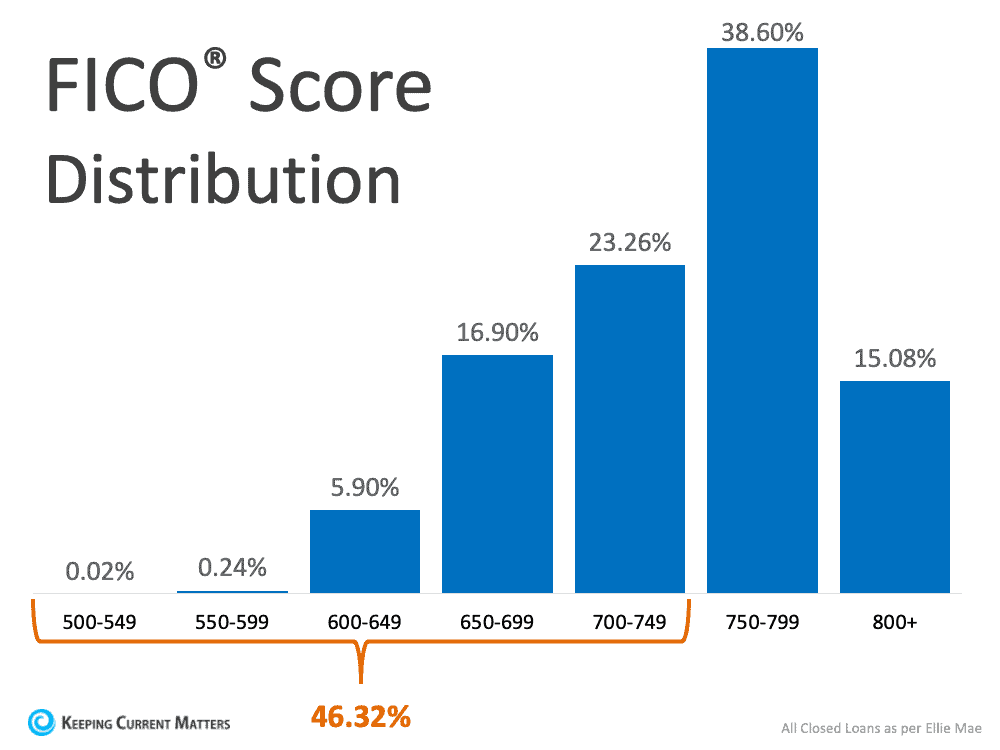

According to data from the most recent Origination Insight Report by Ellie Mae, the average FICO® score on closed loans reached 753 in February. As lending standards have tightened recently, many are concerned over whether or not their credit score is strong enough to qualify for a mortgage. While stricter lending standards could be a challenge for some, many buyers may be surprised by the options that are still available for borrowers with lower credit scores. The fact that the average American has seen their credit score go up in recent years is a great sign of financial health. As someone’s score rises, they’re building toward a stronger financial future. As more Americans with strong credit enter the housing market, we see a natural increase in the FICO® score distribution of closed loans, as shown in the graph below:  If your credit score is below 750, it’s easy to see this data and fear that you may not be able to qualify for a mortgage. However, that’s not always the case. While the majority of borrowers right now do have a score above 750, there’s more to qualifying for a mortgage than just the credit score, and there are still options that allow people with lower credit scores to buy their dream home. Here’s what Experian, a global leader in consumer and business credit reporting, says:

Bottom Line Don’t let assumptions about whether your credit score is strong enough put a premature end to your homeownership goals. Contact your local real estate professional today to discuss the options that are best for you. SOURCE: KCM #BuyingMyths #ForBuyers #SimardRealtyGroup #RealBrokerLLC

0 Comments

Leave a Reply. |

Archives

October 2022

Categories

All

|

RSS Feed

RSS Feed