Some Highlights:

SOURCE KCM #Buyers #InterestRates #SimardRealtyGroup #eXpRealty

0 Comments

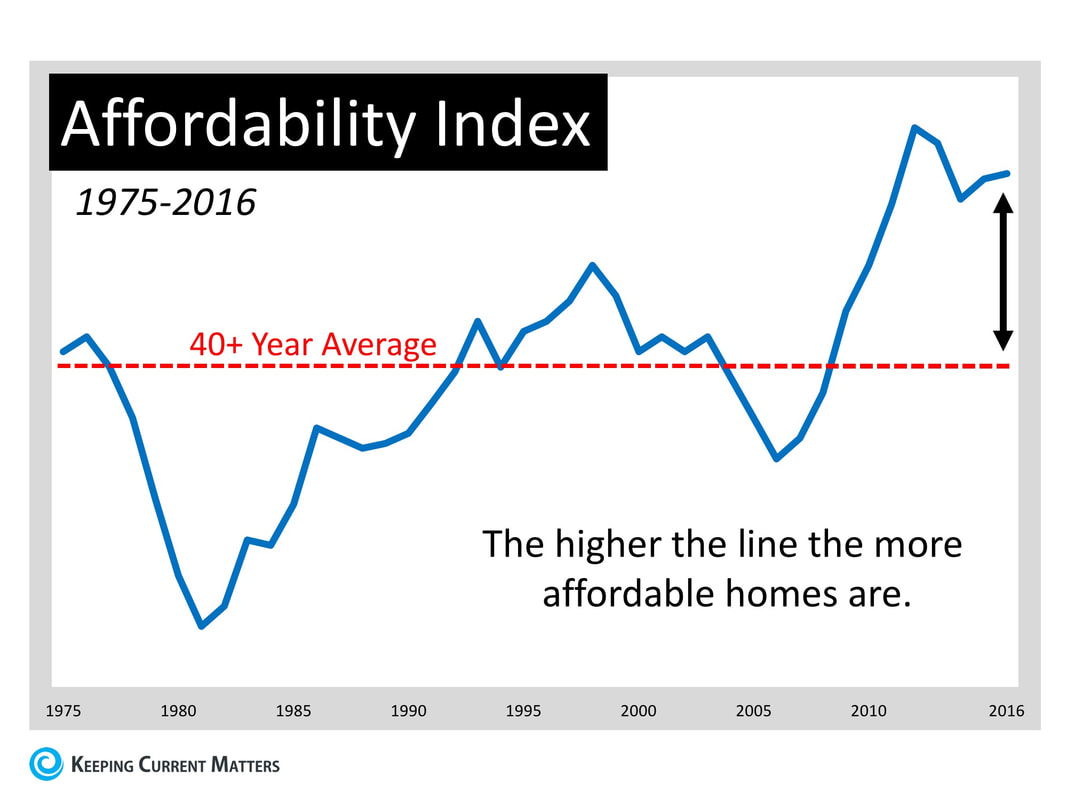

If you are considering selling your current home, to either move up to a larger home or into a home in an area that better suits your current family needs, great news was just revealed. Last week, Trulia posted a blog, Not Your Father’s Housing Market, which examined home affordability over the last 40+ years (1975-2016). Their research revealed that: “Nationally, homes are just about the most affordable they’ve been in the last 40 years… the median household could afford a home 1.5 times more expensive than the median home price. In 1980, the median household could only afford about 3/4 of the median home price. Despite relatively stagnant incomes, affordability has grown due to the sharp drop in mortgage rates over the last 30 years – from a high of over 16% in the 1980s to under 4% by 2016. Of the nation’s 100 largest metros, only Miami became unaffordable between 1990 and 2016. Meanwhile, 22 metros have flipped from being unaffordable to becoming affordable in that same time frame.” Here is a graph showing the Affordability Index compared to the 40-year average:  The graph shows that housing affordability is better now than at any other time in the last forty years, except during the housing crash last decade.

(Remember that during the crash you could purchase distressed properties – foreclosures and short sales – at 20-50% discounts.) There is no doubt that with home prices and mortgage rates on the rise, the affordability index will continue to fall. That is why if you are thinking of moving up, you probably shouldn’t wait. Bottom Line If you have held off on moving up to your family’s dream home because you were hoping to time the market, that time has come. SOURCE KCM #Buyers #Sellers #CTNews #SimardRealtyGroup #JoineXpRealty  As more and more baby boomers enter retirement age, the question of whether or not to sell their homes and move will become a hot topic. In today’s housing market climate, with low available inventory in the starter and trade-up home categories, it makes sense to evaluate your home’s ability to adapt to your needs in retirement.

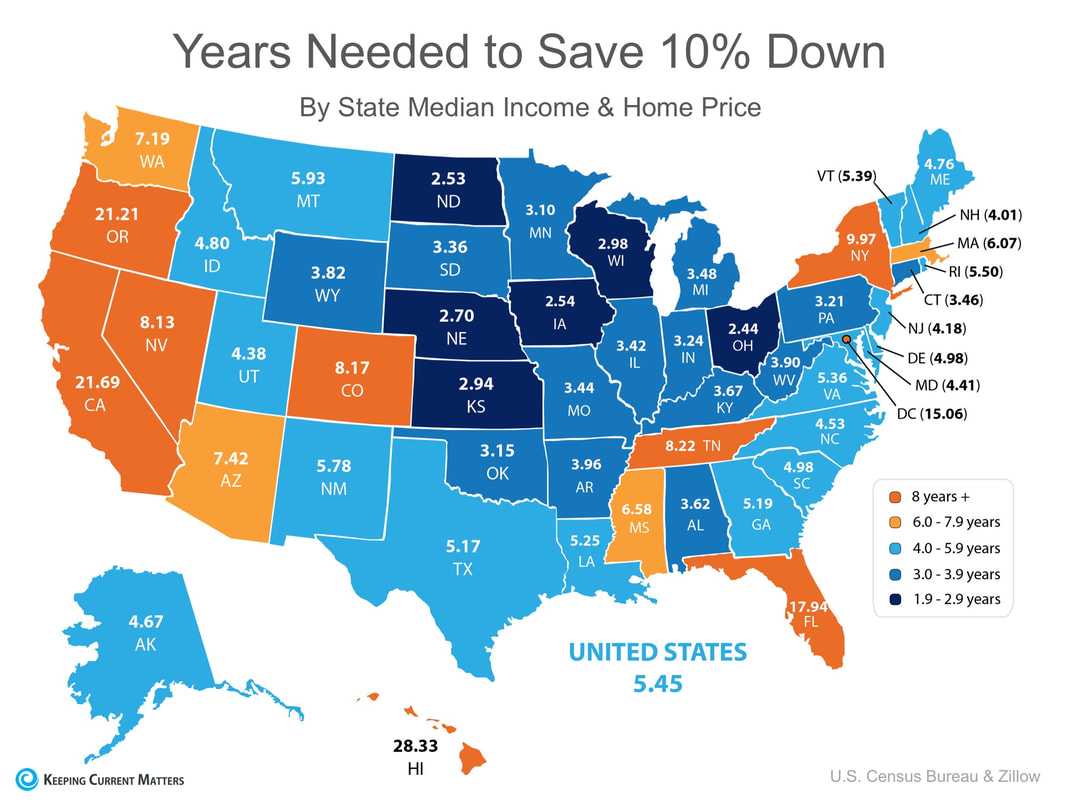

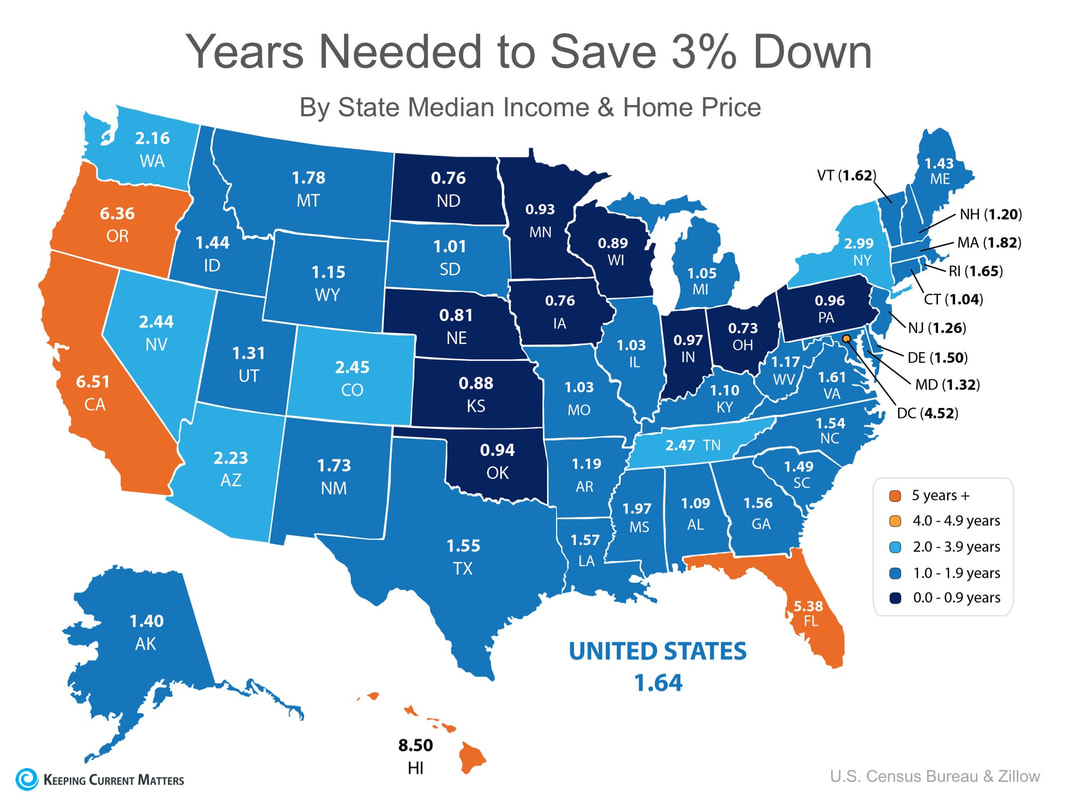

According to the National Association of Exclusive Buyers Agents (NAEBA), there are 7 factors that you should consider when choosing your retirement home. 1. Affordability “It may be easy enough to purchase your home today but think long-term about your monthly costs. Account for property taxes, insurance, HOA fees, utilities – all the things that will be due whether or not you have a mortgage on the property.” Would moving to a complex with homeowner association fees actually be cheaper than having to hire all the contractors you would need to maintain your home, lawn, etc.? Would your taxes go down significantly if you relocated? What is your monthly income going to be like in retirement? 2. Equity “If you have equity in your current home, you may be able to apply it to the purchase of your next home. Maintaining a healthy amount of home equity gives you a source of emergency funds to tap, via a home equity loan or reverse mortgage.” The equity you have in your current home may be enough to purchase your retirement home with little to no mortgage. Homeowners in the US gained an average of over $14,000 in equity last year. 3. Maintenance “As we age, our tolerance for cleaning gutters, raking leaves and shoveling snow can go right out the window. A condominium with low-maintenance needs can be a literal lifesaver, if your health or physical abilities decline.” As we mentioned earlier, would a condo with an HOA fee be worth the added peace of mind of not having to do the maintenance work yourself? 4. Security “Elderly homeowners can be targets for scams or break-ins. Living in a home with security features, such as a manned gate house, resident-only access and a security system can bring peace of mind.” As scary as that thought may be, any additional security and an extra set of eyes looking out for you always adds to peace of mind. 5. Pets “Renting won’t do if the dog can’t come too! The companionship of pets can provide emotional and physical benefits.” Evaluate all of your options when it comes to bringing your ‘furever’ friend with you to a new home. Will there be necessary additional deposits if you are renting or in a condo? Is the backyard fenced in? How far are you from your favorite veterinarian? 6. Mobility “No one wants to picture themselves in a wheelchair or a walker, but the home layout must be able to accommodate limited mobility.” Sixty is the new 40, right? People are living longer and are more active in retirement, but that doesn’t mean that down the road you won’t need your home to be more accessible. Installing handrails and making sure your hallways and doorways are wide enough may be a good reason to look for a home that was built to accommodate these needs. 7. Convenience “Is the new home close to the golf course, or to shopping and dining? Do you have amenities within easy walking distance? This can add to home value!” How close are you to your children and grandchildren? Would relocating to a new area make visits with family easier or more frequent? Beyond being close to your favorite stores and restaurants, there are a lot of factors to consider. Bottom Line When it comes to your forever home, evaluating your current house for its ability to adapt with you as you age can be the first step to guaranteeing your comfort in retirement. If after considering all these factors you find yourself curious about your options, contact a local real estate professional who can evaluate your ability to sell your house in today’s market and get you into your dream retirement home! SOURCE KCM #Buyers #Retired #SimardRealtyGroup #joineXpRealty  Saving for a down payment is often the biggest hurdle for a first-time homebuyer. Depending on where you live, median income, median rents, and home prices all vary. So, we set out to find out how long it would take to save for a down payment in each state. Using data from the United States Census Bureau and Zillow, we determined how long it would take, nationwide, for a first-time buyer to save enough money for a down payment on their dream home. There is a long-standing ‘rule’ that a household should not pay more than 28% of their income on their monthly housing expense. By determining the percentage of income spent renting in each state, and the amount needed for a 10% down payment, we were able to establish how long (in years) it would take for an average resident to save enough money to buy a home of their own. According to the data, residents in Ohio can save for a down payment the quickest in just under 3 years (2.44). Below is a map that was created using the data for each state:  What if you only needed to save 3%? What if you were able to take advantage of one of Freddie Mac’s or Fannie Mae’s 3%-down programs? Suddenly, saving for a down payment no longer takes 5 or 10 years, but becomes possible in a year or two in many states as shown on the map below.  Bottom LineWhether you have just begun to save for a down payment, or have been saving for years, you may be closer to your dream home than you think! Meet with a local real estate professional who can help you evaluate your ability to buy today.

SOURCE KCM #DownPayments #Buyers #SimardRealtyGroup #joineXpRealty  Here are four great reasons to consider buying a home today instead of waiting.

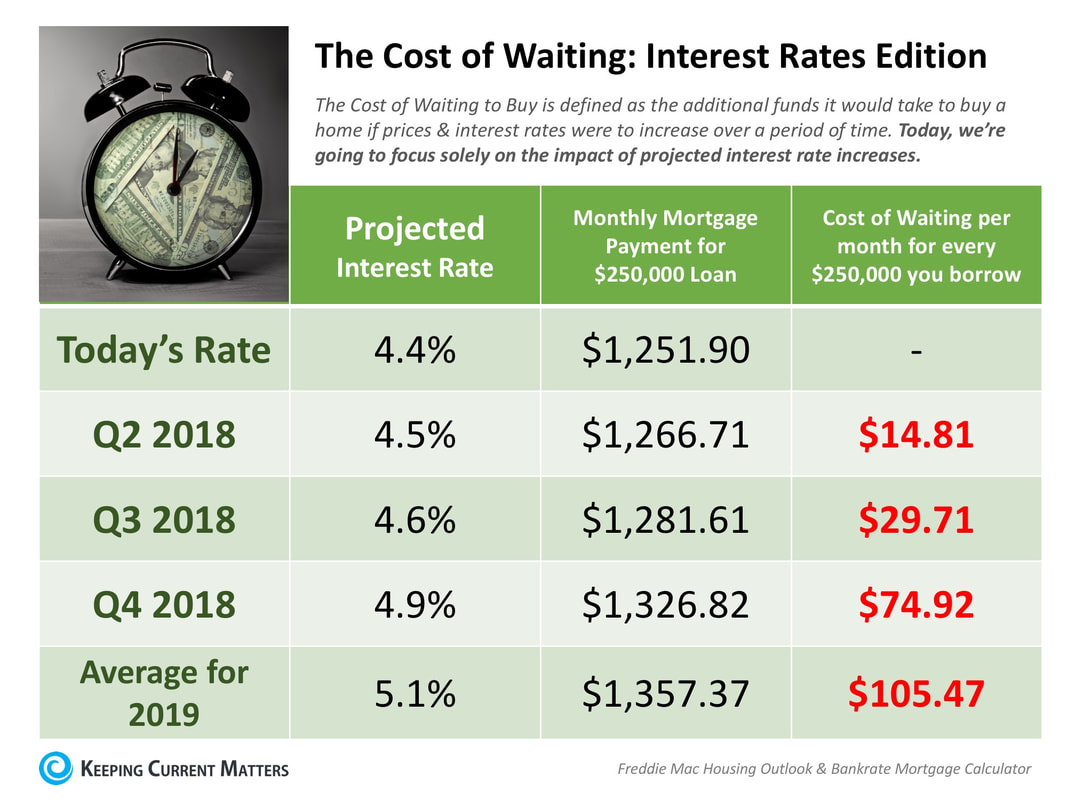

Prices Will Continue to Rise CoreLogic’s latest Home Price Index reports that home prices have appreciated by 6.6% over the last 12 months. The same report predicts that prices will continue to increase at a rate of 4.3% over the next year. The bottom in home prices has come and gone. Home values will continue to appreciate for years. Waiting no longer makes sense. Mortgage Interest Rates Are Projected to Increase Freddie Mac’s Primary Mortgage Market Survey shows that interest rates for a 30-year mortgage hovered close to 4.0% in 2017. Most experts predict that rates will rise over the next 12 months. The Mortgage Bankers Association, Fannie Mae, Freddie Mac and the National Association of Realtors are in unison, projecting that rates will increase by nearly a full percentage point by this time next year. An increase in rates will impact YOUR monthly mortgage payment. A year from now, your housing expense will increase if a mortgage is necessary to buy your next home. Either Way, You Are Paying a Mortgage There are some renters who have not yet purchased a home because they are uncomfortable taking on the obligation of a mortgage. Everyone should realize that unless you are living with your parents rent-free, you are paying a mortgage – either yours or your landlord’s. As an owner, your mortgage payment is a form of ‘forced savings’ that allows you to have equity in your home that you can tap into later in life. As a renter, you guarantee your landlord is the person with that equity. Are you ready to put your housing cost to work for you? It’s Time to Move on with Your Life The ‘cost’ of a home is determined by two major components: the price of the home and the current mortgage rate. It appears that both are on the rise. But what if they weren’t? Would you wait? Look at the actual reason you are buying and decide if it is worth waiting. Whether you want to have a great place for your children to grow up, you want your family to be safer, or you just want to have control over renovations, maybe now is the time to buy. If the right thing for you and your family is to purchase a home this year, buying sooner rather than later could lead to substantial savings. SOURCE KCM #Buyers #SpringMarket #SimardRealtyGroup #joineXpRealty  Some Highlights:

SOURCE KCM #ForBuyers #ForSellers #SimardRealtyGroup #eXpRealty  A recent report by CoreLogic revealed that U.S. home values appreciated by more than 37% over the last five years. Some are concerned that this is evidence we may be on the verge of another housing “boom & bust” like the one we experienced from 2006-2008.

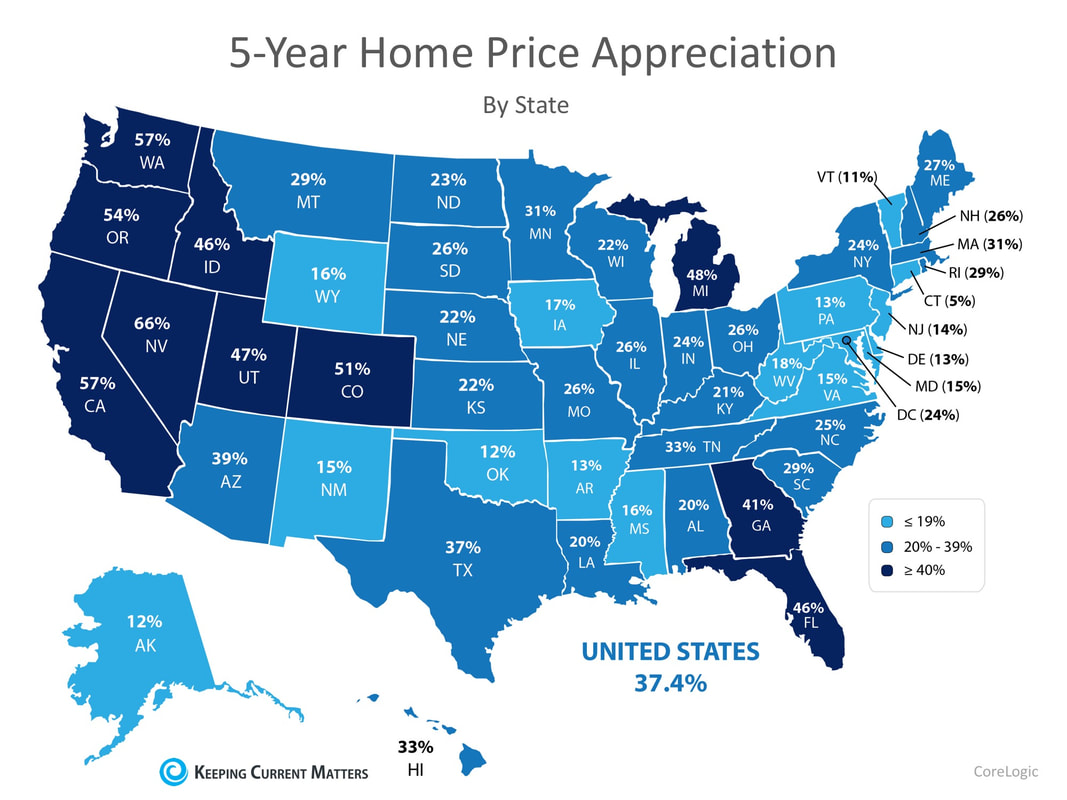

Recently, several housing experts weighed in on the subject to alleviate these fears. Sean Becketti, Freddie Mac Chief Economist “The evidence indicates there currently is no house price bubble in the U.S., despite the rapid increase of house prices over the last five years.” Edward Golding, a Senior Fellow at the Urban Institute’s Housing Finance Policy Center “There is not likely to be a national bubble in the way that we saw the first decade of the century.” Christopher Thornberg, Partner at Beacon Economics “There is no direct or indirect sign of any kind of bubble.” Bill McBride, Calculated Risk “I wouldn’t call house prices a bubble.” David M. Blitzer, Chairman of the Index Committee at S&P Dow Jones Indices “Housing is not repeating the bubble period of 2000-2006.” A recent article by Teo Nicolais, a real estate entrepreneur who teaches courses on real estate principles, markets, and finance at Harvard Extension School concluded that the next housing bubble may not occur until 2024. The article, How to Use Real Estate Trends to Predict the Next Housing Bubble, looks at previous peaks in real estate values going all the way back to 1818. Nicolais uses the research of several economists. The article details the four phases of a real estate cycle and what defines each phase. Nicolais concluded his article by saying: “Those who study the financial crisis of 2008 will (we hope) always be weary of the next major crash. If George, Harrison, and Foldvary are right, however, that won’t happen until after the next peak around 2024. Between now and then, aside from the occasional slow down and inevitable market hiccups, the real estate industry is likely to enjoy a long period of expansion.” Bottom Line The reason for the price appreciation we are seeing is an imbalance between supply and demand for housing. This has created a natural increase in values, not a bubble in prices. SOURCE KCM #ForBuyers #ForSellers #sellingCT #SimardRealtyGroup #eXpRealty  The economists at CoreLogic recently released a special report entitled, Evaluating the Housing Market Since the Great Recession. The goal of the report was to look at economic recovery since the Great Recession of December 2007 through June 2009. One of the key indicators used in the report to determine the health of the housing market was home price appreciation. CoreLogic focused on appreciation from December 2012 to December 2017 to show how prices over the last five years have fared. Frank Nothaft, Chief Economist at CoreLogic, commented on the importance of breaking out the data by state, “Homeowners in the United States experienced a run-up in prices from the early 2000s to 2006, and then saw the trend reverse with steady declines through 2011. After finally reaching bottom in 2011, home prices began a slow rise back to where we are now. Greater demand and lower supply – as well as booming job markets – have given some of the hardest-hit housing markets a boost in home prices. Yet, many are still not back to pre-crash levels.” The map below was created to show the 5-year appreciation from December 2012 – December 2017 by state.  Nationally, the cumulative appreciation over the five-year period was 37.4%, with a high of 66% in Nevada, and a modest increase of 5% in Connecticut.

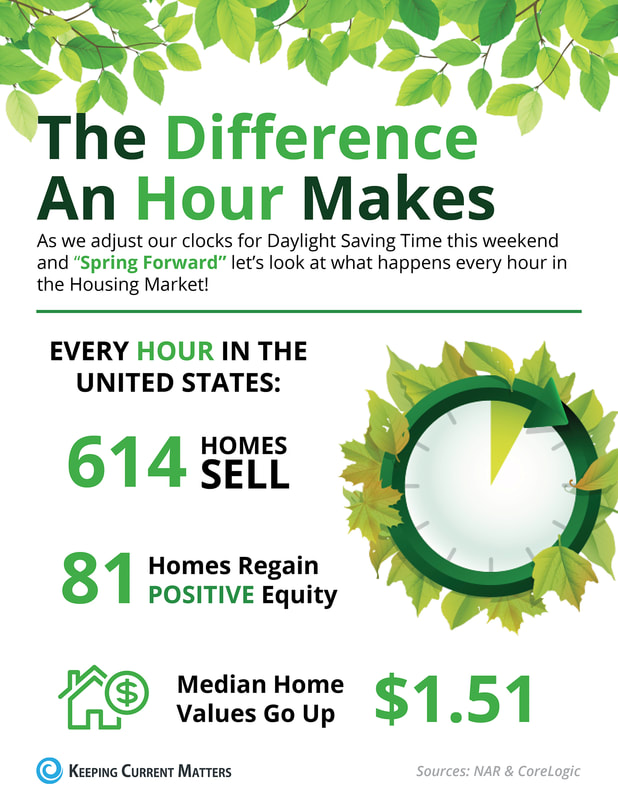

Where were prices expected to go?Every quarter, Pulsenomics surveys a nationwide panel of over 100 economists, real estate experts, and investment and market strategists and asks them to project how residential home prices will appreciate over the next five years for their Home Price Expectation Survey (HPES). According to the December 2012 survey results, national homes prices were projected to increase cumulatively by 23.1% by December 2017. The bulls of the group predicted home prices to rise by 33.6%, while the more cautious bears predicted an appreciation of 11.2%. Where are prices headed in the next 5 years? Data from the most recent HPES shows that home prices are expected to increase by 18.2% over the next 5 years. The bulls of the group predict home prices to rise by 27.4%, while the more cautious bears predict an appreciation of 8.3%. Bottom Line Every day, thousands of homeowners regain positive equity in their homes. Some homeowners are now experiencing values even higher than before the Great Recession. If you’re wondering if you have enough equity to sell your house and move on to your dream home, contact a local real estate professional who can help! SOURCE KCM #HomePrices #MarketUpdates #SimardRealtyGroup #JoineXpRealty  Just like our clocks this weekend in the majority of the country, the housing market will soon “spring forward!” Similar to tension in a spring, the lack of inventory available for sale in the market right now is what is holding back the market.

Many potential sellers believe that waiting until Spring is in their best interest, and traditionally they would have been right. Buyer demand has seasonality to it, which usually falls off in the winter months, especially in areas of the country impacted by arctic temperatures and conditions. That hasn’t happened this year. Demand for housing has remained strong as mortgage rates have remained near historic lows. Even with the recent increase in rates, buyers are still able to lock in an affordable monthly payment. Many more buyers are jumping off the fence and into the market to secure a lower rate. The National Association of Realtors (NAR) recently reported that the top 10 dates sellers listed their homes in 2017 all fell in April, May, or June. Those who act quickly and list now could benefit greatly from additional exposure to buyers prior to a flood of more competition coming to market in the next few months. Bottom Line If you are planning on selling your home in 2018, meet with a local real estate professional to evaluate the opportunities in your market SOURCE KCM #SpringMarket #ForSellers #SimardRealtyGroup #eXpRealty  Some Highlights:

SOURCE KCM #SpringMarket #Sellers #SimardRealtyGroup #JoineXpRealty |

Archives

October 2022

Categories

All

|

RSS Feed

RSS Feed