Buying a home in today’s fast-paced market can be challenging. And since it’s one of the most important purchases in anyone’s life, there’s going to be an emotional element to the process. Working with an expert ensures your emotions don’t get the best of you. DM me today so we can walk through the process together.

#bestdecision #hanginthere #buyingahome #firsttimehomebuyer #househunting #makememove #homegoals #houseshopping #inspiration #mindovermatter #motivation #mindset #inspiredaily #homesweethome #keepingcurrentmatters #

0 Comments

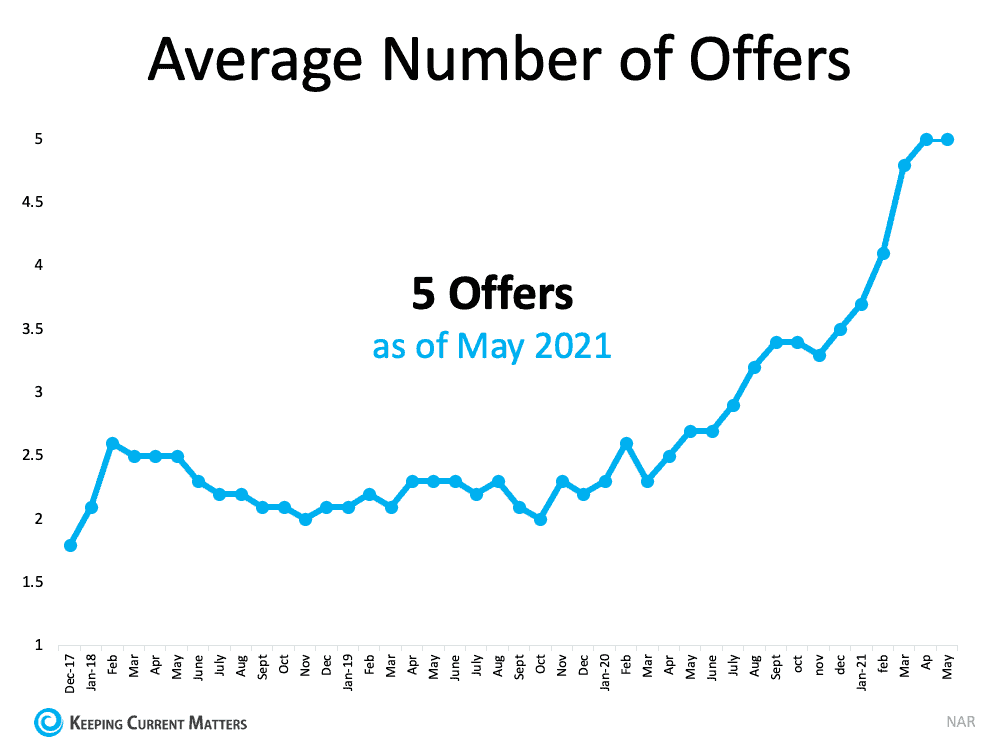

As we move into the second half of the year, one thing is clear: the current real estate market is one for the record books. The exact mix of conditions we have today creates opportunities for both buyers and sellers. Here’s a look at four key components that are shaping this unprecedented market. A Shortage of Homes for Sale Earlier this year, the number of homes available for sale fell to an all-time low. In recent months, however, inventory levels are starting to trend up. The latest Monthly Housing Market Trends Report from realtor.com says: “In June, newly listed homes grew by 5.5% on a year-over-year basis, and by 10.9% on a month-over-month basis. Typically, fewer newly listed homes appear on the market in the month of June compared to May. This year, growth in new listings is conti nuing later into the summer season, a welcome sign for a tight housing market.” This is good news for buyers who crave more options. But even though we’re experiencing small gains in the number of available homes for sale, inventory remains a challenge in most states. That’s why it’s still a sellers’ market, giving homeowners immense leverage when they decide to make a move. Buyer Competition and Bidding Wars Today’s ongoing low supply, coupled with high demand, creates a market characterized by high buyer competition and bidding wars. Buyers are going above and beyond to make sure their offer stands out from the crowd by offering over the asking price, all cash, or waiving some contingencies. The number of offers on the average house for sale broke records this year – and that’s great news for sellers. The latest Confidence Index from the National Association of Realtors (NAR) says the average home for sale receives five offers (see graph below):  For buyers, the best way to put a compelling offer together is by working with a local real estate professional. That agent can act as your trusted advisor on what terms are best for you and what’s most appealing to the seller.

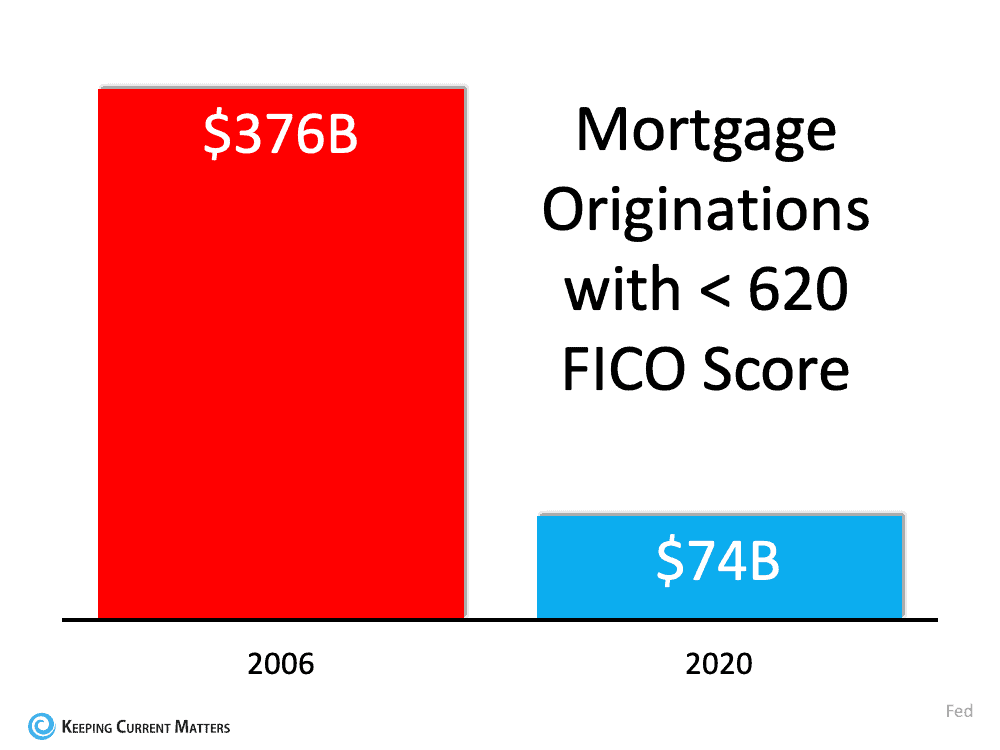

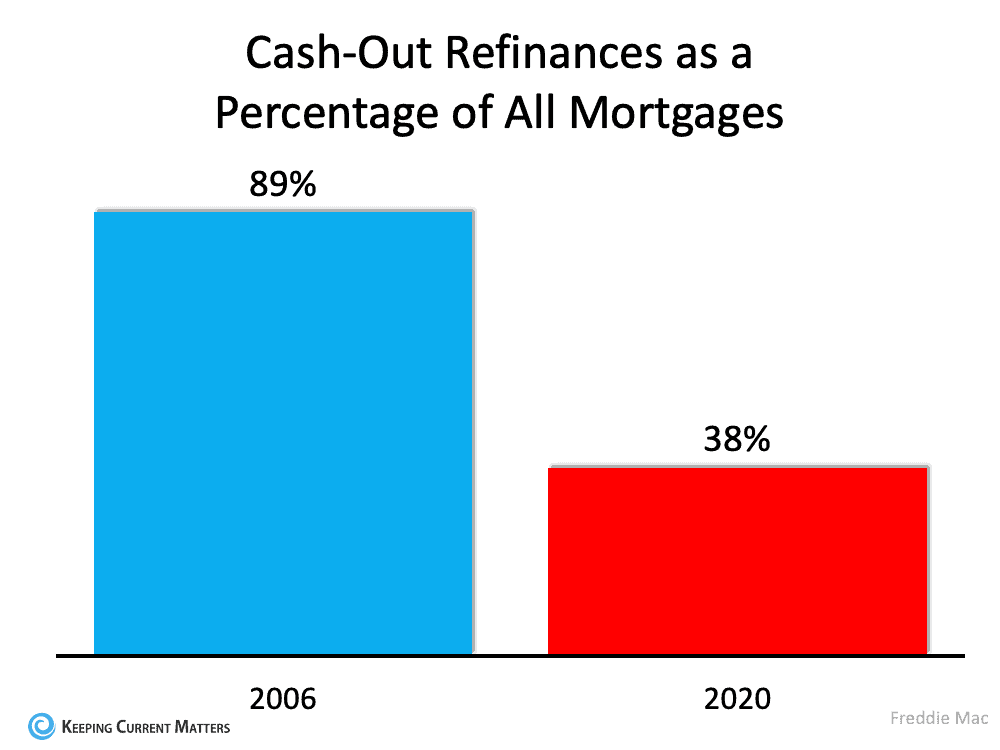

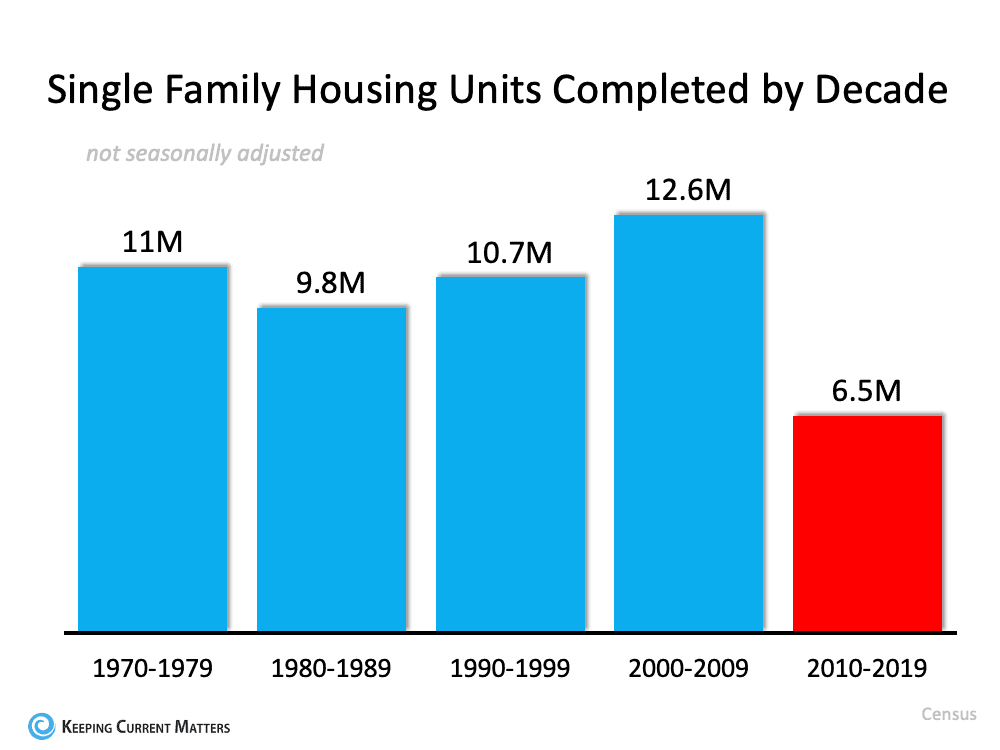

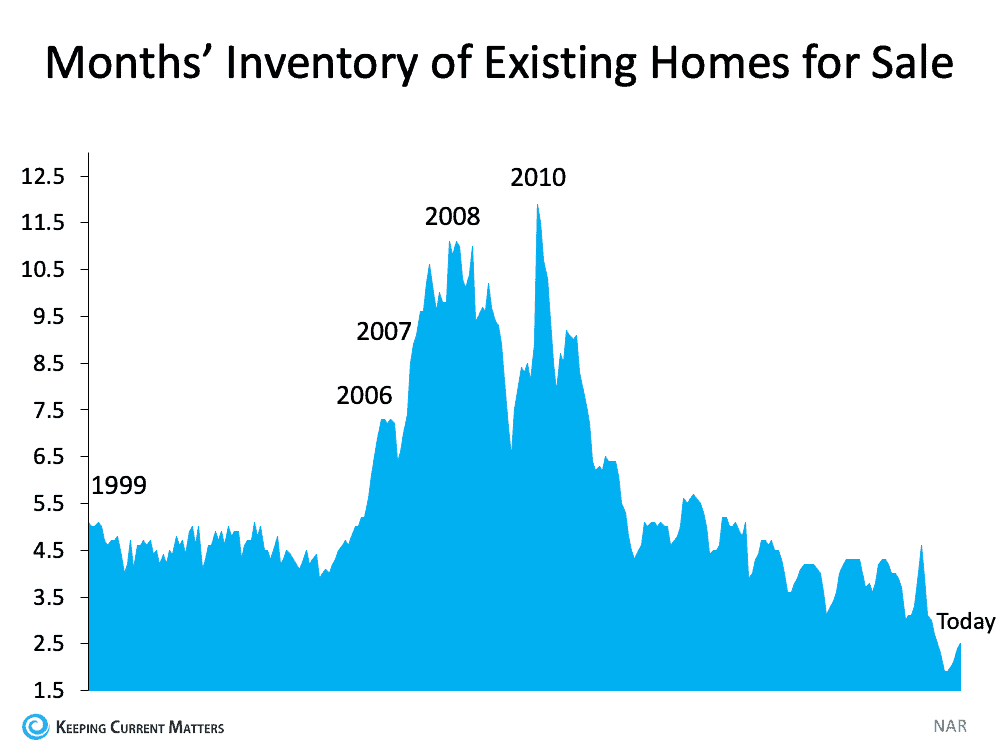

Home Price Appreciation The competition among buyers is driving prices up. Over the past year, we’ve seen home price appreciation rise across the country. According to the most recent Home Price Index (HPI) from CoreLogic, national home prices increased 15.4% year-over-year in May: “The May 2021 HPI gain was up from the May 2020 gain of 4.2% and was the highest year-over-year gain since November 2005. Low mortgage rates and low for-sale inventory drove the increase in home prices.” Rising home values are a big part of why real estate remains one of the top sought-after investments for Americans. For potential sellers, it also means it’s a great time to list your house to maximize the return on your investment. A Rise in Home Values and Equity The equity in a home doesn’t just grow when a homeowner pays their mortgage – it also grows as the home’s value appreciates. Thanks to the jump in price appreciation, homeowners across the country are seeing record-breaking gains in home equity. CoreLogic recently reported: “…homeowners with mortgages (which account for roughly 62% of all properties) have seen their equity increase by 19.6% year over year, representing a collective equity gain of over $1.9 trillion, and an average gain of $33,400 per borrower, since the first quarter of 2020.” That’s a major perk for households to leverage. Homeowners can use that equity to accomplish major life goals or move into their dream homes. Bottom Line If you’re thinking about buying or selling, there’s no time like the present. Reach out to a local real estate professional to talk about how you can take advantage of the conditions we’re seeing today to meet your homeownership goals. SOURCE KCM #ForBuyers #ForSellers #Pricing #SimardRealtyGroup #RealBrokerLLC  With home prices continuing to deliver double-digit increases, some are concerned we’re in a housing bubble like the one in 2006. However, a closer look at the market data indicates this is nothing like 2006 for three major reasons. 1. The housing market isn’t driven by risky mortgage loans. Back in 2006, nearly everyone could qualify for a loan. The Mortgage Credit Availability Index (MCAI) from the Mortgage Bankers’ Association is an indicator of the availability of mortgage money. The higher the index, the easier it is to obtain a mortgage. The MCAI more than doubled from 2004 (378) to 2006 (869). Today, the index stands at 130. As an example of the difference between today and 2006, let’s look at the volume of mortgages that originated when a buyer had less than a 620 credit score.  Dr. Frank Nothaft, Chief Economist for CoreLogic, reiterates this point: “There are marked differences in today’s run up in prices compared to 2005, which was a bubble fueled by risky loans and lenient underwriting. Today, loans with high-risk features are absent and mortgage underwriting is prudent.” 2. Homeowners aren’t using their homes as ATMs this time. During the housing bubble, as prices skyrocketed, people were refinancing their homes and pulling out large sums of cash. As prices began to fall, that caused many to spiral into a negative equity situation (where their mortgage was higher than the value of the house). Today, homeowners are letting their equity build. Tappable equity is the amount available for homeowners to access before hitting a maximum 80% combined loan-to-value ratio (thus still leaving them with at least 20% equity). In 2006, that number was $4.6 billion. Today, that number stands at over $8 billion. Yet, the percentage of cash-out refinances (where the homeowner takes out at least 5% more than their original mortgage amount) is half of what it was in 2006.  3. This time, it’s simply a matter of supply and demand. FOMO (the Fear Of Missing Out) dominated the housing market leading up to the 2006 housing bubble and drove up buyer demand. Back then, housing supply more than kept up as many homeowners put their houses on the market, as evidenced by the over seven months’ supply of existing housing inventory available for sale in 2006. Today, that number is barely two months. Builders also overbuilt during the bubble but pulled back significantly over the next decade. Sam Khater, VP and Chief Economist, Economic & Housing Research at Freddie Mac, explains that pullback is the major factor in the lack of available inventory today: “The main driver of the housing shortfall has been the long-term decline in the construction of single-family homes.” Here’s a chart that quantifies Khater’s remarks:  Today, there are simply not enough homes to keep up with current demand.

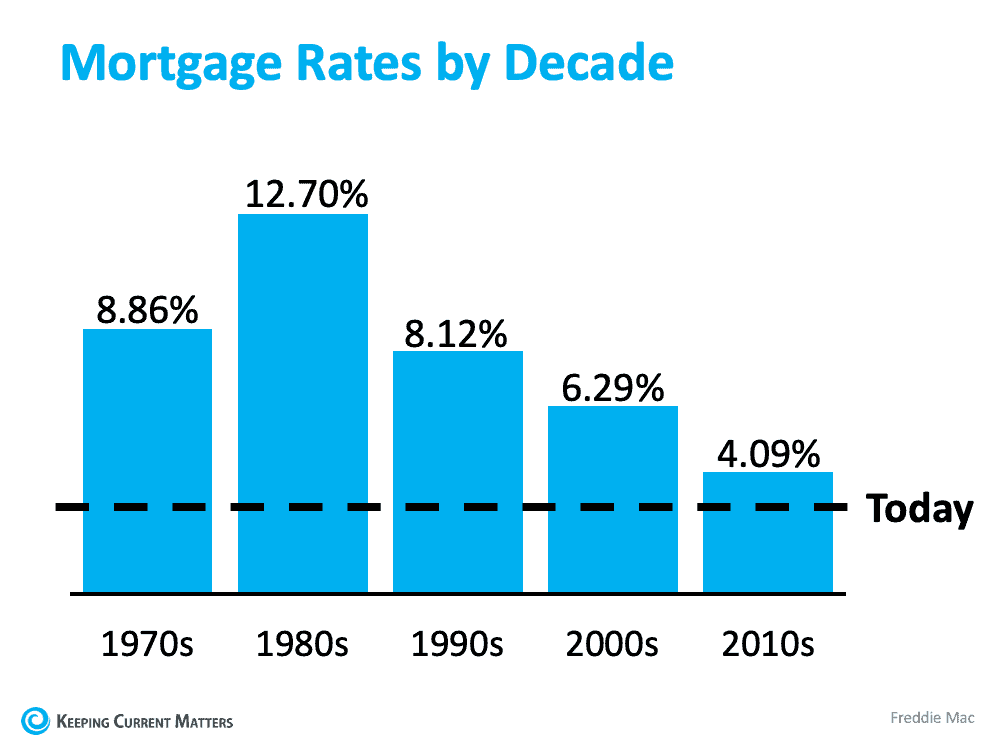

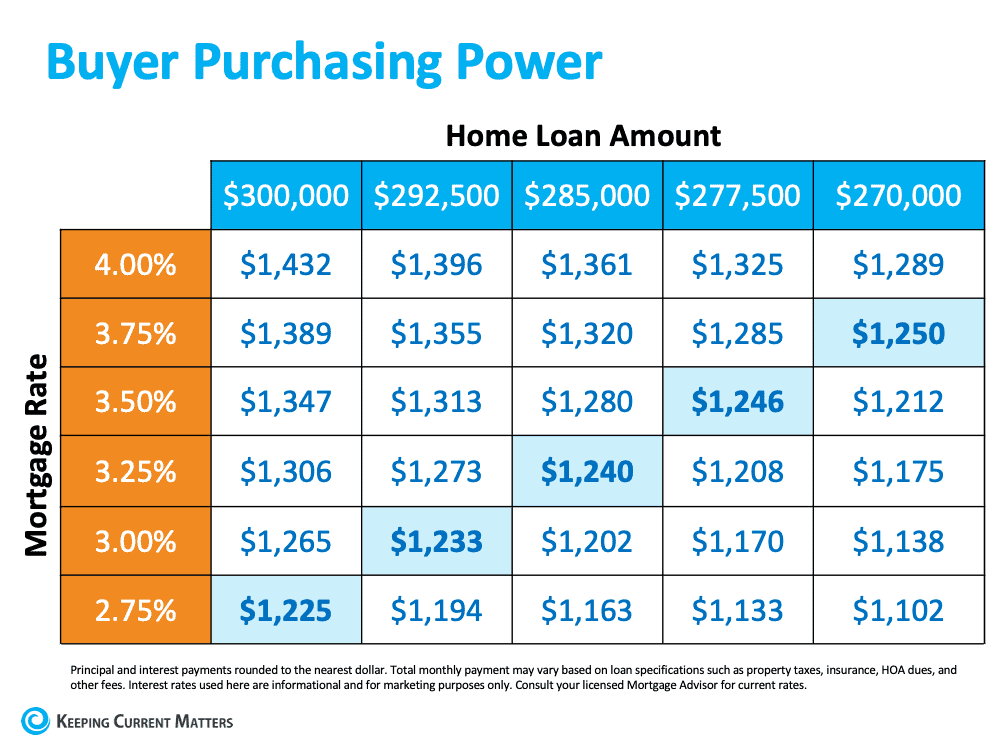

Bottom Line This market is nothing like the run-up to 2006. Bill McBride, the author of the prestigious Calculated Risk blog, predicted the last housing bubble and crash. This is what he has to say about today’s housing market: “It’s not clear at all to me that things are going to slow down significantly in the near future. In 2005, I had a strong sense that the hot market would turn and that, when it turned, things would get very ugly. Today, I don’t have that sense at all, because all of the fundamentals are there. Demand will be high for a while because Millennials need houses. Prices will keep rising for a while because inventory is so low.” SOURCE KCM #Pricing #NewConstruction #HousingMarketUpdates #SimardRealtyGroup #RealBrokerLLC  In today’s real estate market, mortgage interest rates are near record lows. If you’ve been in your current home for several years and haven’t refinanced lately, there’s a good chance you have a mortgage with an interest rate higher than today’s average. Here are some options you should consider if you want to take advantage of today’s current low rates before they rise. Sell and Move Up (or Downsize) Many of today’s homeowners are rethinking what they need in a home and redefining what their dream home means. For some, continued remote work is bringing about the need for additional space. For others, moving to a lower cost-of-living area or downsizing may be great options. If you’re considering either of these, there may not be a better time to move. Here’s why. The chart below shows average mortgage rates by decade compared to where they are today:  Today’s rates are below 3%, but experts forecast rates to rise over the next few years. If the interest rate on your current mortgage is higher than today’s average, take advantage of this opportunity by making a move and securing a lower rate. Lower rates mean you may be able to get more house for your money and still have a lower monthly mortgage payment than you might expect. Waiting, however, might mean you miss out on this historic opportunity. Below is a chart showing how your monthly payment will change if you buy a home as mortgage rates increase:  Breaking It All Down:

Using the chart above, let’s look at the breakdown of a $300,000 mortgage:

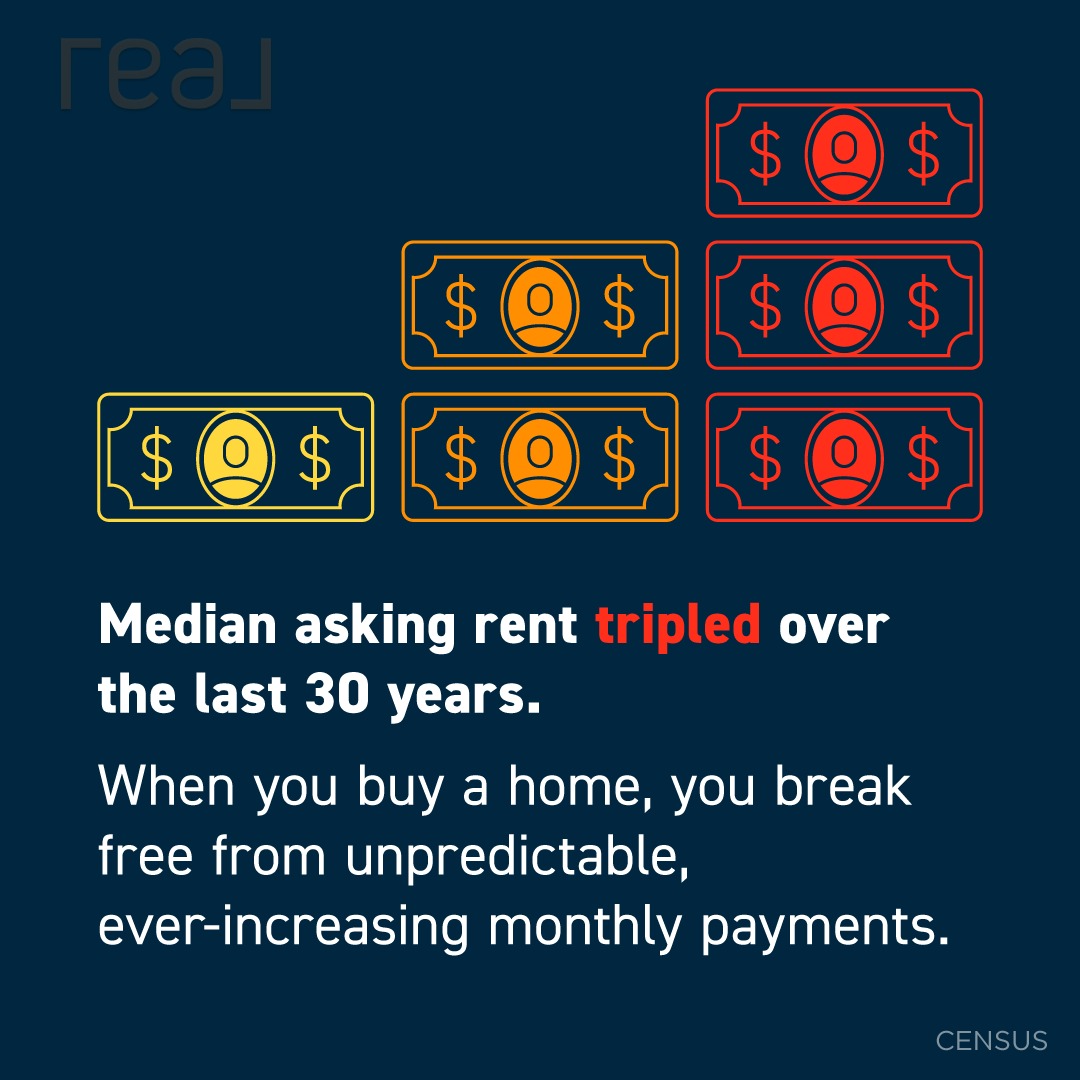

No matter what, whether you’re looking to make a move up or downsize to a home that better suits your needs, now is the time. Even a small change in interest rates can have a big impact on your purchasing power. Refinance If making a move right now still doesn’t feel right for you, consider refinancing. With the current low mortgage rates, refinancing is a great option if you’re looking to lower your monthly payments and stay in your current home. Bottom Line Take advantage of today’s low rates before they begin to rise. Whether you’re thinking about moving up, downsizing, or refinancing, talk to your trusted local real estate advisor today to discuss your options. SOURCE KCM #BuyingMyths #ForBuyer #ForSellers #InterestRates #SimardRealtyGroup  The median asking rent has tripled over the last 30 years. When you buy a home, you break free from unpredictable, ever-increasing monthly payments. If you’re debating whether to rent or buy, you should consider the long-term benefits of owning your own home. DM me today to learn why homeownership is the right call for so many people right now.

#breakfree #rentvsbuy #rentsrising #growyourwealth #buyingpower #homepriceappreciation #affordability #realestate #homevalues #homeownership #homebuying #realestategoals #homebuying #realestatetipsandadvice #keepingcurrentmatters  Some Highlights:

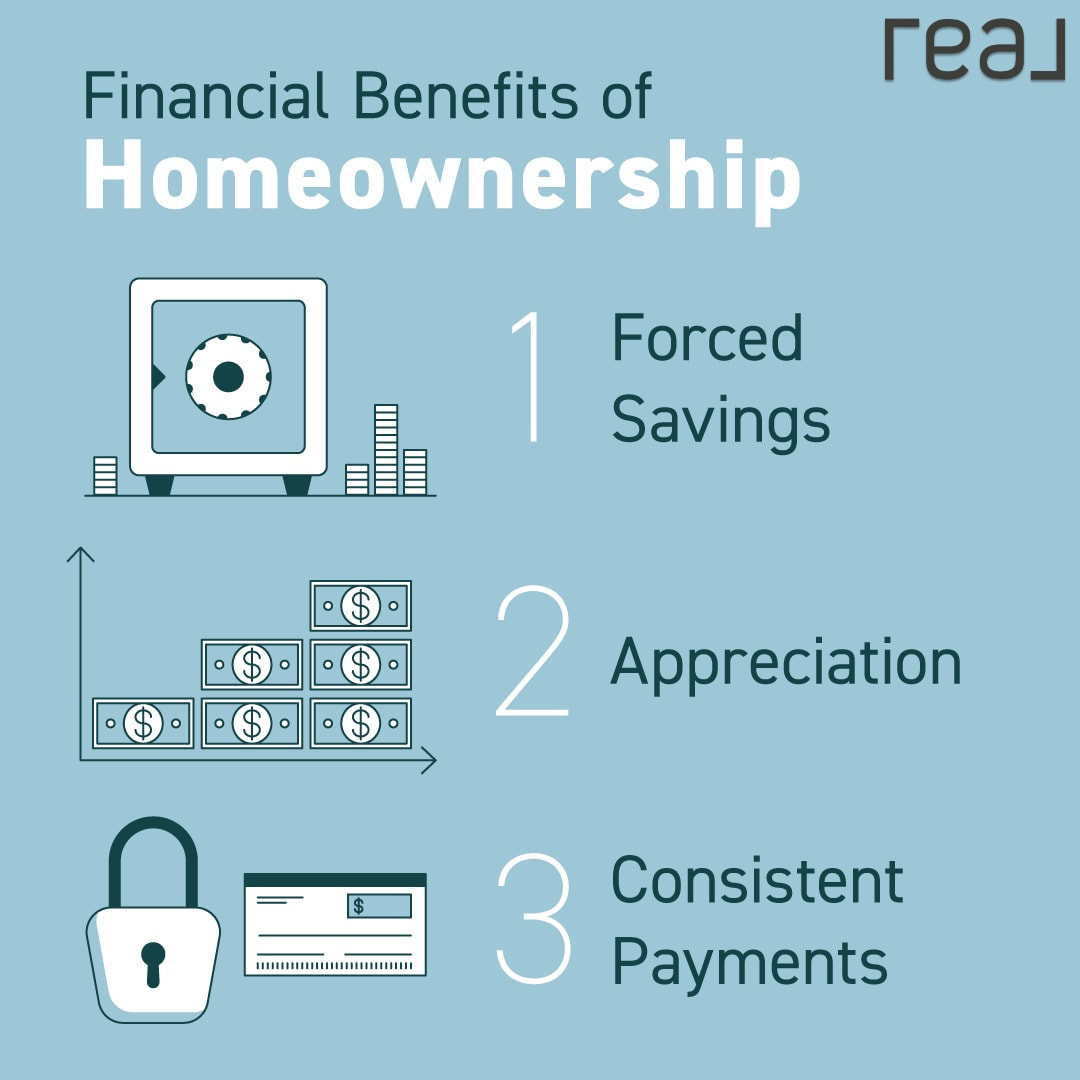

SOURCE KCM #BuyingMyths #HousingMarketUpdate #MoveUpBuyers #SimardRealttyGroup #RealBrokerLLC  Homeownership is full of benefits. On the financial side, these include:

>> a form of forced savings for your household >> a way to take advantage of home price appreciation >> consistent mortgage payments instead of rising rent payments DM me if you’re ready to receive these benefits by becoming a homeowner. #homeownership #financialbenefits #firsttimehomebuyer #opportunity #housingmarket #househunting #makememove #homegoals #houseshopping #housegoals #starterhome #dreamhome #curbappeal #keepingcurrentmatters  Last week, Fannie Mae released their Home Purchase Sentiment Index (HPSI). Though the survey showed 77% of respondents believe it’s a “good time to sell,” it also confirms what many are sensing: an increasing number of Americans believe it’s a “bad time to buy” a home. The percentage of those surveyed saying it’s a “bad time to buy” hit 64%, up from 56% last month and 38% last July. The latest HPSI explains: “Consumers also continued to cite high home prices as the predominant reason for their ongoing and significant divergence in sentiment toward homebuying and home-selling conditions. While all surveyed segments have expressed greater negativity toward homebuying over the last few months, renters who say they are planning to buy a home in the next few years have demonstrated an even steeper decline in homebuying sentiment than homeowners. It’s likely that affordability concerns are more greatly affecting those who aspire to be first-time homeowners than other consumer segments.” Let’s look closely at the market conditions that impact home affordability. A mortgage payment is determined by the price of the home and the mortgage rate on the loan used to purchase it. Lately, monthly mortgage payments have gone up for buyers for two key reasons:

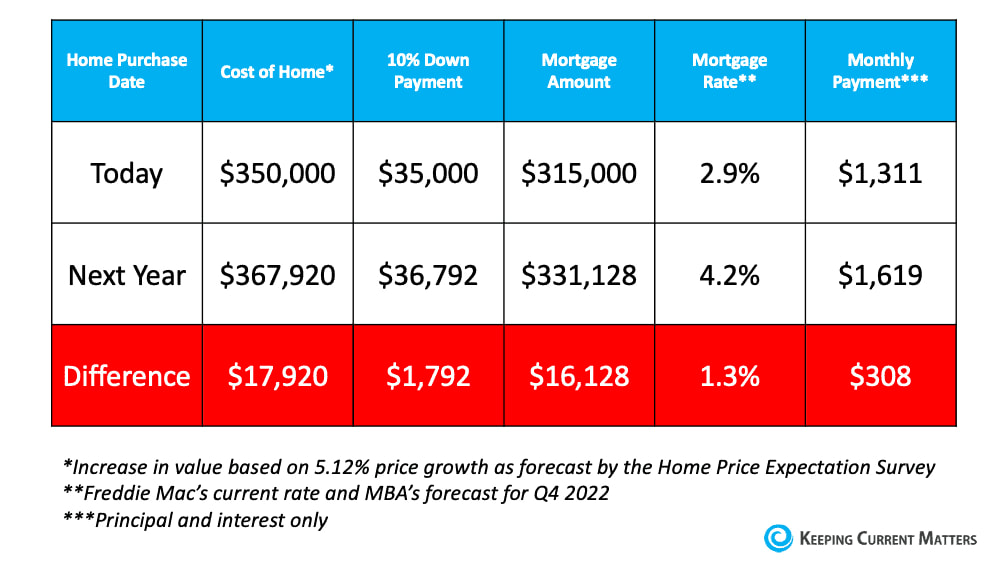

Three weeks ago, ATTOM Data released their second-quarter 2021 U.S. Home Affordability Report which explained that the major ownership costs on the typical home as a percent of the average national wage had increased from 22.2% in the second quarter of 2020 to 25.2% in the second quarter of this year. They also went on to explain: “Still, the latest level is within the 28 percent standard lenders prefer for how much homeowners should spend on mortgage payments, home insurance and property taxes.” In the same report, Todd Teta, Chief Product Officer with ATTOM, confirms: “Average workers across the country can still manage the major expenses of owning a home, based on lender standards.” It’s true that monthly mortgage payments are greater than they were last year (as the ATTOM data shows), but they’re not unaffordable when compared to the last 30 years. While payments have increased dramatically during that several-decade span, if we adjust for inflation, today’s mortgage payments are 10.7% lower than they were in 1990. What’s that mean for you? While you may not get the homebuying deal someone you know got last year, that doesn’t mean you shouldn’t still buy a home. Here are your alternatives to buying and the trade-offs you’ll have with each. Alternative 1: I’ll rent instead. Some may consider renting as the better option. However, the monthly cost of renting a home is skyrocketing. According to the July National Rent Report from Apartment List: “…So far in 2021, rental prices have grown a staggering 9.2%. To put that in context, in previous years growth from January to June is usually just 2 to 3%. After this month’s spike, rents have been pushed well above our expectations of where they would have been had the pandemic not disrupted the market.” If you continue to rent, chances are your rent will keep increasing at a fast pace. That means you could end up spending significantly more of your income on your rental as time goes on, which could make it even harder to save for a home. Alternative 2: I’ll wait it out. Others may consider waiting for another year and hoping that purchasing a home will be less expensive then. Let’s look at that possibility. We’ve already established that a monthly mortgage payment is determined by the price of the home and the mortgage rate. A lower monthly payment would require one of those two elements to decrease over the next year. However, experts are forecasting the exact opposite:

By waiting until next year, you’d potentially pay more for the home, need a larger down payment, pay a higher mortgage rate, and pay an additional $3,696 each year over the life of the mortgage.

Bottom Line While you may have missed the absolute best time to buy a home, waiting any longer may not make sense. Mark Fleming, Chief Economist at First American, says it best: “Affordability is likely to worsen before it improves, so try to buy it now, if you can find it.” SOURCE KCM #BuyingMyths #InterestRates #Pricing #SimardRealtyGroup #RealBrokerLLC  The only thing hotter than a scorching July day? Today’s real estate market. Whether you’re buying a home or selling your house this summer, there are major opportunities you can take advantage of. DM me so we can make sure this is a hot season for your housing market goals.

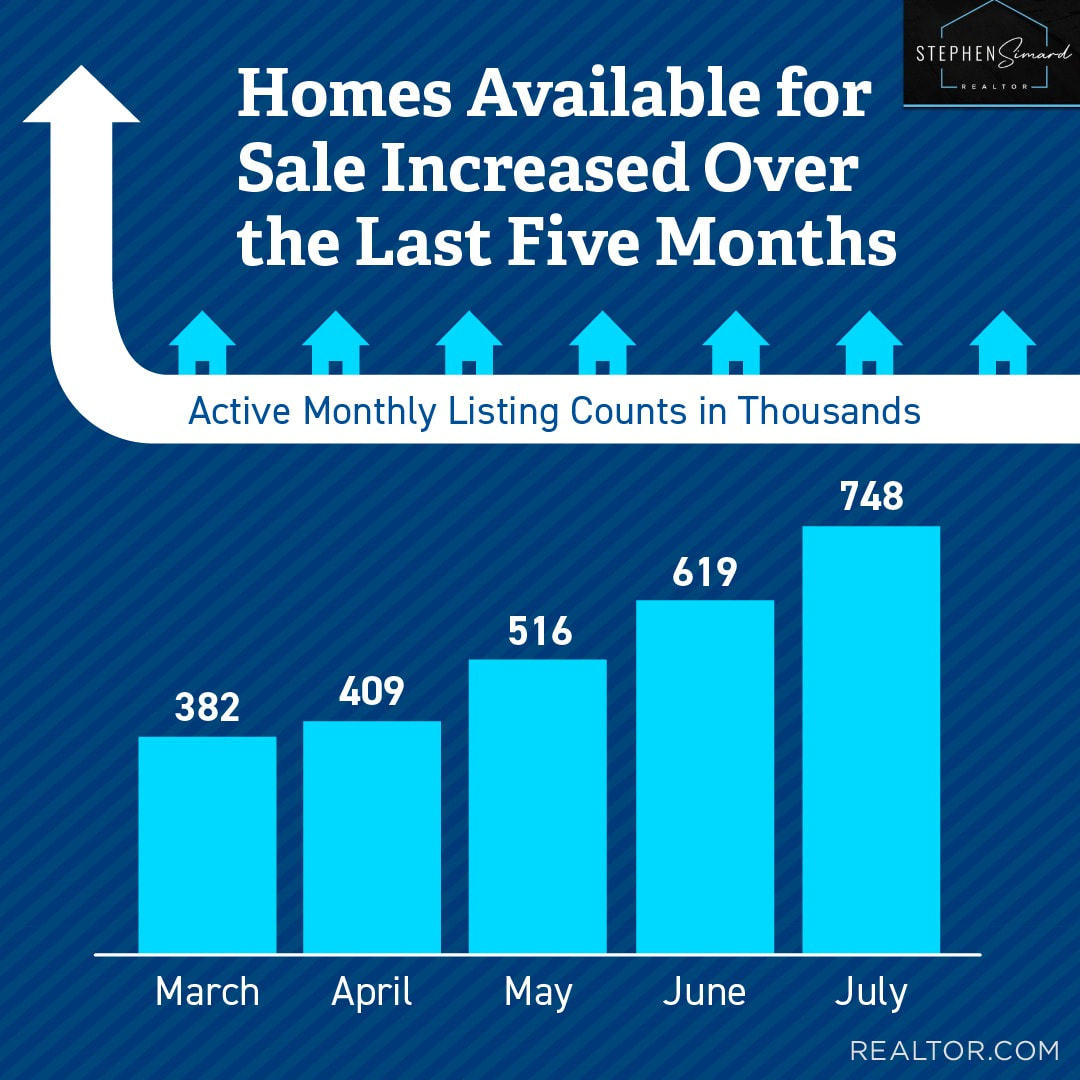

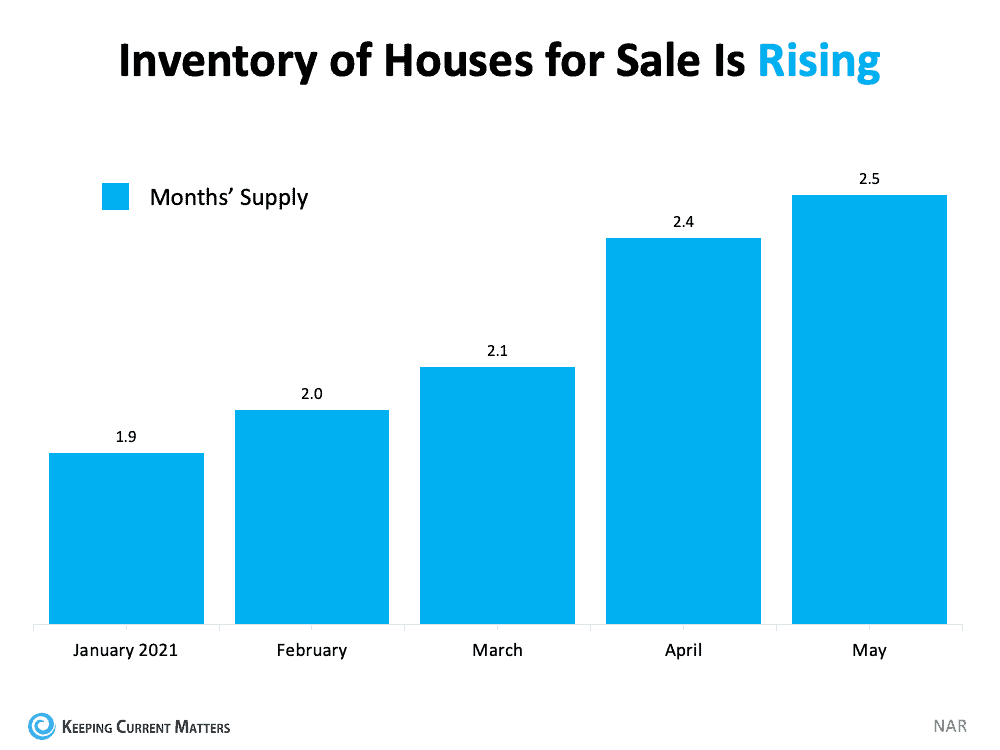

#summerrealestate #buyingahome #sellingyourhouse #realestate #homeownership #homebuying #realestategoals #realestateagent #realestateexpert #realestateagency #realestateexperts #realestateagents #instarealestate #keepingcurrentmatters  An important factor in today’s market is the number of homes for sale. While inventory levels continue to sit near historic lows, there are indications we may have hit the lowest point we’ll see. Odeta Kushi, Deputy Chief Economist at First American, recently said of our supply challenges: “It looks like inventory may have hit a bottom (we’ve seen this in the higher frequency data as well). Unsold inventory in May was at 2.5 months supply, up from 2.4.” To put it into perspective, the graph below shows levels of inventory rising since the beginning of the year:  We’re still not close to a balanced market, which would be a 6 months’ supply of homes for sale. However, we are seeing a slow but steady increase in homes coming up for sale. And that leaves many buyers and sellers wondering the same thing: what does that mean for me? Buyers: More Options Are Arriving, so It’s Time To Act If you’re a buyer, more inventory coming to market is a welcome sight. More supply means more options and less competition, which could mean fewer bidding wars. According to the latest Monthly Housing Market Trends Report, supply levels are continuing to increase, which is different from the typical summer market: “In June, newly listed homes grew by 5.5% on a year-over-year basis, and by 10.9% on a month-over-month basis. Typically, fewer newly listed homes appear on the market in the month of June compared to May. This year, growth in new listings is continuing later into the summer season, a welcome sign for a tight housing market.” If you’re having trouble finding your next home, this news should give you the hope and motivation to keep your buying process moving forward. Experts project mortgage rates will begin increasing, which will make purchasing a home less affordable as time passes. You can still capitalize on today’s low interest rates, so stick with your search as more homes come to market. Sellers: Our Supply Challenges Aren’t Over Yet, so Now Is the Time To Sell If you’ve been putting off selling your house, you shouldn’t wait much longer. The year’s month-over-month gains in homes for sale have helped buyers, but we’re still very much in a sellers’ market. As the graph below shows, even with the number of homes for sale rising, we’re still well below the supply levels we’ve seen historically:  Of course, more homes are coming to market now, and more are expected in the coming months. Selling your house this summer gives you the chance to get ahead of the competition and maximize your sales potential before more homes are put up for sale in your neighborhood.

Bottom Line More homes for sale means more options for buyers and more competition for sellers. Whether you’re looking to buy or sell, connect with your trusted real estate advisor today to discuss your options and why it’s still a good time to make your move. SOURCE KCM #ForBuyers #ForSellers #HousingMarketUpdate #SimardRealtyGroup |

Archives

October 2022

Categories

All

|

RSS Feed

RSS Feed