whether buying your first home or moving up to your dream home, knowing your options will make the mortgage process easier. Your dream home may already be within your reach. SOURCE KCM #ForBuyers #SimardRealtyGroup #JoinExpRealty  Congrats to our buyers for putting this lovely home under contract!

#UnderContract #Stafford #SimardRealtyGroup #JoinExpRealty  Some Highlights:

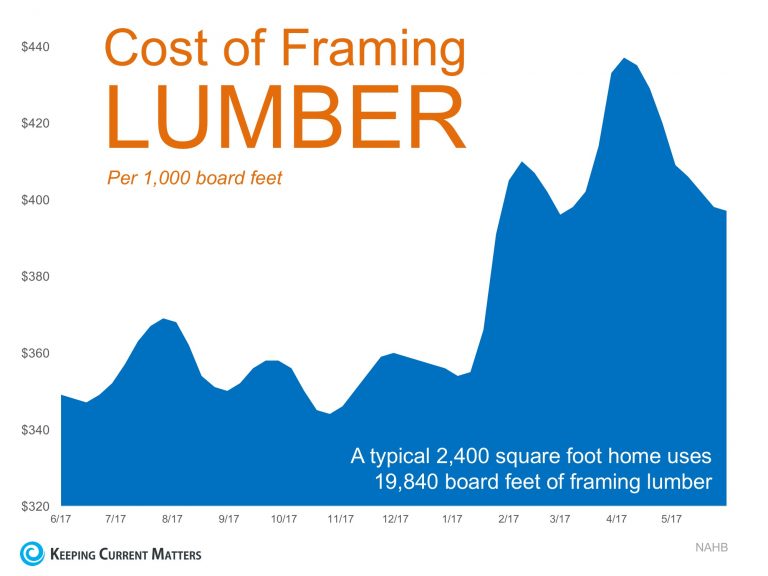

SOURCE KCM #ForBuyers #Infographics #SimardRealtyGroup #ExpRealty  Many real estate economists have called on new home builders to ramp up production to help relieve the shortage of inventory of homes for sale throughout the United States. The added inventory would no doubt aid buyers in their search to secure their dream home, while also helping to ease price increases throughout the country. Unfortunately for builders, there are many forces that are making it difficult for them to do just that! Last week at the National Association of Real Estate Editors 51st Annual Conference,CoreLogic’s Chief Economist Frank Nothaft broke down the 4 ‘L’s of New Home Construction: Lots, Labor, Lumber, and Lending. The concept of supply and demand is ripe in the new home construction industry. The four ‘L’s of new home construction are each suffering a supply problem, and with that comes added costs. Let’s break it down! Lots – There is a shortage of land near metros at an affordable price, causing builders to move farther and farther away from cities to keep costs down. This isn’t always an attractive option for those who want to stay close to work. Labor – The Great Recession forced many skilled construction and trade workers to find other sources of income once their jobs were lost at the time of the crash. Even though the overall housing market has recovered, these workers have not returned. Those who remain are starting to age out and retire, causing even more of a shortage and additional costs. Lumber – The cost to build a new home is directly tied to the cost of the lot and the cost of the supplies needed to build the home. Lumber costs continue to escalate due to policies restricting the importation of Canadian lumber, making larger luxury homes an attractive option to recoup costs when selling, rather than building smaller single-family homes and making less profit. Below is a graph showing the increase in cost of 1,000 board feet of framing lumber.  Year-over-year, lumber costs are up 13% after reaching a high of $433 in the second week of April.

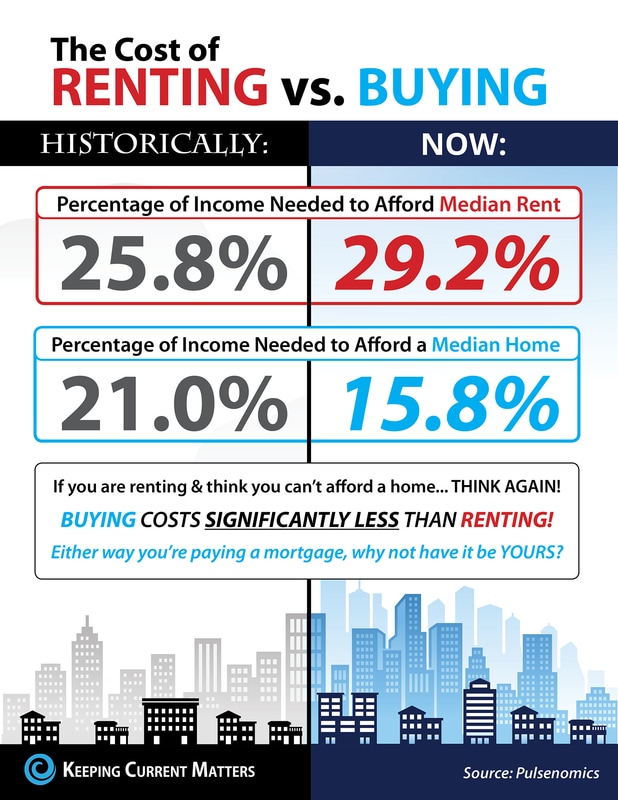

Lending – During the Great Recession, many small community banks were forced to close their doors. These banks were a great source of capital and lending for builders looking to borrow money at a low interest rate in the community in which they were building. Tougher lending standards have made borrowing funds more expensive and more difficult for builders. Bottom Line Additional costs across all 4 ‘L’s have made building luxury properties more attractive to builders as they are able to make a larger margin with the higher sales price. The move to scale down to starter and trade up homes to help with supply will mean any additional costs are absorbed by the builders unless the supply of the 4 ‘L’s can increase! SOURCE KCM #NewConstruction #HousingMarketUpdates #SimardRealtyGroup #JoinExpRealty  The results of the latest Rent vs. Buy Report from Trulia show that homeownership remains cheaper than renting with a traditional 30-year fixed rate mortgage in the 100 largest metro areas in the United States.

The updated numbers actually show that the range is an average of 3.5% less expensive in San Jose (CA), all the way up to 50.1% less expensive in Baton Rouge (LA), and 33.1% nationwide! Other interesting findings in the report include:

Bottom Line Buying a home makes sense socially and financially. If you are one of the many renters out there who would like to evaluate your ability to buy this year, meet with a local real estate professional who can help you find your dream home. SOURCE KCM #Buyers #HousingMarketUpdate #SimardRealtyGroup #ExpRealty Congrats to our sellers! looking forward to a smooth closing! Cheers! 🥂🥂🥂

The perfect blend of location, style, and living space, this home is the one you have been looking for. An inviting sun filled open floor plan with Pottery barn colors, refinished hardwood floors, 9' ceilings, and a complete remodel, this home is like new. http://224mountainbrookdrive.thebestlisting.com/  Some Highlights:

SOURCE KCM #ForBuyers #ForSellers #Infographics #SimardRealtyGroup #ExpRealty  In a blog post published last Friday, CNN’s Diana Olnick reported on the latest results of the FAU Buy vs. Rent Index. The index examines that entire US housing market and then isolates 23 major markets for comparison. The researchers at FAU use a “‘horse race’ comparison between an individual that is buying a home and an individual that rents a similar-quality home and reinvests all monies otherwise invested in homeownership.”

Having read both the index and the blog post, we would like to clear up any confusion that may exist. There are three major points that we would like to counter: 1. The Title The CNN blog post was titled, “Don’t put your money in a house, says a new report.”The title of the press release about the report on FAU’s website was “FAU Buy vs. Rent Index Shows Rising Prices and Mortgage Rates Moving Housing Markets in the Direction of Renting.” Now, we all know headlines can attract readers and the stronger the headline the more readership you can attract, but after dissecting the report, this headline may have gone too far. The FAU report notes that rising home prices and the threat of increasing mortgage rates could make the decision of whether to rent or to buy a harder one in three metros, but does not say not to buy a home. 2. Mortgage Interest Rates are Rising According to Freddie Mac, mortgage interest rates reached their lowest mark of 2017 last week at 3.89%. Interest rates have hovered around 4% for the majority of 2017, giving many buyers relief from rising home prices and helping with affordability. While experts predict that rates will increase by the end of 2017, the latest projections have softened, with Freddie Mac predicting that rates will rise to 4.3% in Q4. 3. “Renting may be a better option than buying, according to the report.” Of the 23 metros that the study reports on, 11 of them are firmly in buy territory, including New York, Boston, Chicago, Cleveland, and more. This means that in nearly half of all the major cities in the US, it makes more financial sense to buy a home than to continue renting one. In 9 of the remaining metros, the decision as to whether to rent or buy is closer to a toss-up right now. This means that all things being equal, the cost to rent or buy is nearly the same. That leaves the decision up to the individual or family as to whether they want to renew their lease or buy a home of their own. The 3 remaining metros Dallas, Denver and Houston, have experienced high levels of price appreciation and have been reported to be in rent territory for well over a year now, so that’s not news… Beer & Cookies One of the three authors of the study, Dr. Ken Johnson has long reported on homeownership and the decision between renting and buying a home. The methodology behind the report goes on to explain that even in a market where a renter would be able to spend less on housing, they would have to be disciplined enough to reinvest their remaining income in stocks/bonds/other investments for renting a home to be a more attractive alternative to buying. Johnson himself has said: “However, in perhaps a more realistic setting where renters can spend on consumption (beer, cookies, education, healthcare, etc.), ownership is the clear winner in wealth accumulation. Said another way, homeownership is a self-imposed savings plan on the part of those that choose to own.” Bottom Line In the end, you and your family are the only ones who can decide if homeownership is the right path to go down. Real estate is local and every market is different. Meet with a local real estate professional who can explain what’s really going on in your area and can help you make the best, most informed decision for you and your family. SOURCE KCM #ForBuyers #RentingVSBuying #SimardRealtyGroup #ExpRealty |

Archives

October 2022

Categories

All

|

RSS Feed

RSS Feed